solarseven

TLT: Well-Positioned To Recover In 2023

As we ended 2022’s trading yesterday (December 30), it may be opportune for investors to consider a position in the iShares 20+ Year Treasury Bond ETF (NASDAQ:TLT).

TLT is a long-duration Treasury bond ETF battered in 2022 as the Fed went on a rate hike rampage.

Media headlines have been promulgating the most well-communicated recession in recent times, as the Fed is expected to remain hawkish through 2023.

The inverted yield curve has narrowed to -55 bps from a record low of nearly -85 bps in early December. Equity strategists and economists have sparred over whether we could enter a recession. And if we do, how deep could it be? Fed Chair Jerome Powell did not rule out a recession in 2023 at the recent December FOMC conference, even though its summary of economic projections stated a 0.5% median GDP growth estimate. Despite that, Powell reminded investors that it’s impossible to know in advance whether we could have a recession.

Still, the S&P 500 (SPX) (SPY) has shrugged off the market’s pessimism, as it has likely baked in a mild-to-moderate recession at its October lows. Moreover, the inverted yield curve, which has consistently predicted a recession historically, has also pointed in the same direction.

Moreover, The Conference Board Index of Leading Economic Indicators (LEI) has continued to fall further, increasing the risks of a near-term recession. Even the usually bullish strategist Edward Yardeni suggested that “if there’s going to be a recession, it’s going to be soon, and that’s what the markets fear.”

TLT: A Recession Is Not Guaranteed. But It’s Ok

Notwithstanding, Yardeni also articulated that the yield curve inversion may not indicate a recession this time. He accentuated that he has yet to glean signs of a “widespread credit crunch” caused by the Fed’s tightening, leading to a recession. He also reminded investors that the financial system is much more robust following the Global Financial Crisis (GFC) in 2007/08. Hence, Yardeni argued this “this time may be different”:

There certainly have been meltdowns in cryptocurrencies, private equity, and the ARK, meme, and SPAC stocks. But none of these developments has turned into a widespread credit crisis. So this time, the inverted yield curve may be signaling that inflation has likely peaked and will continue to moderate. – Yardeni Research, December 5 Briefing (registration needed)

In addition, interest rate strategists have also put forward their 2023 projections, with most suggesting lower 2Y Treasury yields as the Fed reacts to a slower economy.

Even the strategists from Goldman Sachs (GS) who penciled in the highest 2Y yield forecast at 4.6%, is below the Fed’s median forecast of 5.1% for its Fed funds rate (FFR) by the end of 2023.

Therefore, is there going to be a recession or no recession? It depends on whether you trust the yield curve’s historical potency or follow Yardeni’s take on a potential soft landing.

But does it matter to the TLT? In both cases, the TLT should benefit whether we are going into recession. Why? Strategists still expect the Fed to move earlier than anticipated to cut rates whether the economy falls into recession.

The strategists anticipating a recession expect the Fed to pivot faster, as Deutsche Bank (DB) highlighted: “US recession and Fed rate cuts will bring a steeper curve.” As a result, DB strategists’ forecast suggests a 2Y yield of 3.15% by the end of 2023, down from the current 4.43%.

However, GS strategists who don’t expect a “deep” recession believe that “inflation will be sticky, requiring restrictive policy for longer.”

Notwithstanding, both sides of the house expect a lower 2Y rate, suggesting that the economy will likely weaken further (deep recession or not).

And that’s good for the TLT because of the battering it has received over the past year as long-term rates surged. But, given its long-duration configuration, it has also caused tremendous volatility for investors.

However, with macroeconomic headwinds intensifying, we are more confident that the Fed will unlikely raise rates beyond its 5.1% median FFR target. Coupled with potentially lower inflation rates moving ahead, long term bonds should not see higher yields above their October highs. But is there a guidepost to ascertain that the thesis remains intact?

