bodnarchuk

I wrote about Coeur Mining (NYSE:CDE) in October here, explaining the tremendous and misunderstood leverage the company has to gold/silver prices. Management was forced to raise capital in a share offering early in 2022 because of weaker-than-expected metals pricing. The company has expanded shares outstanding each year the past decade on asset combinations and equity issuance. In the end, regular share dilution has been the primary reason investors shy away from owning this company.

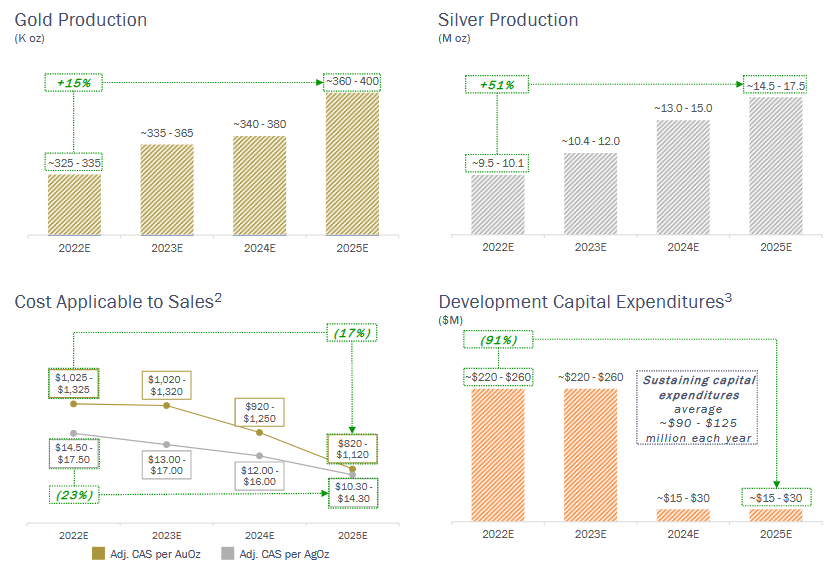

However, dramatically stronger silver production is coming in the second half of 2023 from its Nevada Rochester mine (after years of expansion costs lacking revenue to offset the capital outlay). In addition, the company raised needed cash of $150 million by selling out prospective resource properties to AngloGold (AU) late in 2022 at a rich premium to underlying holding values. Altogether, these positive developments mean Coeur is expected to be generating better profitability in 6-12 months (at least breakeven by Q4) and significant free cash flow, without any meaningful rise in metals quotes.

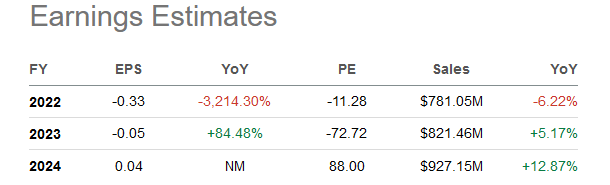

Using effectively stagnate gold/silver prices, Wall Street analysts are projecting cash earnings to appear by early 2024, on the back of Rochester production increases. Using a super-bullish projection of a 50% increase in gold/silver prices over the next 12-18 months (US$2800 gold and $38 silver), I am coming up with EPS potential above $1 in the not-too-distant future. To say Coeur is highly leveraged to extended precious metals upside is something of an understatement of the facts.

Seeking Alpha Table – Coeur Mining EPS & Sales Estimates by Wall Street Analysts, January 12th, 2023

