Hispanolistic

If Lyft, Inc. (NASDAQ:LYFT) investors feel a sense of déjà vu after the company’s 30% plunge after Q4 results, they can be forgiven. Because even as a non-investor (in Lyft), I recall a few instances of almost similar headlines where the stock fell huge due to poor guidance. (Example 1 here, Example 2 here). Q4 earnings weren’t that bad but the gut punch came in the form of Q1’s revenue guidance as the company guided about 11% less than expected.

I don’t think anyone should be surprised at the market reaction because Uber Technologies (NYSE:UBER) has been falling despite the classic beating and raise. Uber has time and again proved that despite always being grouped together, it is a much stronger company. To make sure readers don’t bring up Uber into the discussion, a few reasons why Uber is different: it is showing better FCF, has a much higher market share in U.S, operates in food delivery, and is international.

Getting back to Lyft, going public in 2019, Lyft benefitted from a rare combination of cheaper borrowing rates, gig-economy growth, and general market conditions. I am listing out a few business, fundamental, and technical reasons arguing why Lyft may not just be a bad stock to hold here but may even be in existential threat. Let us get into the details.

What Does Not Kill You Makes You Stronger – Only If You Survive

Yes, I know, the heading above says the same thing twice. But that is intentional and for emphasis. Companies tend to learn and grow as they go through various economic and market cycles. People use examples like Apple (AAPL) and Amazon.com (AMZN) to argue why young companies should not be discarded after a few rough years. This is strong survivorship bias as we talk only about the winners and not the ones that fell by the way side.

To be more specific, Lyft has only operated in favorable economic and market conditions so far. Q4’s net loss of nearly $600 Million does not inspire any confidence that the company can survive long-term in a World (or Country) that is seeing decade high interest rates and is at best, expected to have a mild recession.

Biting The Hand That Feeds

A big part of Lyft’s popularity had and still has to do with the Gig economy. People felt and still feel empowered by the fact that they get to choose when and how they work. “Flexibility” and “Independence” are two key words used by many gig workers. But as highlighted in this (must-ready) interview from a Lyft (and Uber) driver, these two factors come in with a heavy price:

“Flexibility” and “independence” sound nice, but here’s the truth: When you have to work over 50 hours a week to make ends meet, when you have to weigh every hour that you don’t work against the lost income, when you are one accident or illness away from financial ruin, flexibility and independence mean nothing.”

Furthermore, alienating the drivers, the ones who “drive” the business for all practical reasons, is not a smart idea.

“Lyft had unilaterally cut drivers’ rates, forcing me to work longer hours to earn the same amount of money.“

