buzbuzzer

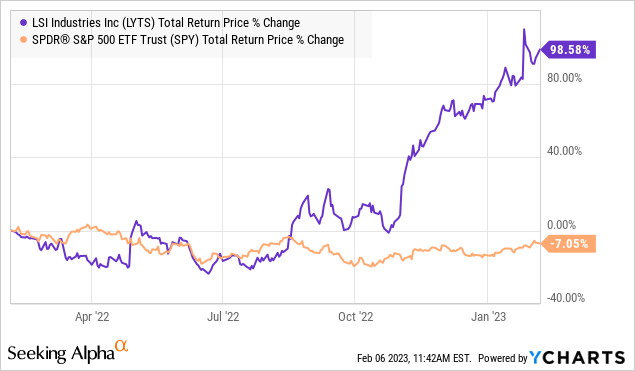

LSI Industries Inc. (NASDAQ:LYTS) is a leader in the segment of industrial and commercial lighting, along with marketing signage solutions utilized by major corporations. We last covered the stock back in 2021, noting an impressive growth outlook based on strong demand for energy-efficient illumination and a shift by customers toward the modernization of retail properties. Indeed, shares of LYTS have been a big winner, nearly doubling over the past year as an outlier compared to the broader market selloff.

Our update today highlights recent developments including the company’s latest earnings report which beat expectations. A new initiative installing solar panel arrays atop retail gas stations represent a new market opportunity the company is pursuing.

We reiterate a bullish long-term view of the stock which checks off several boxes of what we believe to be a high-quality and fundamentally strong small-cap. At its core, LSI Industries has proved capable of successfully executing a growth strategy that remains supported by several market tailwinds. We see more upside going forward.

LYTS Earnings Recap

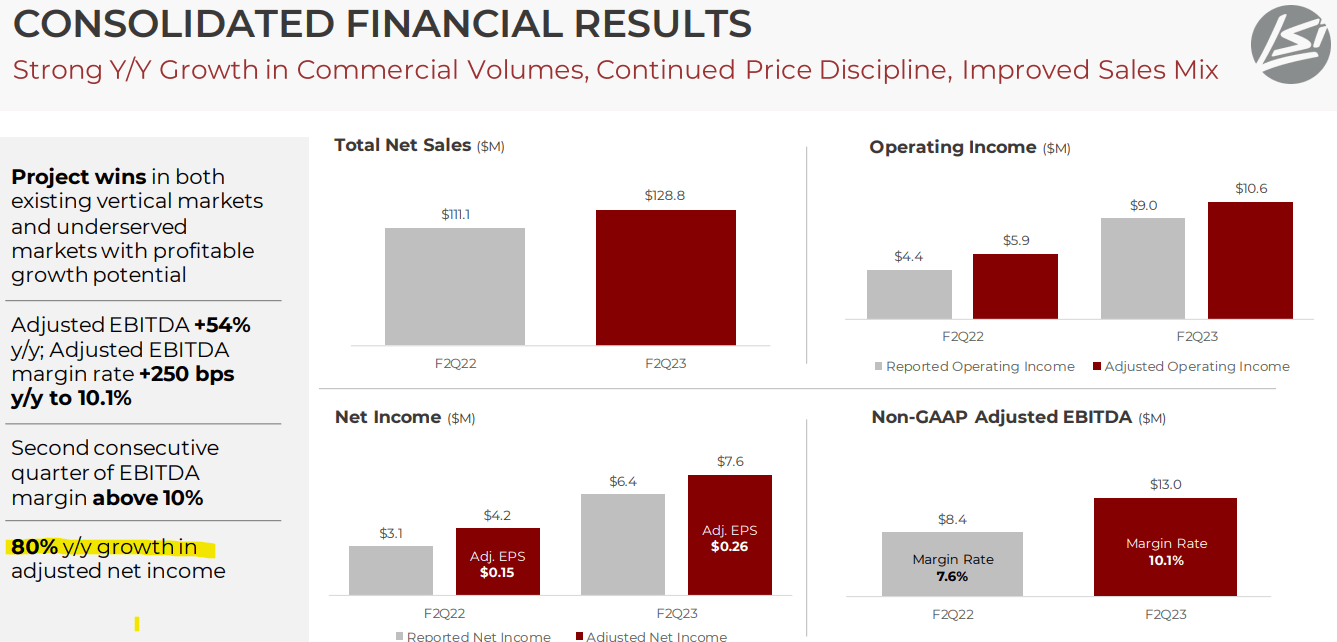

LYTS reported its fiscal 2023 Q2 earnings on January 26th with a non-GAAP EPS of $0.26, $0.09 ahead of estimates. Adjusted net income for the period at $7.6 million was up 80% year-over-year.

