Yagi Studio/DigitalVision via Getty Images

Co-produced with Treading Softly

Have you ever heard the phrase: “There’s no such thing as a free lunch?”

It’s a folksy way of saying that nothing is free. I understand the sentiment. You have to pay for food or the service of someone else making it for you.

Life is expensive. My life, however, often does have free lunches, namely because I put my hard-earned money to work, and it pays for them.

I am an income investor who buys income and enjoys the fruit of my labors. So when the market sells two exceptionally low-risk investments, I jump at the opportunity.

This way, when it comes to paying for my lunch, I have dividends to cover it – as well as the price for my game of golf after lunch! I don’t need to sell shares of my investments to cover my expenses. The shares themselves generate the necessary income to do so.

Let’s dive in.

Pick #1: UTG – Yield 8.7%

Utilities are generally considered a “recession-resistant” sector because utility companies see little variation in their earnings in any economic condition. Utility companies typically enjoy mini-monopolies and their product is one that people can’t live without. While their pricing power is somewhat limited by government regulation, historically, utilities have been able to navigate the bureaucracy. They might not always get the price hikes they want, but in the words of the Rolling Stones, you get what you need.

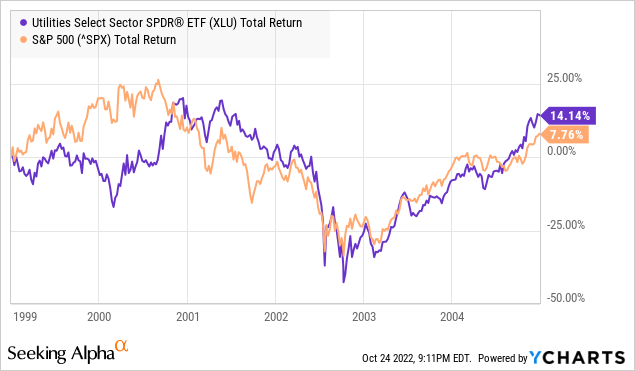

For this reason, utilities are generally considered “defensive”. But let’s be clear, the market is not a rational place. While the companies are solid and continue to produce reliable results in any economic conditions, this does not mean that the share prices stay high. I see many investors confuse “stable earnings” with “stable prices”. Share prices for utilities will fall in a market sell-off just like anything else. The chart below happened during the dot-com bust:

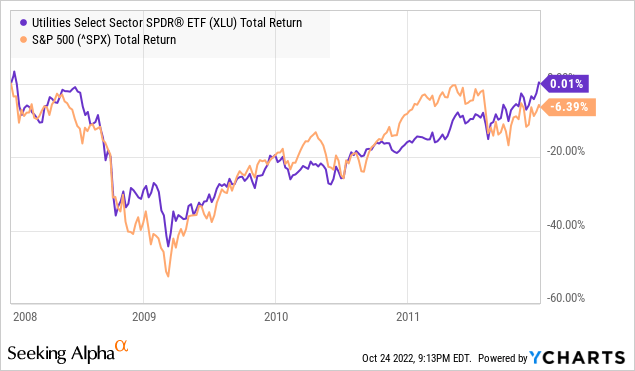

It happened during the Great Financial Crisis:

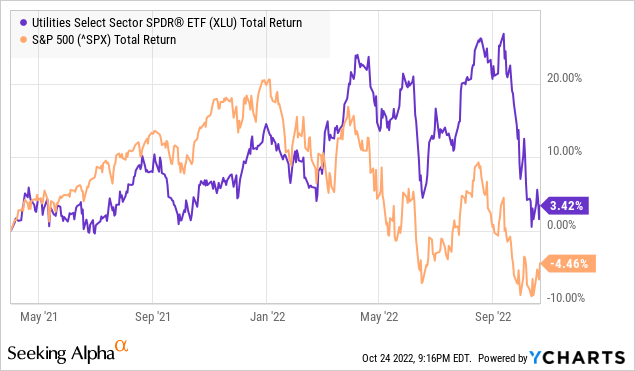

It is happening again right now:

There is no “magic bullet” that is going to protect you from downdrafts in the market when the market is selling off everything.