TLT: Bond Sellers Are Still In Control

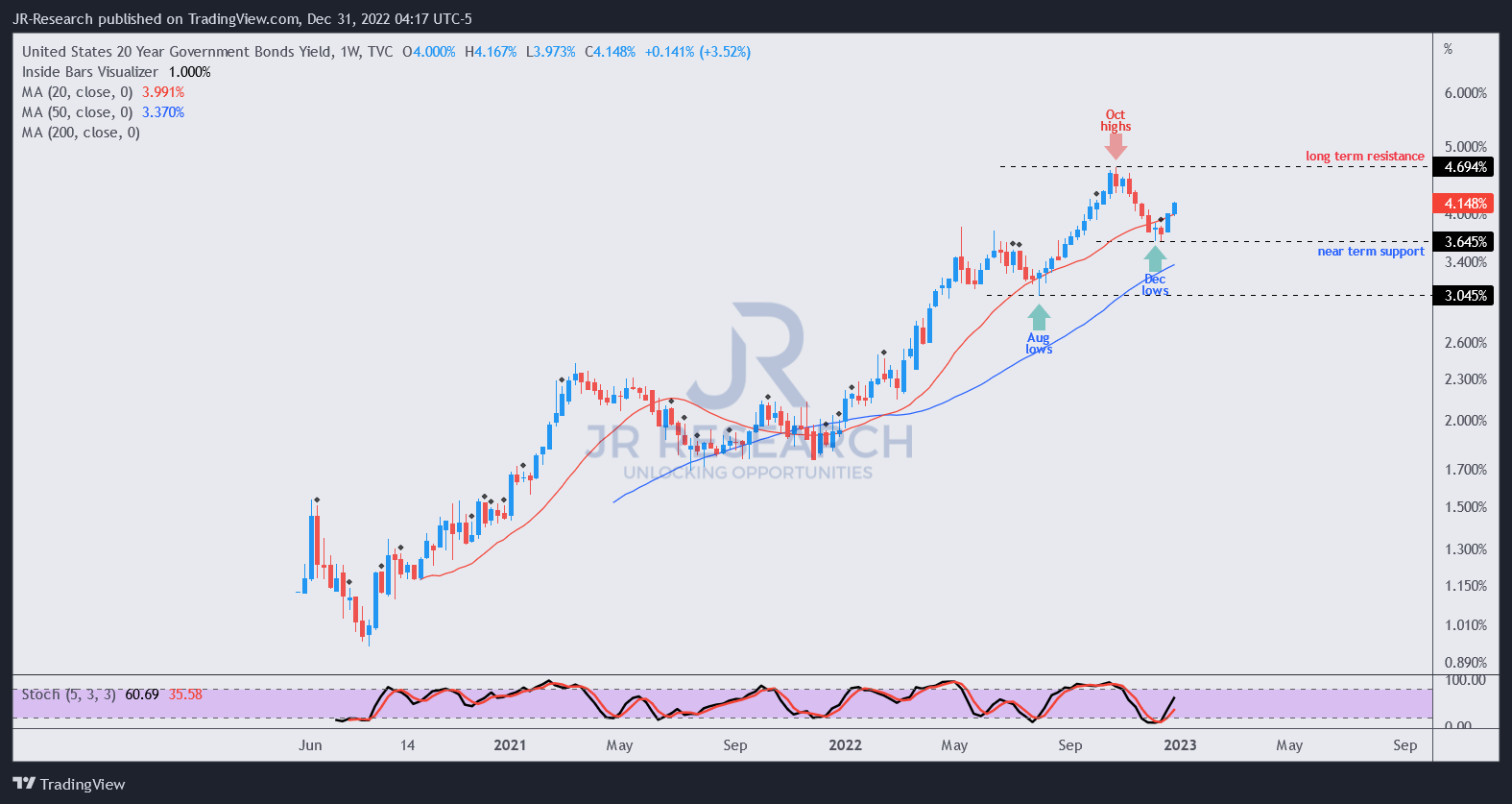

US20Y yield % price chart (TradingView)

As seen above, the 20Y yield formed a bottom in early December, pulling back from a medium-term uptrend as bond sellers returned to prevent further downside.

The bottoming of the 20Y yield also preceded the SPX’s December top post-FOMC conference. Therefore, the price action between the S&P 500 and the bond markets is still positively correlated, as bond sellers remain in control.

But, investors shouldn’t be stunned by such a performance in 2022, given the macro uncertainties and still elevated inflation. Deutsche Bank also accentuated that:

During periods of higher inflation and inflation uncertainty, bond and equity returns tend to be positively correlated. This reduces the hedging benefits of bonds, and bond risk premia should rise accordingly. – Bloomberg

We have also not gleaned any bull trap in the price action. Therefore, it remains to be seen whether bond buyers could return in earnest to prevent the 20Y yield from retaking its October highs. As such, further downside in the TLT should not be ruled out.

