jetcityimage

Lowe’s (NYSE:LOW) has held up remarkably through the market gyrations over the past several years. With people making home improvements to enhance the work-from-home home experience, and the surge in home buying with record low interest rates, LOW has been one of the beneficiaries coming out of COVID. Even with challenges from managing inflation, rising wages, and supply chain constraints LOW has done well. LOW has returned a total of -6.5% over the past 12 months, as compared to -8.1% for home improvement retailers as a group (as tracked by Morningstar) and -7.7% for the S&P 500. Over the past 3 years, however, LOW has dramatically outperformed, with annualized total return of 21.6% per year vs. 14.8% per year for the home improvement retail industry, and 8.6% per year for the S&P 500 (SPY).

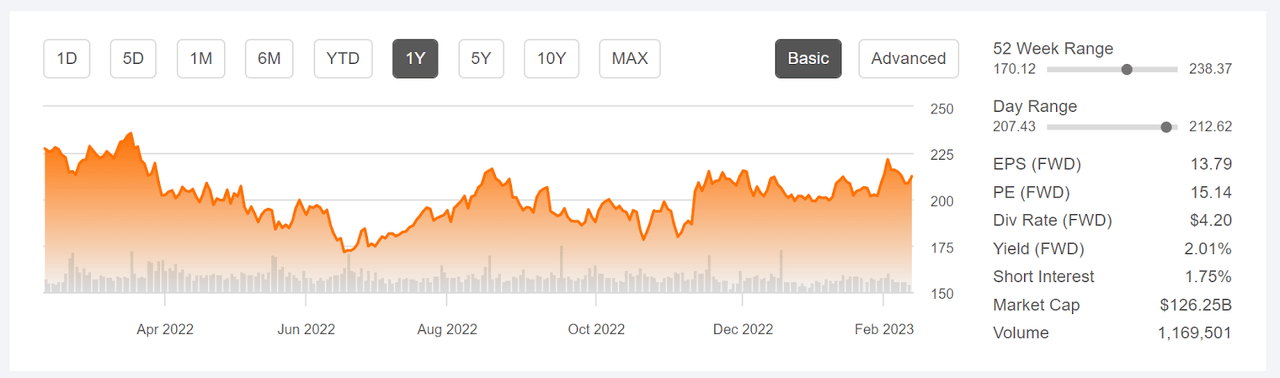

12-Month price history and basic statistics for LOW (Seeking Alpha)

LOW’s earnings history shows the substantial growth that corresponded to COVID and its aftermath. LOW has beaten expectations on EPS for all but 1 of the last 12 quarters. The consensus outlook for EPS growth over the next 3 to 5 years is 19% per year.

Trailing (4 years) and estimated future quarterly EPS for LOW. Green (red) values are amounts by which EPS beat (missed) the consensus expected value (ETrade)

LOW’s TTM P/E is 15.8, with a forward P/E of 15.1. These values are in the low range of P/E values over the past 10 years. The current valuation looks very reasonable, especially relative to the consensus outlook for earnings growth.

While rising interest rates and a slowing housing market have the potential to impact LOW’s sales, management communicated confidence in ongoing growth in home improvement spending. CEO Marvin Ellison has stated that the 3 most significant predictors of home improvement spending are home price appreciation, the age of houses, and disposable income. With many homeowners having seen a surge in home equity in the past several years, people have both an incentive to maintain their investment and the resources to do so. He also noted that the average age of American homes is around 40 years, so there will be considerable ongoing need for updates and repairs. Another important driver of home improvement spending is that families are more likely to improve their existing homes rather than selling one and buying another, not least because many homeowners have low mortgage rates that are no longer available.

I last wrote about LOW on June 7, 2022, about 8 months ago, and I reiterated a buy rating on the stock. From the market close on that date until today, LOW has returned a total of 10.4% vs. 0.2% for the S&P 500 (SPY). For my June 7 post, the Wall Street consensus rating was a buy, with a consensus 12-month price target that corresponded to an expected total return that was 22% to 29% over the next year, varying based on the source of the consensus outlook. The market-implied outlook, a probabilistic price forecast that represents the consensus view from the options market, was slightly bullish for the 7.45-month period from June 7, 2022 to January 20, 2023, with expected volatility of 34% (annualized). As a rule of thumb for a buy rating, I want to see an expected total 12-month return that is at least ½ the expected volatility (34%). Taking even the low end of the Wall Street consensus at face value, LOW exceeded this threshold. Along with the positive outlooks, LOW’s valuation was reasonable, with a P/E of 15.9.

