jetcityimage

Investment Case

In this article, I’m initiating coverage of my largest individual equity holding Lowe’s (NYSE:LOW). Warren Buffett has often mentioned that good investments should be easy to identify; you don’t need complicated forecasting models or robust technical analysis to find a wonderful business. Finding a wonderful business with effective management at a fair price and buying all you can is more important than predicting where the market will go next. When you see it you’ll know, and I believe this is the case for Lowe’s. Lowe’s is the longstanding #2 in the home improvement retail duopoly but has return potential that is foolish to ignore. The market is undervaluing Lowe’s at current levels, and I am buying all I can while that’s still the case.

Valuation

My valuation for Lowe’s sets a fair value price point at $287.18 and a margin of safety price point at $201.40. I used a Discounted Cash Flow model and took current free cash flow (FCF) levels, FCF growth trends, and the price/FCF multiple to compute conservative estimates of Lowe’s fair value. Lowe’s is down about 8% on the year and is trading at a P/FCF multiple of about 20. The margin of safety price, at which I consider Lowe’s a Strong Buy, assumes a P/FCF of 5. I use a discount rate of 20% annually and the final piece is the expected growth rate of Lowe’s FCF. The 10-year compounded annual growth rate (CAGR) of Lowe’s levered FCF is 10%, so my conservative estimate uses a growth rate of 5% and my fair value estimate uses 10%. In other words, at prices below $201.40, I consider Lowe’s a Strong Buy and at prices below $287.18, I consider Lowe’s a Buy.

I believe that Lowe’s can at least continue growing at the 10-year CAGR historical rate of 10%. In fact, I believe the new management team and refreshed strategy will yield much higher than 10% CAGR over the next 10 years. Marvin Ellison and a number of other relatively new executives have many years of industry experience and are focused on driving value for investors. Cash is being put to good use by buying back shares and paying dividends while re-investing in business systems to increase operating efficiencies and inventory management. In a duopoly, it doesn’t always pay to be the market leader. Lowe’s can learn from the mistakes of The Home Depot (HD) and can generate great returns on the back of effective management decision-making and financial discipline. Lowe’s has momentum and consistent growth in the Pro, ‘Do-it-for-me’ (DIFM) space, which is more recession-proof than the ‘Do-it-yourself’ (DIY) business. Lowe’s still generates roughly 3/4 of sales from their DIY customers, whose demand is more likely to be impacted by inflation and (even the expectation of) a recession. But DIY is a growing segment in its own right. The internet has fueled the rise of the DIYer, and a slowing housing market and increasing inflation are not going to impact this trend in the long run. The shift to DIY is driven by the internet de-mystifying home maintenance and allowing virtually anyone to learn how to do it. Home repairs don’t wait for the recession to end, though consumers may delay certain repair spending, so there’s actually potential for spending to shift from the DIFM category to the DIY category as more consumers try to save money through DIY.

Company Overview

Lowe’s is the second-largest home improvement retailer in the world, operating 1,969 stores in the United States, and is in the process of selling its Canadian locations (RONA, Lowe’s Canada, Réno-Dépôt, and Dick’s Lumber), set to close at the beginning of 2023. This is a step toward simplifying Lowe’s business model but does provide a good case study into poor capital allocation. The deal for the four brands guarantees only $400M for Lowe’s, who bought Rona in 2016 for roughly $2.4B. This is reflected in the $2.1 non-common asset impairment that was recently written off. The mistakes of the past ought to be learned from and left in the past, and the decision to sell at a loss may have been tough but we believe a simplification of a business model is good. Management that’s focused on driving value in the US market, which makes up a majority of total sales, is good. Lowe’s stores offer products and services for home decorating, maintenance, repair, and remodeling, with maintenance and repair accounting for two-thirds of products sold. Lowe’s targets retail do-it-yourself (around 75% of sales) and do-it-for-me customers as well as commercial and professional business clients (around 25% of sales). I estimate Lowe’s captures a low-double-digit share of the domestic home improvement market, based on U.S. Census data and management’s estimates for market size. A combination of organic market growth and growing market share are key components in the formula for the excellent investment opportunity presented.

