ipopba/iStock via Getty Images

Revenue in the third quarter came in at a record for LiveVox Holdings, Inc. (NASDAQ:LVOX), even in an unfavorable economic climate.

Some of the positive catalysts in the reporting period were margin growth from its public cloud infrastructure, and increasing revenue in AI and digital, along with an increasing usage from the normalization of the credit cycle, albeit at a slower pace than the company had expected.

Based upon data from Moody’s Analytics and the New York Fed, there is an increase in the number of first-party delinquencies that will be a tailwind for the company going forward.

In the near and long-term, it looks like company growth will be largely determined by the increase in upsells and lengthening sales cycles with new logos.

TradingView

With the company share price recently jumping, it appears to me it may be getting ahead of itself, and investors would probably be wise to wait for it to correct before taking a position.

In this article, we’ll look at some of the company’s recent performances and how it is probably going to perform over the next year or so.

Latest numbers

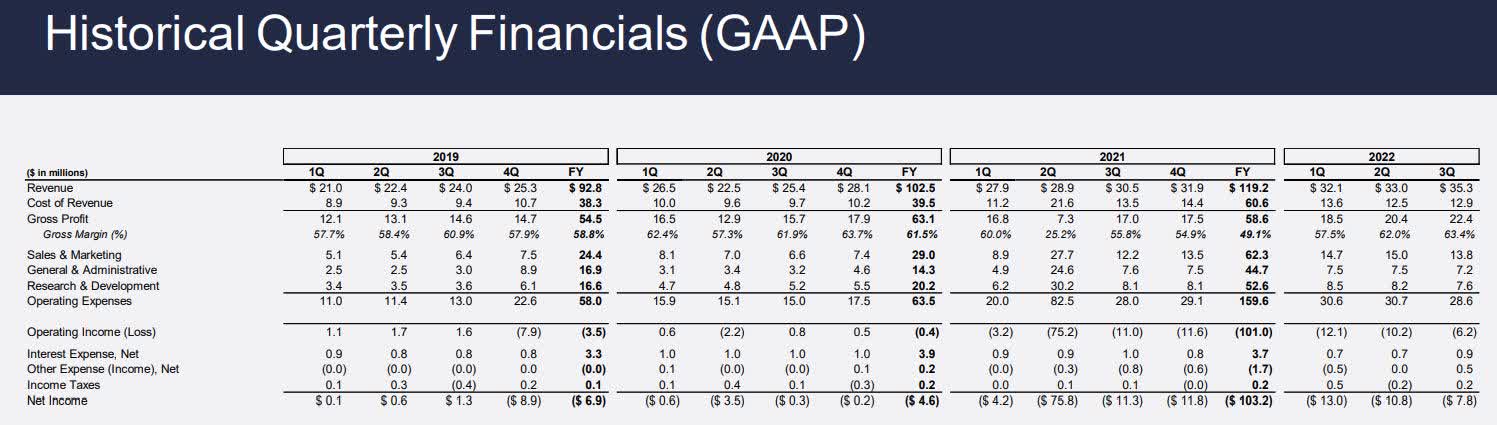

Revenue in the third quarter of 2022 was $35.3 million, up 16 percent from the $30.5 million in revenue generated in the third quarter of 2021. Revenue in the first nine months of 2022 was $100.3 million, compared to revenue of $87.4 million in the first nine months of 2021.

Contract revenue in the third quarter of 2022 was $28 million, up 21 percent year-over-year and five percent sequentially. Revenue from excess usage was $7.3 million, down three percent year-over-year, and 17 percent sequentially.

Investor Presentation

Adjusted EBITDA in the third quarter was negative $(1.5) million, up $4.1 million from the prior quarter. That was attributed to an improvement in adjusted gross margin of $2.2 million and a $1.9 million improvement in operating expenses.

Investor Presentation

Gross margin was 66.3 percent in the quarter, beating guidance. That was attributed to the company now having moved 100 percent of its customer base to the public cloud.

Net loss in the reporting period was $(7.8) million or $(0.08) per share, compared to a net loss of $(11.3) million in the third quarter of 2021. Net loss in the first nine months of 2022 was $(31.5) million or $(0.34) per share, compared to a net loss of $(91) million or $(1.20) per share in the first nine months of 2021.

Cash and cash equivalents at the end of the third quarter of 2022 were $22.6 million, down approximately $25 million from the $47.2 million in cash and cash equivalents at the end of calendar 2021. At the end of the reporting period the company held debt of $55 million.