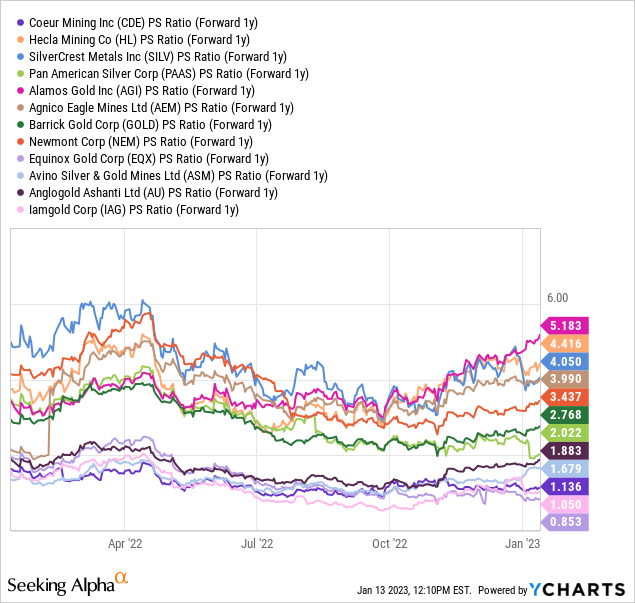

Another expression of this positive leverage story is found in the price valuation to forward 1-year projected sales. The highest income margin, strongest reserve players are valued in the 3x to 5x ratio range on revenue currently. Mid-tier and expensive-cost miners are closer to Coeur’s 1x multiple. The good news is Rochester’s expansion coming online in 2023 is forecast to lower unit costs of mining for the whole company, while providing extra cash for debt reduction. As time passes and gold/silver prices climb, I am thinking newly robust income levels and lower costs should combine to GROW Coeur’s valuation multiples on top of quickly improving operating results. This setup is what gets me excited about CDE, assuming management can execute its plan.

YCharts – Gold/Silver Miners, Price to Forward Estimated 1-Year Sales, 12 Months

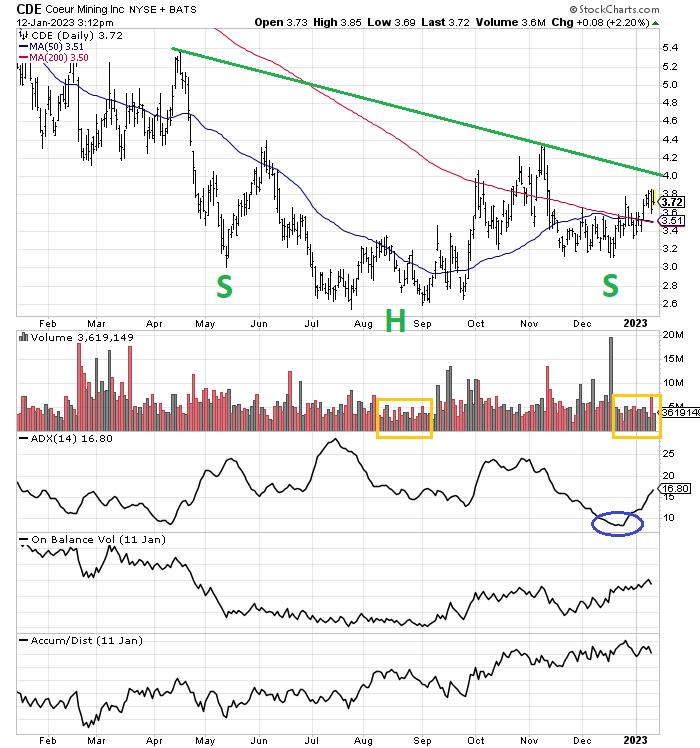

Bottom line, the best excuse to consider buying Coeur today is the immediate chart trading pattern. Over the last six months, price has outlined a tremendous looking head-and-shoulders bottoming picture, where a supply/demand turn in share trading can be pinpointed (not guaranteed, but it does increase the odds of rising price soon). Plus, a number of momentum indicators are signaling a lack of supply (sellers) may now exist, which could lead to a material upturn in the share quote, given rising gold and silver prices continue throughout most of the year (which is my prediction). I have written extensively on the odds of a powerful up-move coming in precious metals during 2023, with a long list of arguments why such is plausible (including bullish seasonality, inverted lease rates on metals, low valuations relative to other asset classes and recent gold/silver history, futures market positioning, and more).