The momentum was driven by both the top-line strength with net sales reaching $129 million, up 16% y/y along with firming margins. The adjusted EBITDA margin of 10.1% was up from 7.6% in the period last year.

source: company IR

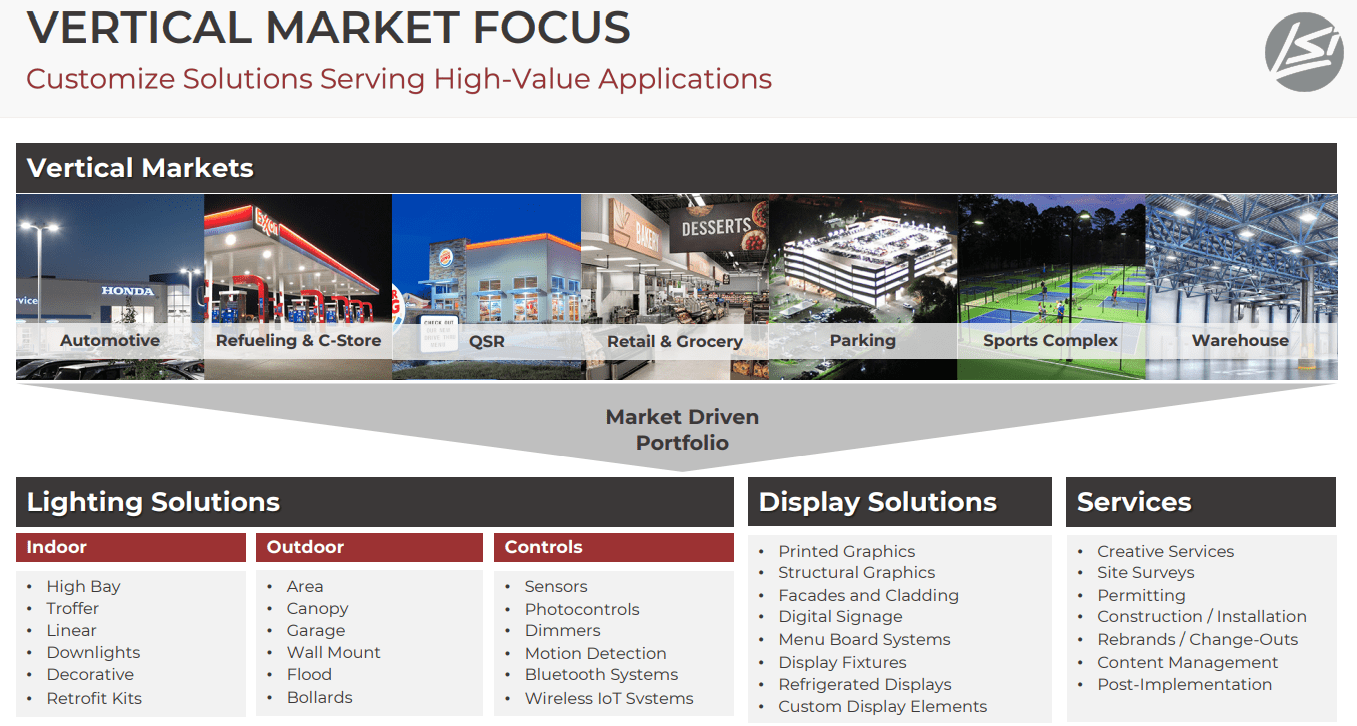

An important theme has been the impact of pricing initiatives implemented last year and overall cost control efforts. Management noted the continued demand in both its core lighting and display segments with sales up 17% y/y and 15% y/y, each respectively. End users in applications at refueling stations, convenience stores, grocery, and general merchandising have been strong points.