No, Not COVID

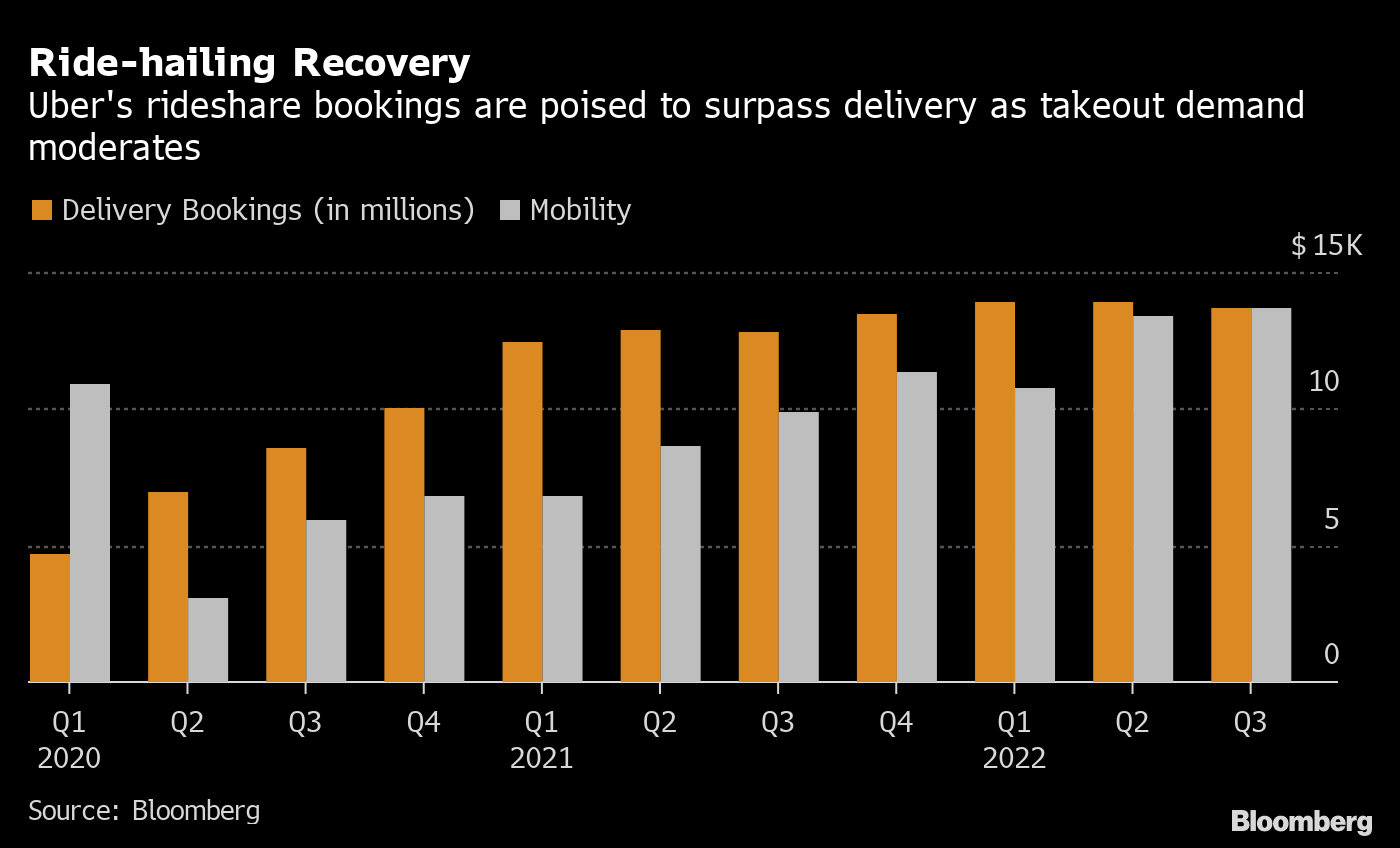

It is easy to blame the post-2020 struggles on COVID but as shown by the two charts below, it is clear that Uber has gone past its pre-COVID numbers in both ride-share and food delivery. But Lyft is still yet to reach its pre-pandemic levels in ridership.

Lyft COVID (Bloomberg.com)

Uber COVID (Bloomberg.com)

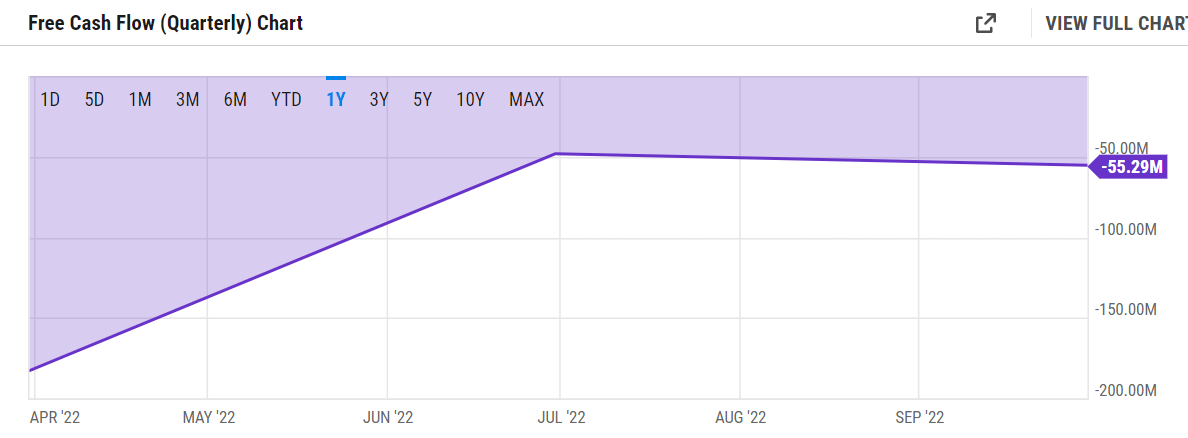

Free Cash Flow – Or Let’s say Free of Cash Flow

I’ve rarely (perhaps never) seen an FCF chart like the one below. I actually thought my screen was flipped or something. No kidding. Then I looked at the actual numbers that produced the chart and there was nothing wrong with my screen. That means there is nothing right with Lyft’s FCF as since going public in 2019, the company has had ONE solitary quarter with positive FCF (~$5M). Before anyone thinks Lyft is just getting started:

- the company has been operating for more than 10 years

- it has been a public company for 4 years.

- free cash flow is much more critical for younger companies as it determines their ability to not just function but to borrow as well.