Competition

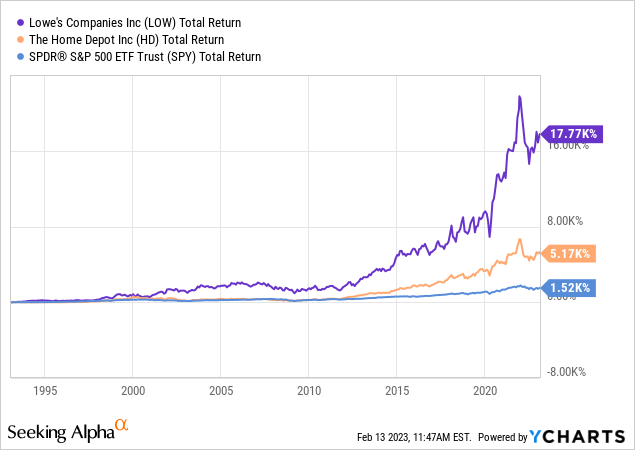

Lowe’s foremost competitor is The Home Depot. HD is clearly the market leader, but Lowe’s is a formidable opponent and is set to benefit from the effective execution of management strategy and modernization of technology. An investment in Lowe’s first needs to pass the hurdle of HD. The first question for any investor ought to be ‘Do I expect Lowe’s to outperform The Home Depot, and why?’ Any investment case that doesn’t directly address this question is flawed from the start. I found the best answer to that question here, in what was one of the most informative and helpful investment articles I’ve ever read. Although both Lowe’s and The Home Depot are wonderful businesses, LOW has historically outperformed HD, why?

Strong (and getting stronger) dividend growth, consistent earnings growth, and an overall wonderful business. Further, LOW share buybacks have outpaced HD and LOW has a really solid payout ratio. Despite HD showing stronger retail sales per square foot, the average Lowe’s customer spends more per visit. This shields Lowe’s a bit more than Home Depot from a slowdown in traffic. The macro risks both companies face are the same, with relatively high debt burdens (making shareholder equity negative), a cooling housing market, and inflationary pressures. The key to my investment case in Lowe’s is the modernization of systems. In the modern world, effective management is synonymous with the sensible collection and use of data. Lowe’s is set to modernize 90% of its operating systems by 2024 and 100% by 2025. Equipping store associates with better technology and modernized systems not only drives efficiency in operations but also allows for higher-quality inventory data which empowers management to make more informed inventory decisions. In a market with big-ticket purchases like appliances and bulk purchases of construction materials, effective inventory management is key to driving growth. The future earnings growth of Lowe’s may not be driven entirely by top-line growth but by expense reduction. Lowe’s may not have the upside potential it did 30 or 40 years ago, but they have a robust network of stores and are driving value by increasing operating efficiency, improving inventory management, and becoming more focused by cutting out the Canada business. While Home Depot is focusing on its Mexico and Canada operations, which make up 13.5% of total stores, Lowe’s is now laser-focused on the US market which has roughly a $900B-$1T addressable market in its own right. There’s plenty of room to grow right here at home, and Lowe’s looks better positioned and more focused than The Home Depot to continue growing and generating market-beating returns.

Risk

Lowe’s has a lot more debt than cash on hand. Typically, I’m apprehensive of any company where this is the case. The bulk of the debt is in the form of notes payable maturing from 2027-2031, which gives Lowe’s a sufficient amount of time to ensure it’s covered. At worst, the debt will impact share repurchases or dividends, and at best it will have a menial overall impact.

There is also the risk of a broad-based reduction of consumer demand and purchasing power, which of course does not bode well for Lowe’s topline growth. This impacts Lowe’s and Home Depot, and other home improvement retailers, the same. We still believe Lowe’s is the best home improvement retailer, but a drawdown of consumer demand may decrease the relative attractiveness of Lowe’s compared to companies in other sectors. I will be monitoring each earnings report and will read the 2023 annual report to develop a refreshed investment outlook for Lowe’s to ensure I’m only invested as long as I believe the long-term growth outlook is robust.

Conclusion

In the pursuit of consistently beating the market, discipline is key. Lowe’s management is enforcing discipline with ambitious share buybacks and dividend growth, so it’s only a matter of investor discipline to reap the rewards. I initiated a position in Lowe’s at $212.28 and plan to stick around for a while.

Be the first to comment