source: company IR

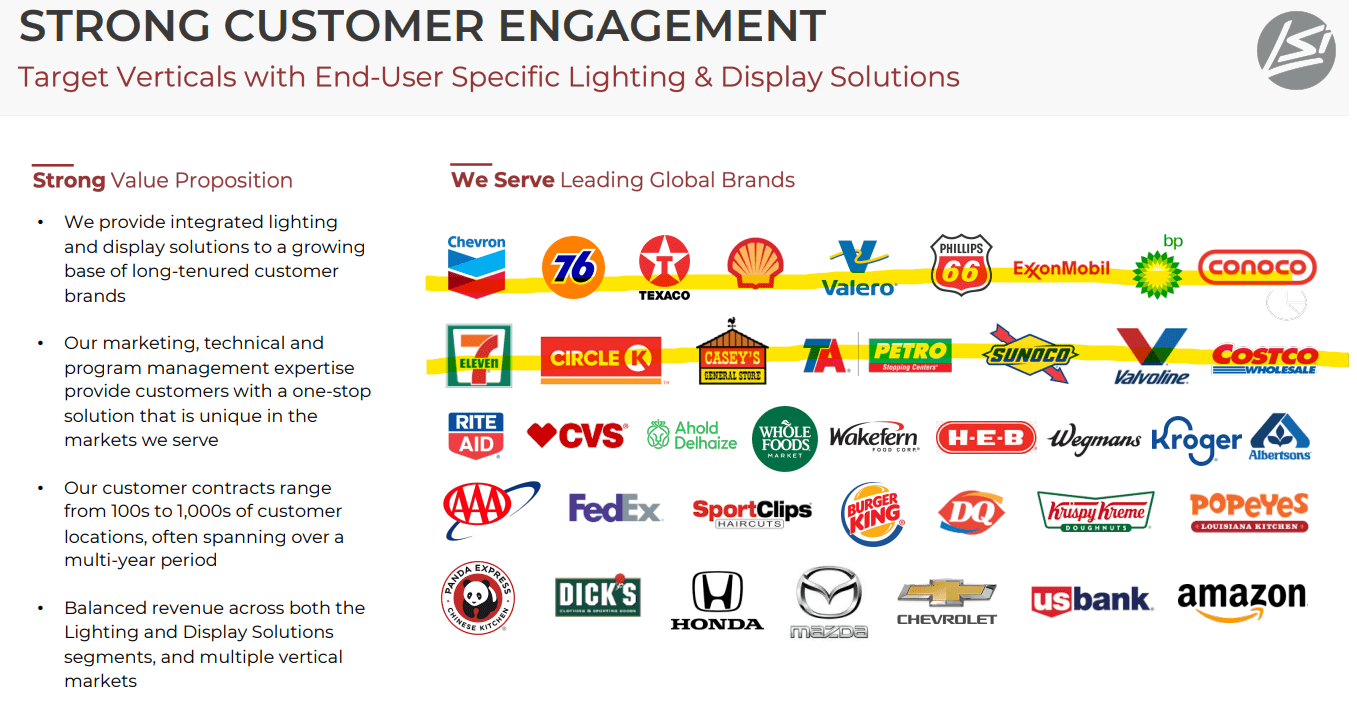

For context, some of the “wins” LSI has been capturing include efforts by customers looking to enhance lighting and signage through renovations as well as in new builds. During Q2, for example, the company completed a $12 million project to update approximately 200 refueling gas stations in Puerto Rico for a major oil company. While not specifically cited, we can connect the dots with news reports of Exxon Mobil Corp (XOM) converting 177 Shell plc (SHEL) gas stations in the region under its umbrella.

On this point, the record year for the energy sector including downstream operations has been a boom for LSI piggybacking on the earnings momentum and investment activities. Beyond ExxonMobil, other global brands that operate or license gas stations are noted as end-users of LSI solutions. This is important as the business relationships support a runway for future engagements as a positive for growth opportunities.