LYFT FCF (YCharts.Com)

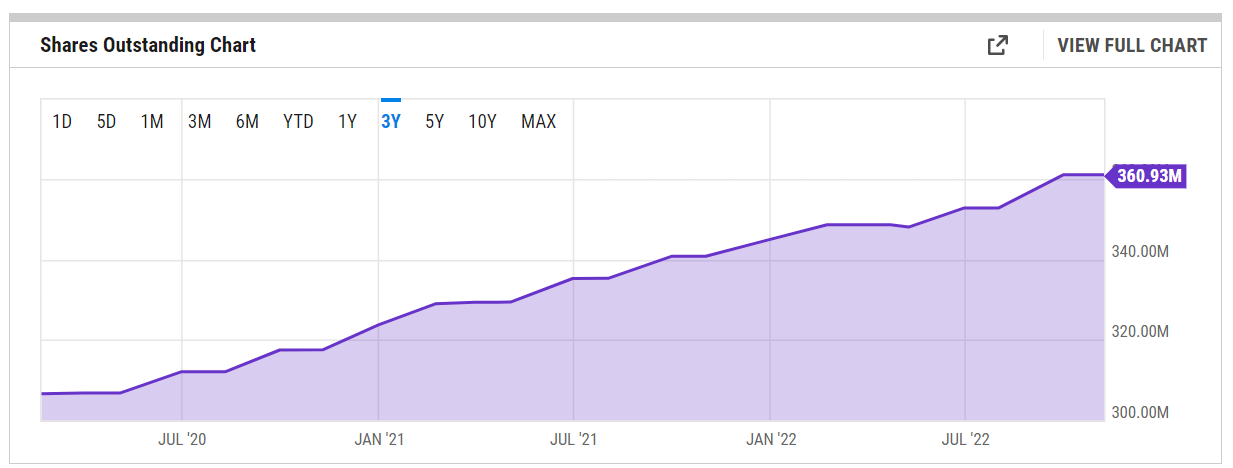

Shares Outstanding Increase

I don’t mean to be insensitive to the losses suffered by Lyft investors as I have some losers still. But these two charts gave me a giggle. The one above and the one below perfectly summarize the fundamental situation with Lyft. Up is down and down is up. What should be going up is going down and what should be going down is going up. Shares outstanding is up 20% in less than two years and once again, no one should be surprised because Lyft attracts its corporate talent with the lure of Restricted Stock Units (“RSUs”). Employees win and shareholders lose.

LYFT Shares (YCharts.com)

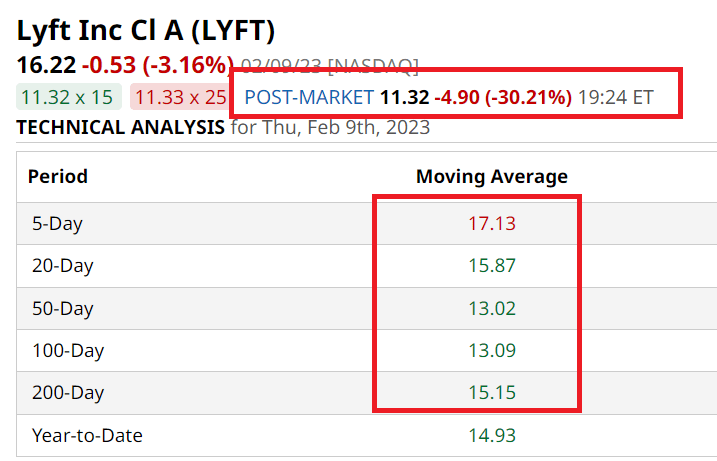

Technical Strength – Turns Into Weakness

The carnage after-hours has taken out one of the few things the stock had in its favor. Lyft’s stock was building up some nice technical momentum as shown by the moving averages below, having taken out even the 200-Day moving average. Alas, with the price slumping to $11.32 as of this writing, expect further downward pressure as both retail and institutional investors digest the numbers. Not to forget, analysts will start throwing their reduced price targets next week.

Lyft Moving Avgs (Barchart.com)

Conclusion

As much as it seems counterintuitive to recommend selling a stock after a 30% post-earnings fall, that seems like the right thing to do given the company’s fundamental struggles and the fact that the stock is still up 15% YTD. Typically, situations like this where a well-known company is struggling to stay alive, the safe bet is that a competitor or a big-fish (Hello Elon) comes in to save the day. But I don’t see either happening with Lyft because Uber’s platform is much stronger and I don’t see why they’d need to step in. High interest rates and general worries about the economy will likely keep the big-fish investors out as well.

In short, Lyft needs a Lift. But is unlikely to get one. It has to survive or sink on its own.

Be the first to comment