For readers who are unfamiliar with the market-implied outlook, a brief explanation is needed. The price of an option on a stock reflects the market’s consensus estimate of the probability that the stock price will rise above (call option) or fall below (put option) a specific level (the option strike price) between now and when the option expires. By analyzing the prices of call and put options at a range of strike prices, all with the same expiration date, it is possible to calculate the probable price forecast that reconciles the options prices. This is the market-implied outlook. For a deeper discussion than is provided here and in the previous link, I recommend this outstanding monograph published by the CFA Institute.

As we have now passed the period for which the previous outlook was calculated, I have generated updated market-implied outlooks for LOW and I have compared these with the current Wall Street consensus outlook in revisiting my rating.

Wall Street Consensus Outlook for LOW

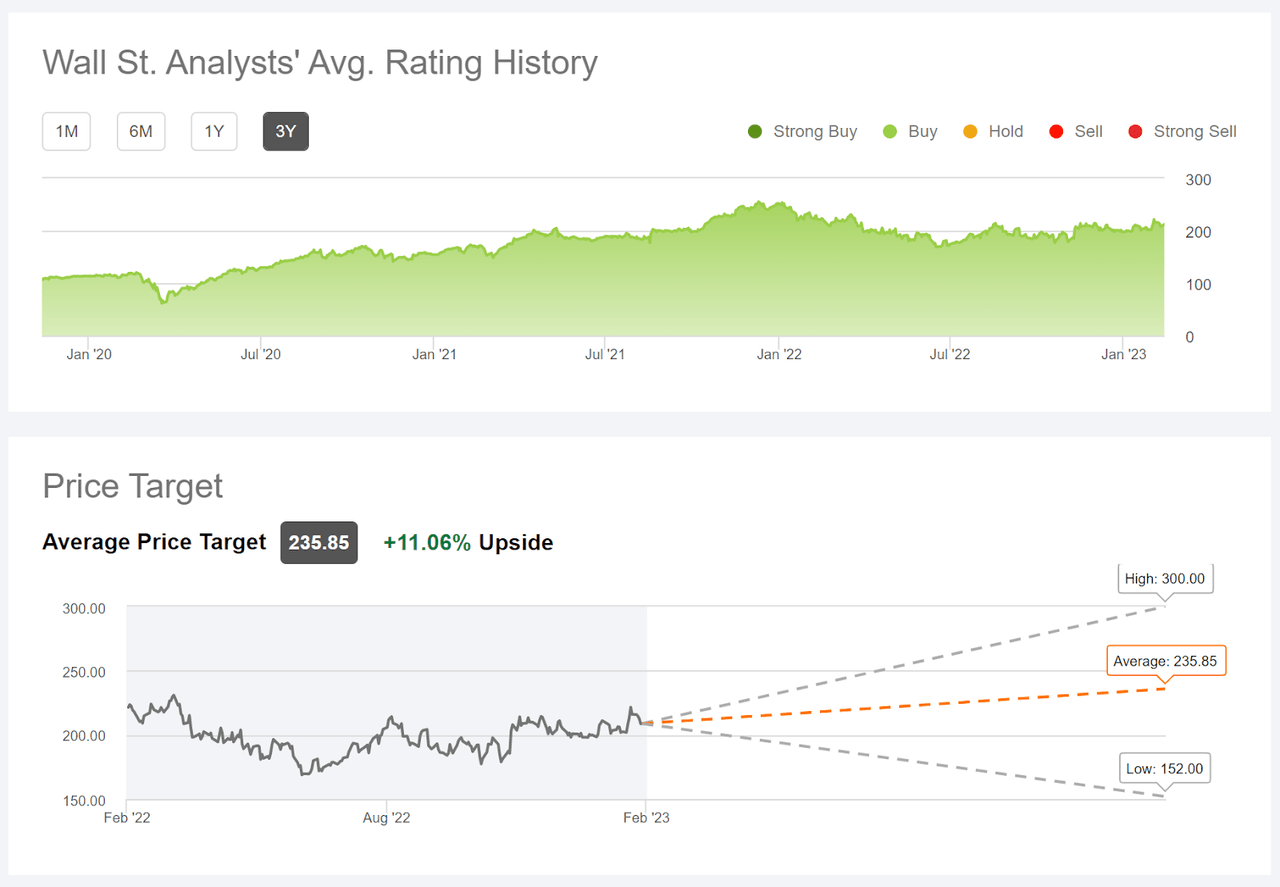

Seeking Alpha calculates the Wall Street consensus outlook for LOW by combining the views of 34 analysts who have published price targets and ratings within the past 90 days. The consensus rating is a buy, as it has been for all of the past 3 years. The consensus 12-month price target is 11.1% above the current share price, which corresponds to an expected total return of 13.1% over the next year. The spread among the individual analyst price targets is a bit too high for comfort, indicating a wide range of opinions and reducing the likely predictive value of the consensus. As a rule of thumb, I discount the consensus price target when the highest individual price target is more than twice the lowest. In the case of LOW, this ratio is 1.97.