source: company IR

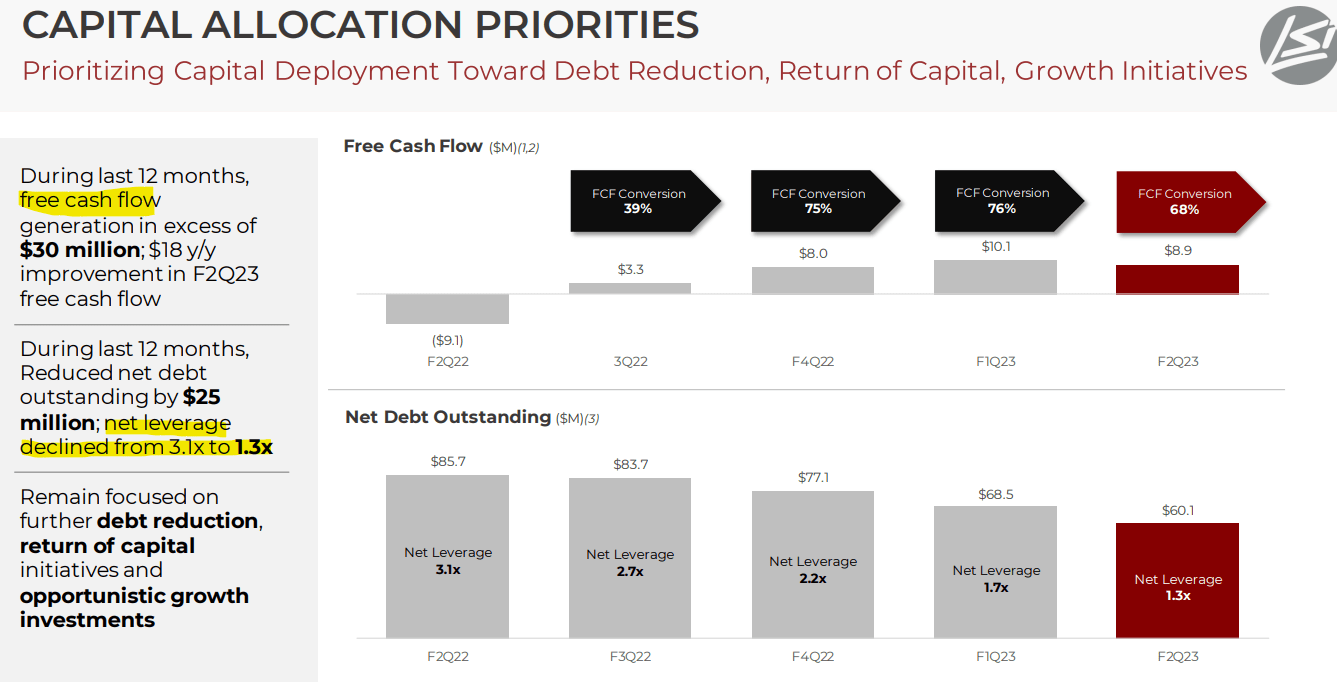

When looking at LYTS, a big development has been the clear shift toward recurring profitability. The company generated $8.9 million in free cash flow in its Q2 and $30 million over the past year. This has provided flexibility for the company to repay debt while investing in more growth. The net leverage ratio reported at 1.3x at the end of the quarter is now down from 3.1x this time last year.

We can also cite the regular quarterly dividend by LYTS at a current rate of $0.05 per share, which yields 1.4%. With EPS of $0.78 over the trailing twelve months, the earnings payout ratio of around 25% is otherwise well supported. While nothing has been announced, we won’t be surprised by a dividend increase in the next year or so as part of the company’s return of capital priority.

source: company IR

LYTS Opportunity In Solar?

One of the messages by management this quarter is that despite the economic backdrop, the company remains optimistic regarding operating conditions into the second half of the fiscal year and the long run.

Beyond the ongoing strength in verticals and applications mentioned above, what’s also interesting is the company’s early steps into solar installations as a turn-key option mounted on top of the gas station and car-wash canopy.

LSI noted the completion of a first-of-its-kind array at a retailer at a “Speedy Stop” refueling and convenience store in August, Texas that is capable of generating upwards of 170 MWh of electricity on an annual basis. The press release noted that the investment by operators can pay for itself within four years.

By this measure, we can start looking at LYTS as a sort of “solar name” capturing ESG trends as a new growth dynamic. This is important considering many of the Federal level tax incentives being pushed into the market since the implementation of the “Inflation Reduction Act” as an opportunity for LSI Industries over the next decade.

The advantage LSI has in this segment relative to competitors is that they already have relationships with the gas station operators from its signage and lighting business. The bullish case for the stock is that these initiatives can accelerate over the next few years.

To be clear, the solar side of the business is still small, but it adds a layer of attraction to the stock that supports both higher growth and even some valuation multiples expansion. There is also a sense that these solutions are in a value-added category of services that should add to the profitability potential. That was also the message from CEO Jim Clark during the earnings conference call:

We see the Canopy at most petroleum retail locations as an untapped opportunity and this project is a good example of how we can turn this unused space into a real profit center for both us and our customers, let alone the environmental impact of the clean energy production. I want to caution everyone that this is simply a first step but it does go a long way into underlining the opportunities and possibilities of expanding products and services we can offer in our various vertical markets.