Utilities are defensive in that the earnings of the companies and the dividends remain strong. The valuations made by all the people trading in the market? Nothing is safe from them. People make all sorts of bad decisions all the time. The stock market is simply the aggregate result of all the decisions of every stockholder at a particular moment in time. This is why I focus on income, because, in my experience, the more people involved in arriving at a decision, the lower the quality.

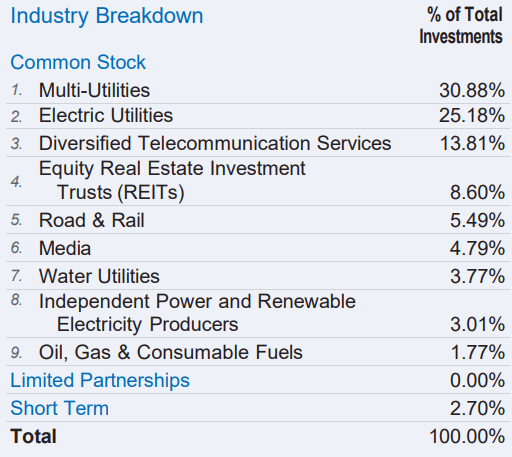

Reaves Utility Income Fund (UTG) is a CEF (closed-end fund) that invests in a diversified portfolio of utility and infrastructure companies. Source

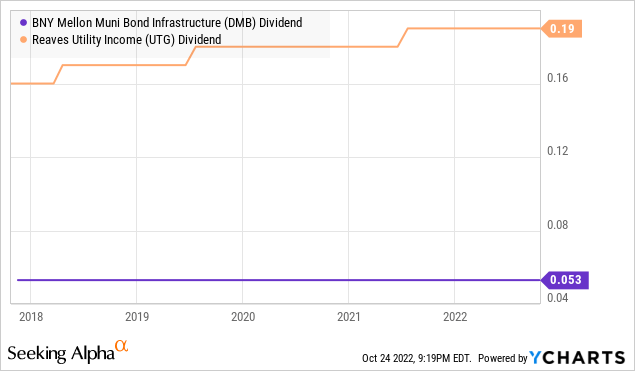

UTG

Like the S&P’s utility sector index (XLU), UTG has seen its fair share of price swings. But you know what hasn’t bounced up and down? The dividend. UTG’s dividend started at $0.10/month, and by the Great Financial Crisis, it was $0.115/month and maintained throughout with a few special dividends. UTG has seen several dividend raises since then and now pays $0.19/month.

UTG has been an extraordinarily well-run CEF, that has been tested by large sell-offs in the GFC and then COVID and come out the other side stronger than ever. Investors in the market are fearful. They are selling first and asking questions later. For income investors like us, this is an opportunity to pick up income investments at a discount.

Yes, utilities will continue to see selling pressure when everything else is falling. Their earnings will remain solid and the companies will continue producing a high level of income. Let your neighbors be the ones panicking over changes in prices while you sit back and collect a growing stream of income!

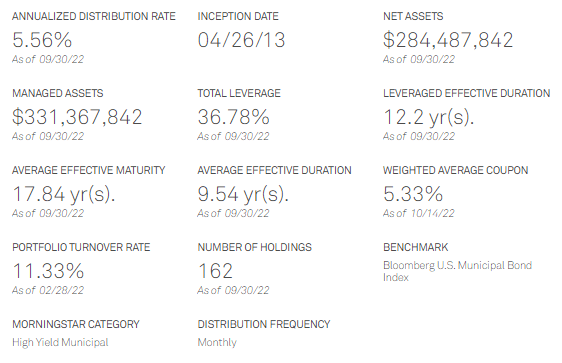

Pick #2: DMB – Yield 6.2%

BNY Mellon Municipal Bond Infrastructure Fund (DMB)

When interest rates go higher, bond investors make more money, this is a reality that is both obvious and counterintuitive at the same time. After all, bond investors make money from collecting interest payments. So if rates go higher, that means bond investors are collecting more money. If you are collecting more money, you make more money.