Wall Street analyst consensus rating and 12-month price target for LOW (Seeking Alpha)

I often look at more than one version of the Wall Street consensus, as they can differ to a meaningful degree. ETrade’s version of the Wall Street consensus is generally consistent with Seeking Alpha’s, with a buy rating and a wide dispersion among analyst opinions.

Market-Implied Outlook for LOW

I have calculated the market-implied outlook for LOW for the 4.1-month period from now until June 16, 2023 and for the 11.2-month period from now until January 19, 2024, using the prices of put and call options that expire on these dates. I selected these specific expiration dates to provide a view to the middle of 2023 and through the entire year.

The standard presentation of the market-implied outlook is a probability distribution of price return, with probability on the vertical axis and return on the horizontal.

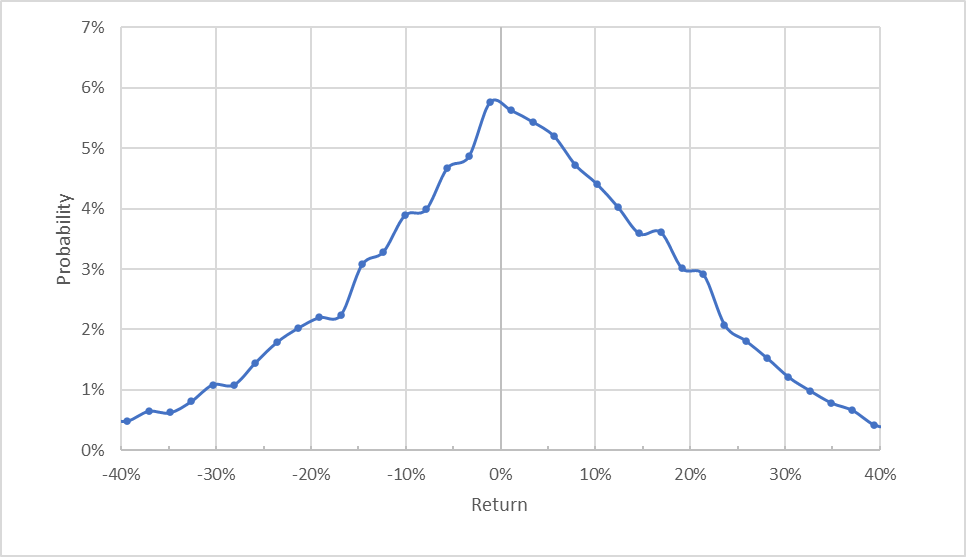

Market-implied price return probabilities for LOW for the 4.1-month period from now until June 16, 2023 (Author’s calculations using options quotes from ETrade)

While the maximum probability corresponds to a price return that is very slightly below zero, the shape of the distribution favors positive returns over this period. Compare, for example, the probability of having a +10% return to that for a -10% return. This asymmetry in probabilities suggests a bullish tilt. The expected volatility calculated from this distribution is 32.4% (annualized), very close to the value that I calculated back in June. For comparison, ETrade calculates implied volatility of 32% for the options expiring on June 16, 2023.