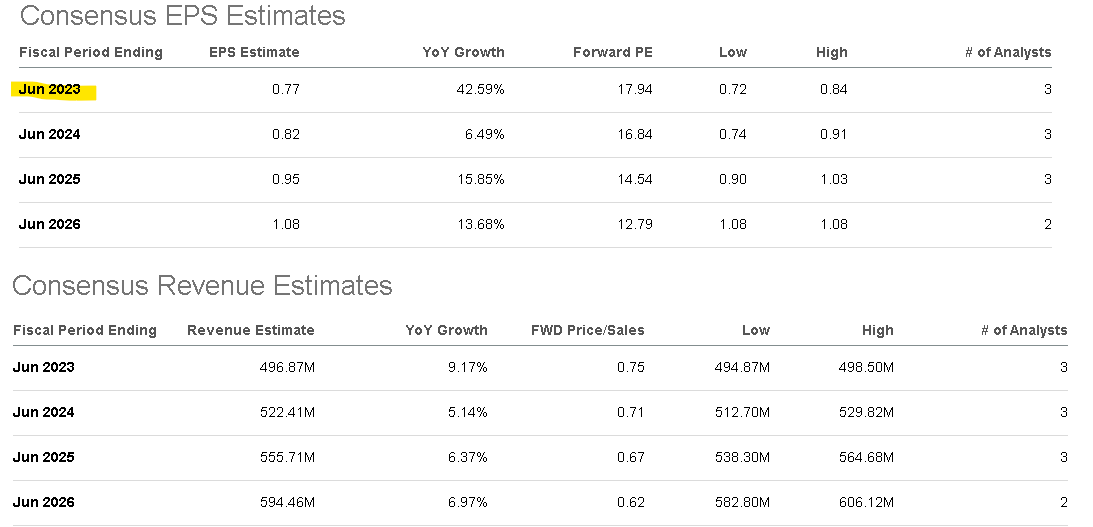

The current market EPS forecast is for fiscal 2023 EPS to reach $0.77, representing a 43% increase over last year. This would be a continuation of the trends observed in Q2 based on firming margins on top of 9% revenue growth for the full year. For 2024, the outlook is for earnings growth to moderate towards 6.5%, against tough comparables while the top line averages growth in the mid-single-digits.

We believe these estimates may prove to be conservative with a bullish case for the stock that the company can outperform based on operating strength and financial execution. In this regard, LYTS trading at an 18x forward P/E multiple is compelling in our view with room for initiatives in solar representing a new growth component. The ongoing deleveraging is also positive for valuations.

source: company IR

LYTS Stock Price Forecast

We rate LYTS as a buy, with a price target for the year ahead at $17.50 representing a forward P/E of 21x on the current consensus EPS of $0.82 for the fiscal year 2024 which is about 16 months away.

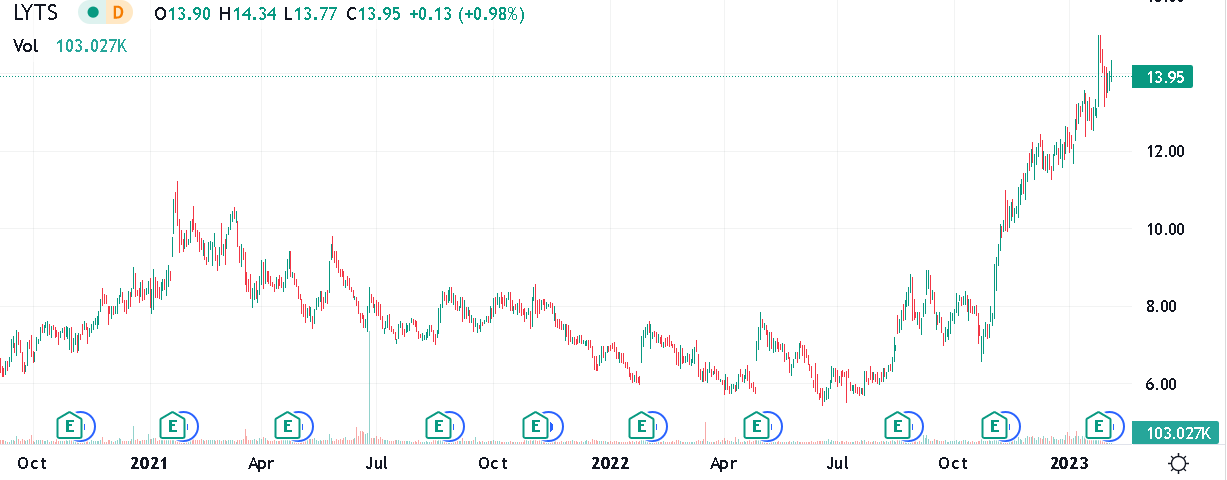

At the same time, it’s important to acknowledge what has already been a breathtaking rally with the stock surging by nearly 100% just since lows in late October. We believe part of that dynamic could be related to the messaging on solar alongside the stronger momentum in the stock market over the period. With a sense that economic conditions can improve going forward, there is a case to be made that LSI Industries’ outlook is stronger today than at any time over the past year.

Into the next few quarters, the EBITDA margin and cash flow trends will be key monitoring points for the stock. The main risk would be for a disappointing slowdown at the top line or a shift into a deeper deterioration of the economy would undermine demand trends and open the door for a leg lower in the stock.

Seeking Alpha

Be the first to comment