On the other hand, when bond yields go up, the value of all pre-existing bonds goes down. This is where many equity investors get confused because they look at bonds through the lens of total return. Worse, they calculate the total return assuming that they sell the bond right now. Unlike equity, where we don’t know how much cash it will produce over a certain period, with bonds, we know. It is predetermined and set by contract. The borrower gets $X and agrees to pay back $Y over a certain number of years. At maturity, the borrower repays 100% of the principal, and the lender profits from the interest received in the meantime. You can, at any moment, sit down and determine to the penny how much you will receive from a loan if it is paid as agreed.

When bond prices change, the amount owed doesn’t change. Typically, one of two things happens that causes bond prices to decline. Either investors predict a higher risk of default, or there are alternative investments of similar risk with a higher yield. If the former is driving the price action, then existing bondholders do need to be concerned. After all, the borrower defaulting is the only way a bond investor can have a negative return if they hold until maturity.

If bond prices are falling because interest rates are rising, then the “loss” is only because there are better opportunities and larger profits available today than there were before. You still receive the same amount of money you anticipated receiving when you made the initial investment. Your total return, if you hold until maturity, will be identical to what you calculated. Lower prices just mean that when a loan matures, you will be able to reinvest the principal at a higher interest rate and receive more income on your new investment than you received on the last one.

The key to fixed-income investing is to buy at a yield that you are happy with and then hold. Sell only if the price rises to a point that you are no longer happy with the yield.

DMB is an example of a bond fund where we weren’t happy with the yield for a long time. Prices were too high, and the yield was too low. Over the past year, the prices of DMB’s holdings declined as interest rates rose. Now we can receive a yield of 6%, which is high enough to make it attractive to us at HDO.

Municipals are bonds that are issued to state and local governments. (Source: BNY)

BNY

Note that DMB’s average coupon is at 5.33%, meaning that DMB is receiving a high enough coupon to cover the dividend. In fact, the average price of loans in DMB’s portfolio is currently $99. The decline was DMB’s portfolio coming down to par.

DMB has a portfolio that is primarily made up of investment-grade bonds, with over 46% rated A or higher.

BNY

This means that default risk is very low, especially since municipals have lower default rates than corporate bonds with similar ratings.

The loans that DMB holds have long maturities, with over 80% maturing ten or more years from now.

BNY

This creates a lot of stability for the dividend as DMB receives a fixed amount of interest and will receive that for a long time. It also means that DMB’s ability to take advantage of high-interest rates is muted. The 8.5% that is maturing this year will be reinvested at today’s rates, but the bulk is “buy and hold”, which means that the dividend you see is the dividend you are likely to get.

When you buy a municipal bond fund, the benefits are stability, safety, and attractive tax implications since the interest on municipal bonds are tax-exempt at the Federal level.

Buy at a yield that is attractive to you and meets your goals. Then hold and don’t worry about the changes in bond prices. When the Fed starts its easing cycle, the long-term bonds that DMB holds will be some of the quickest to increase in value. Until then, collect your dividend while you wait!

Shutterstock

Conclusion

UTG and DMB are both excellent dividend-paying securities. UTG offers a highly attractive 8.7% yield. DMB offers a 6.2% yield, which is exempt from Federal taxes in the U.S.

Retirees are looking for reliable income, UTG shows growth over the last 5 years, and DMB has been rock steady:

So when the market puts income on sale, I am a customer looking to enjoy the cheap prices!

This way, when it comes to buying lunch, I can pay and enjoy a free lunch – since the market is paying my bill for me!

What is paying for your lunch? Is it your retirement savings via selling shares? Is it Social Security that you worked decades to receive? Or are you still working to pay for your lunch?

I challenge you to reach the level of financial security that the market is paying your bills for you. Perhaps we can coin the term a “trophy retiree”, all I need to do is live however I want, and the market pays all my bills – no work required!

That’s the beauty of income investing. That’s the wonder of our Income Method!

Be the first to comment