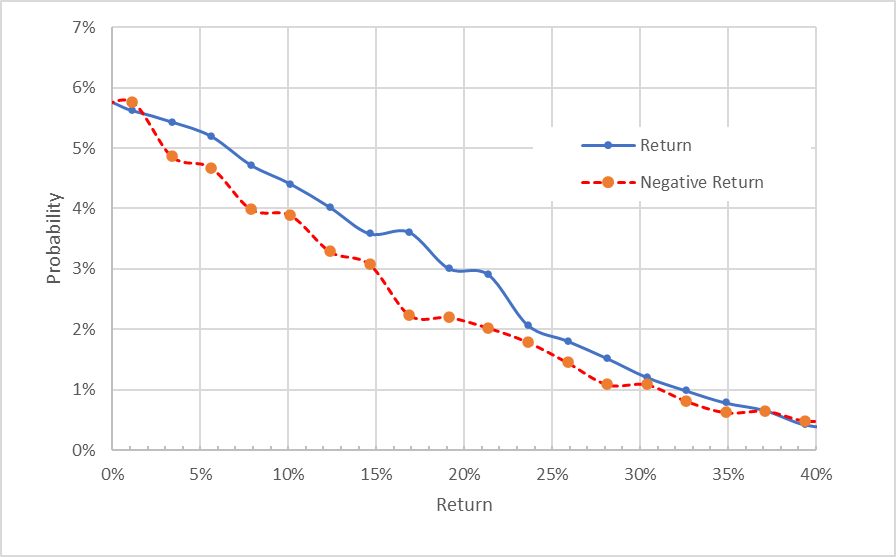

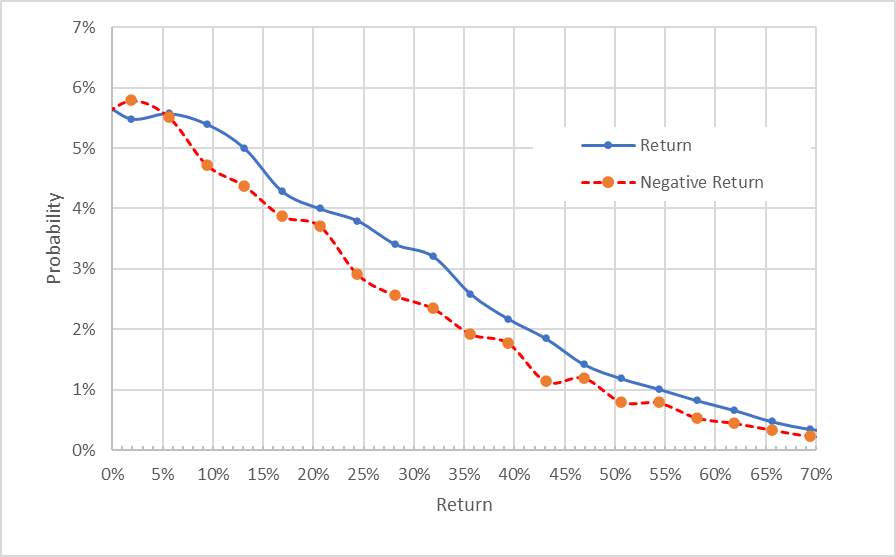

To make it easier to compare the relative probabilities of positive and negative returns, I rotate the negative return side of the distribution about the vertical axis (see chart below).

Market-implied price return probabilities for LOW for the 4.1-month period from now until June 16, 2023. The negative return side of the distribution has been rotated about the vertical axis (Author’s calculations using options quotes from ETrade)

This view shows that the probabilities of positive returns are consistently higher than the probabilities of same-size negative returns, across almost the entire range of possible outcomes (the solid blue line is above the dashed red line over almost the entire chart above). This is a bullish outlook.

Theory indicates that the market-implied outlook is expected to have a negative bias because investors, in aggregate, are risk averse and thus tend to pay more than fair value for downside protection. There is no way to measure the magnitude of this bias, or whether it is even present, however. The expectation of a negative bias reinforces the bullish interpretation of this outlook.

The market-implied outlook for the 11.2-month period from now until January 19, 2024 also exhibits a marked shift in probabilities favoring positive returns. The expected volatility calculated from this distribution is 30.6%. This is a bullish outlook into early 2024.

Market-implied price return probabilities for LOW for the 11.2-month period from now until January 19, 2024. The negative return side of the distribution has been rotated about the vertical axis (Author’s calculations using options quotes from ETrade)

The market-implied outlooks to the middle of 2023 and into the start of 2024 have a bullish tilt, with expected volatility that falls from about 32% in the first half of the year to around 30% for the longer period. These outlooks are more bullish than the result from June.

Summary

Lowe’s has performed admirably over the past several years and the outlooks are quite favorable over the next year. Earnings are expected to grow at a solid rate going forward. Even if the housing market continues to slow, homeowners are more likely to improve their current dwellings rather than giving up their low mortgage interest rates in the process of moving to new properties. The Wall Street consensus rating for LOW continues to be a buy, as it has been for all of the past 3 years. The consensus 12-month price target corresponds to expected total return of 13.1%, slightly below ½ of the expected volatility (30%-32%), the threshold that I want to see for a buy rating. The market-implied outlooks for LOW are bullish to the middle of 2023 and to the start of 2024, with moderate volatility. I am maintaining a buy rating on LOW.

Be the first to comment