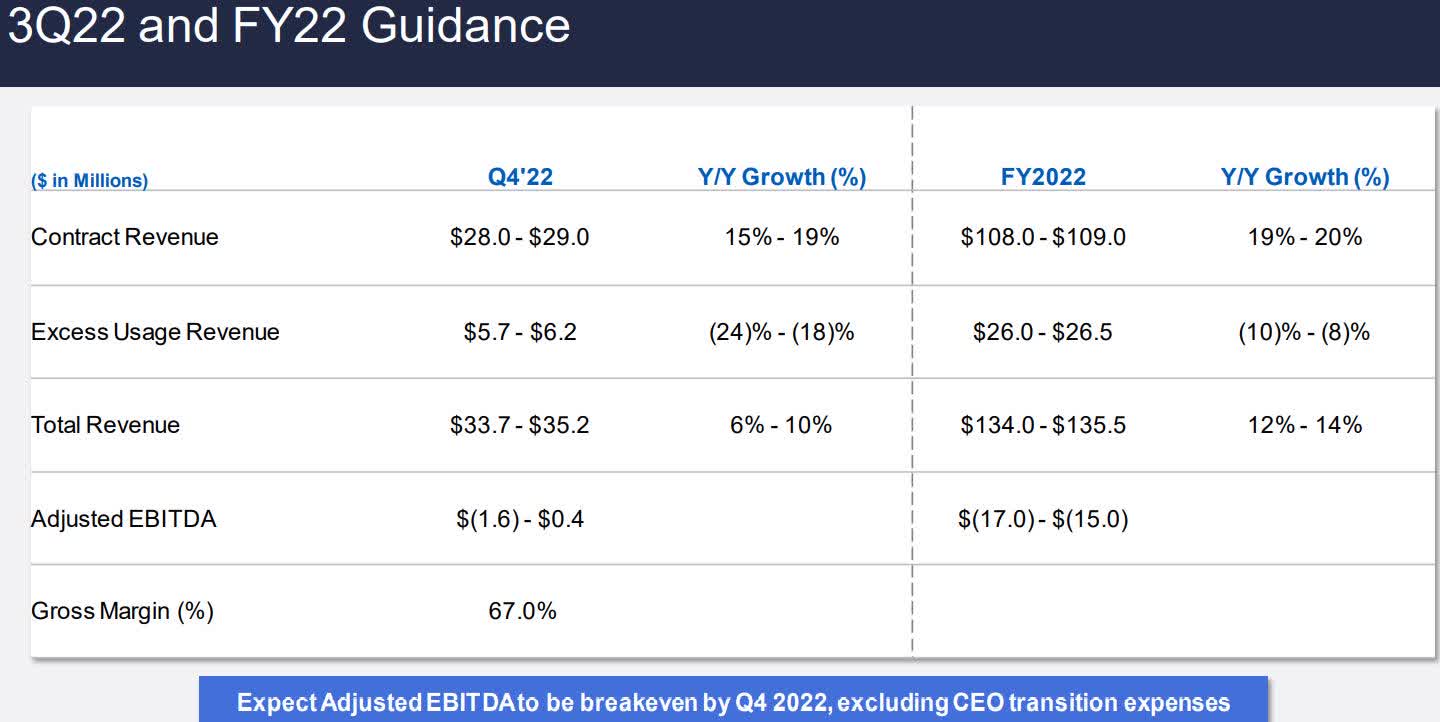

Revenue guidance for the fourth quarter is from $32 million to $33.7 million, with approximately $28 million to $29 million coming from contract revenue. Full-year revenue is projected to come in at $134 million to $135.5 million, which would be up 14 percent year-over-year.

Upsells and new logos

In the near term LVOX has a lot of potential to drive significant revenue from upselling its existing customer base, with the company estimating it could drive as much as $2 billion revenue from the upsells.

Not only is that a nice increase in revenue, but it also would do so at a quicker pace than new logos would in the current economic environment.

As for new logos, the pipeline of the company is up 34 percent year-over-year, but macro-economic conditions have resulted in the lengthening of the sales cycles of new logos, which means it’s going to take longer to have an impact on the performance of LVOX.

When asked about the elongation of the sales cycles, management said it could be as long as twice what it has been over the last “year or two.”

A couple of big new logo wins the company revealed in the third quarter were a subprime auto lender and a large BPO customer that has approximately 10,000 agents around the world.

As for upsells, among the largest in the reporting period was in the travel and tourism industry. The other major upsell in the third quarter came from one of its largest customers, but it wasn’t revealed what sector it competed in.

Conclusion

There have been some improvements in the performance of the company now that it has moved 100 percent of its customers to the public cloud, specifically in gross margin and adjusted EBITDA.

Yet even with some of the tailwinds mentioned by the company, including increasing usage from credit cycle normalization, it’s still doing so at a slower rate than the company anticipated, which when combined with lengthening sales cycles with new logos, it points to a lot of heavy lifting in upsells for the company to generate meaningful revenue growth over the next year. If it can successfully leverage its public cloud infrastructure it should be able to further boost AI and digital revenue, as the opportunity in agent automation is huge, according to management.

But taken as a whole, it looks to me like LVOX is going to struggle to gain momentum in 2023. What could change my thesis is if the company is able to significantly increase upsells in the near term, which would fairly rapidly boost the top and bottom lines of the company.

As for new logos, that is a solid tailwind for the long-term, but it’s not likely to have a lot of impact on the company’s performance in 2023, especially in the first half.

And as mentioned earlier in the article, the company’s share price has jumped over the last few days, and it would probably be best to wait for a pullback before taking a position, for those that like the future potential of LVOX.

Be the first to comment