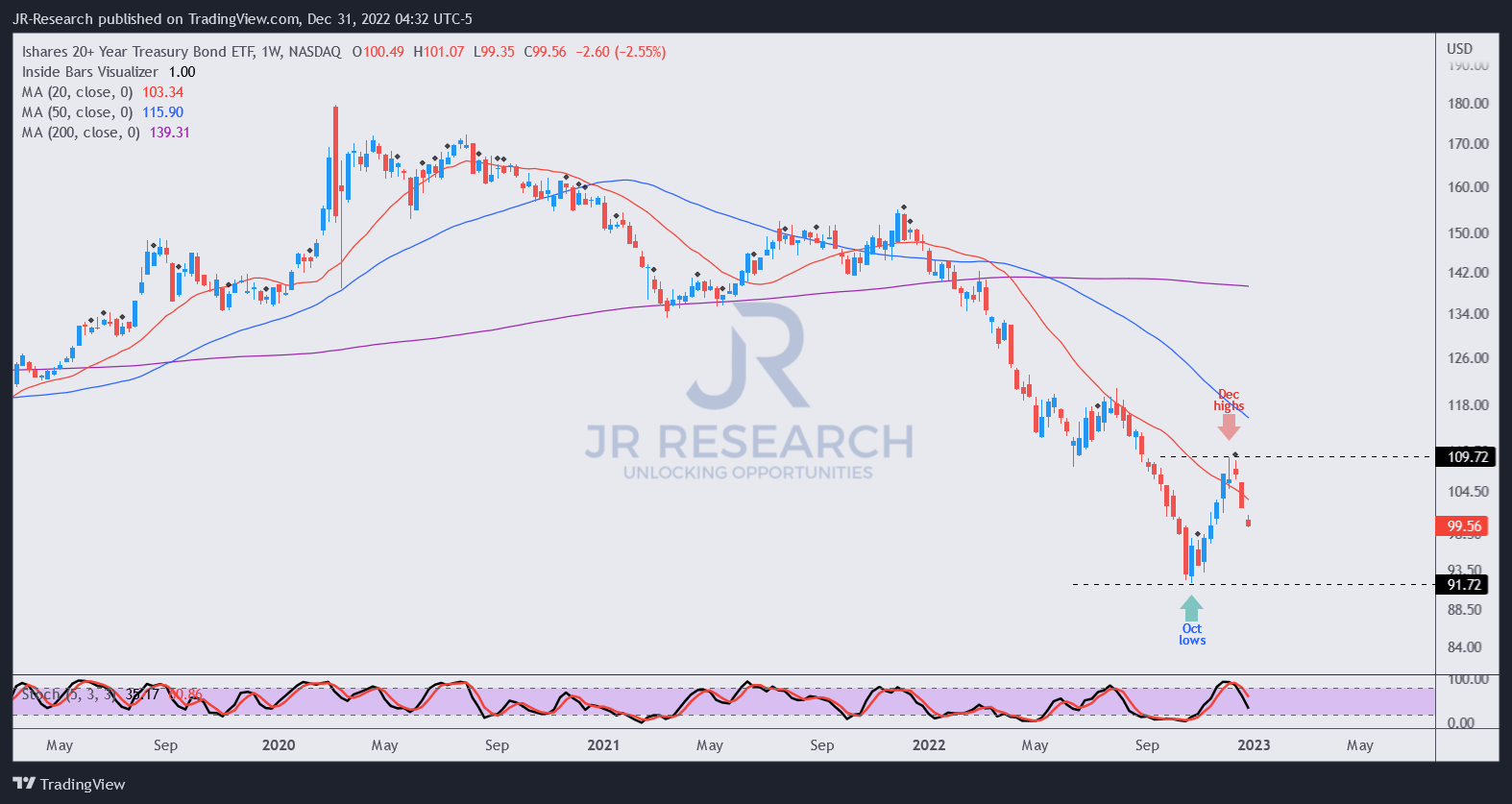

TLT price chart (weekly) (TradingView)

TLT’s medium-term price chart clearly shows that bond sellers remain in control of its downtrend bias, as seen above.

TLT sellers rejected its December highs as investors reacted to the Fed’s hawkish stance through 2023. With the TLT pulling back, we need to see buyers returning to defend it from breaching its October lows decisively for our thesis to remain valid.

Takeaway

Our base case is for a mild-to-moderate recession, which we postulate has likely been contemplated at the SPY’s October lows. As such, TLT lows in October should also have baked in peak Fed hawkishness, as the market anticipates the Fed to pivot in 2023/24.

With that in mind, we make the case that the TLT’s October lows should be supported, with bond sellers likely losing conviction at those levels, believing that the Fed is likely near its peak hiking momentum.

Hence, capitalizing on the pullback in the TLT to benefit from a potential mean reversion opportunity, whether or not we get a slowdown/recession/deep recession, seems constructive if investors missed its October bottom.

Rating: Buy

Be the first to comment