Coeur Assets

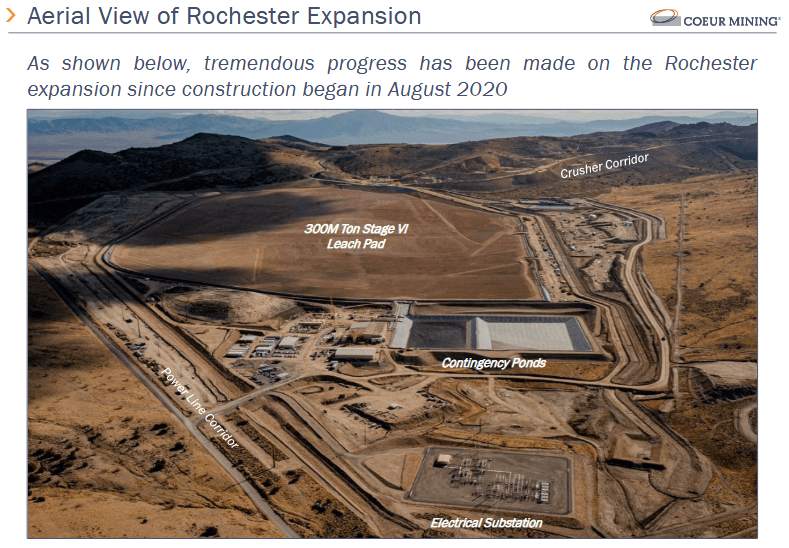

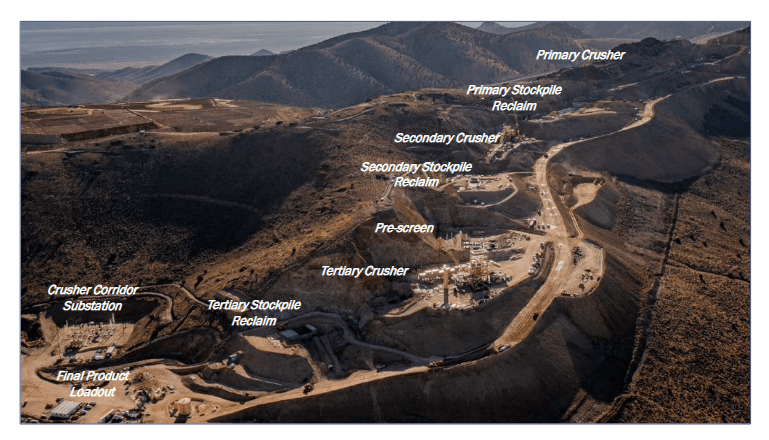

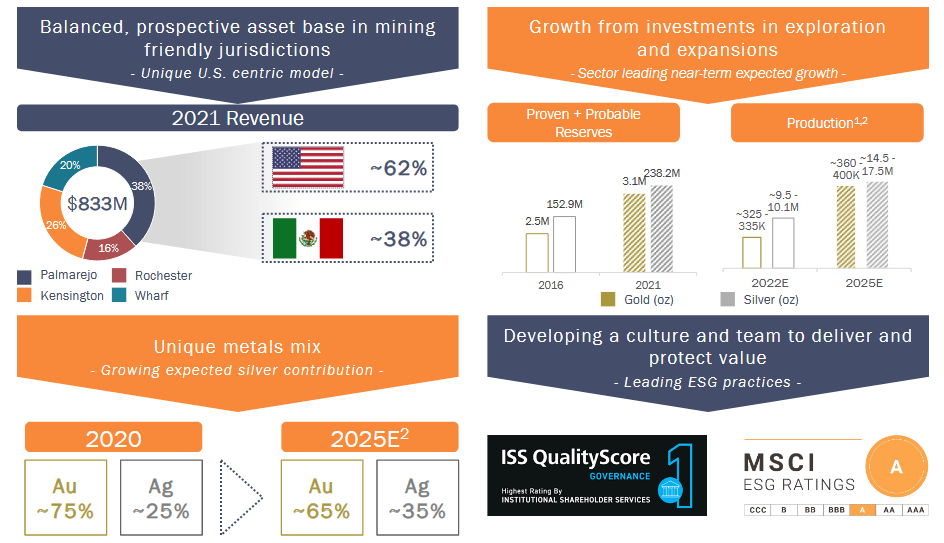

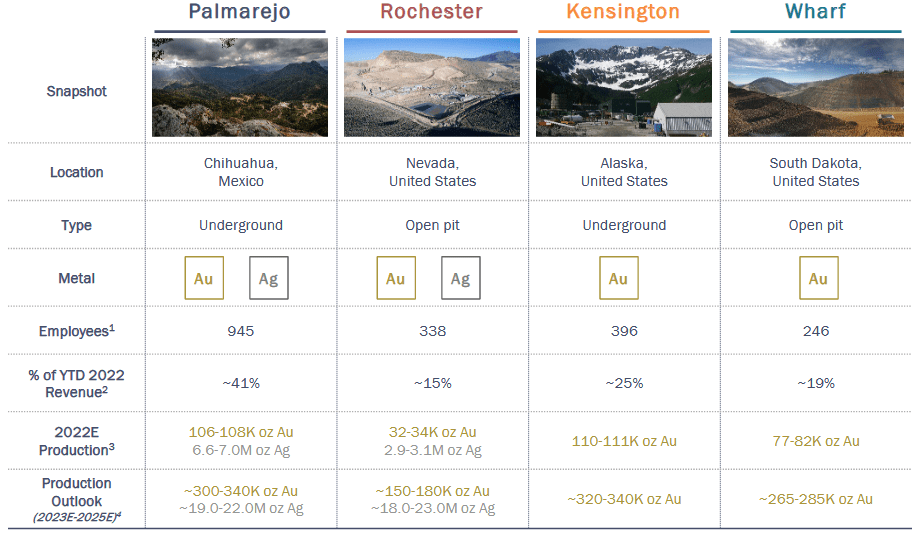

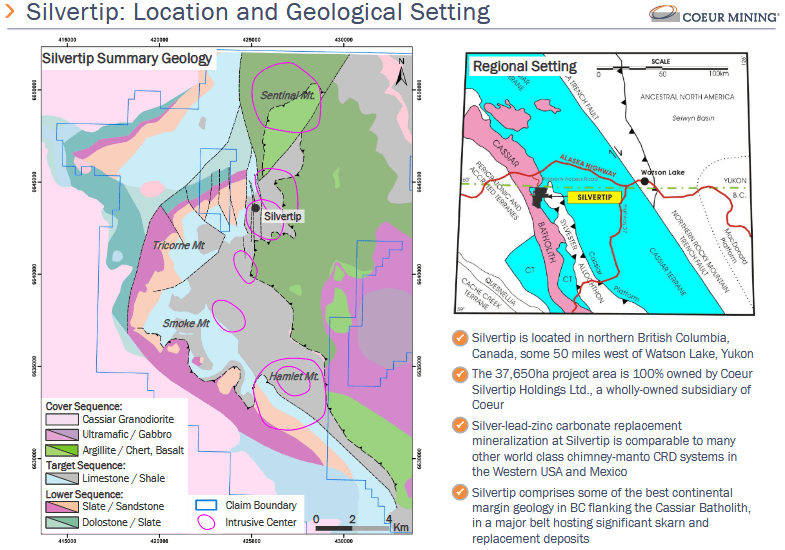

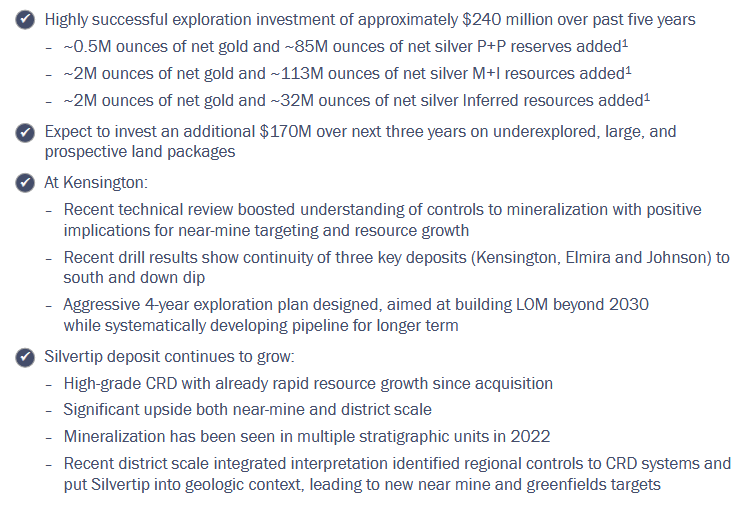

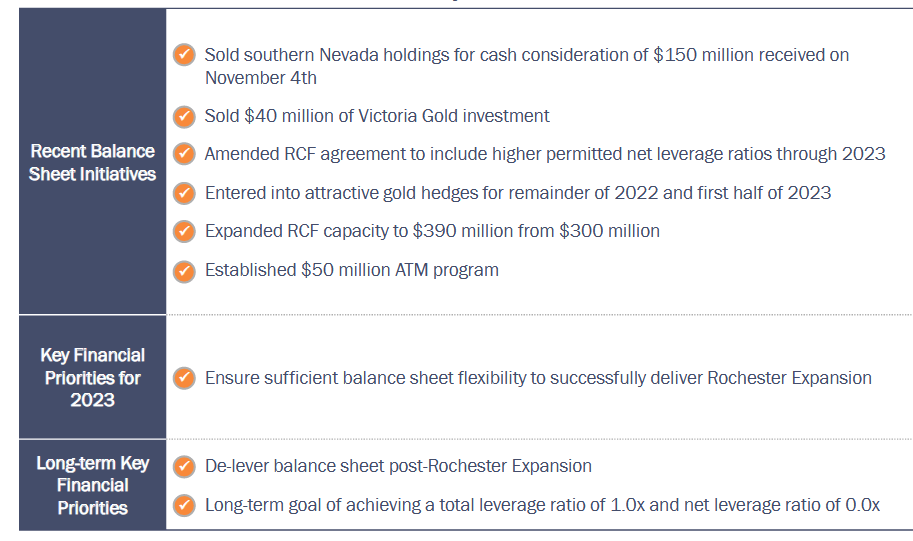

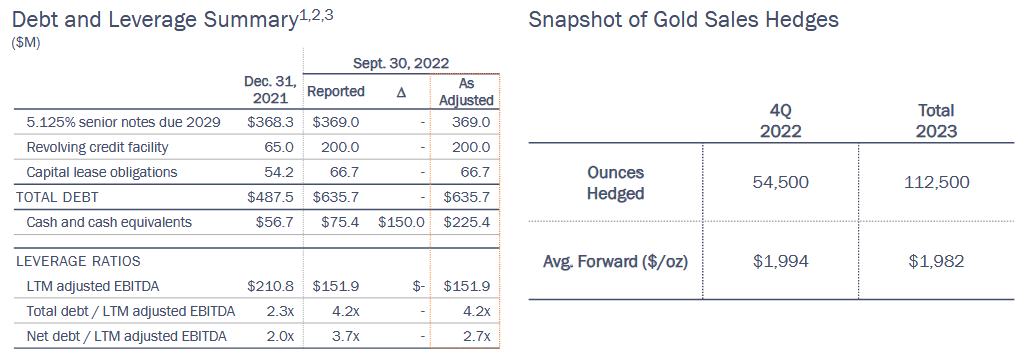

Below are graphs, tables, and ideas taken from the mid-December Investor Day Presentation put out by the company. The slides provide an excellent overview of Coeur’s operating assets, reserve/production levels, and balance sheet. The highlights are new ounces and revenues are coming soon from Rochester, and a few years later from the Silvertip mine under development in Canada. Four operating mines in North America could easily be five in time. Also, after years of heavy capital expenditures, management is forecasting a major decline in required investment spending alongside a substantial rise in “free” cash flow starting in 6-9 months. The added free cash generation (from Rochester) is targeted to reduce debt/leverage closer to zero in 2-3 years (potentially eliminating almost $20 million in annual interest expense). In the end, Coeur could move from one of the higher-cost mining outfits into the middle of the pack for global producers.

December 2022 Investor Day Presentation – Rochester Mine – Refining & Leaching Construction December 2022 Investor Day Presentation – Rochester Mine – Crusher Construction December 2022 Investor Day Presentation – Revenue Overview, Mine Safety Record December 2022 Investor Day Presentation – 4 Operating Mine Stats December 2022 Investor Day Presentation – Silvertip, British Columbia Map December 2022 Investor Day Presentation – Exploration Success December 2022 Investor Day Presentation – Balance Sheet Changes December 2022 Investor Day Presentation – Debt & Gold Hedge Numbers December 2022 Investor Day Presentation – Projected Mining Costs & Production

Bottoming Chart Pattern

Coeur appears to have outlined a classic head-and-shoulders bottoming pattern, where selling volumes have dried up on the shoulder just completed in December. Below is a 1-year chart of daily price and volume changes. I have boxed in gold the ultra-low trading volume lately, which matches up well with the price bottoming area in August. In addition, the 14-day Average Directional Index score of 7 several weeks ago (circled in blue) was the lowest since 2015. The ADX highlights a low-volatility balance of buying and selling weeks ago.

On Balance Volume and the Accumulation/Distribution Index have been moving in the right direction since September. Plus, new highs in both indicators over the last couple of weeks could be leading price to the upside. With price drifting above both the 50-day and 200-day moving averages in January, it looks like the first milestones of a trend reversal from lower to higher have been achieved.

Finally, I have drawn a green trendline through 2022’s declining high trades. It now crosses $4 per share. My conclusion is any advance above $4 in coming weeks will be screaming a long-term up-move has begun.

StockCharts.com – Coeur Mining, 1 Year of Daily Price & Volume Changes, Author Reference Points

Final Thoughts

I doubled my small Coeur position last week, a function of the chart pattern and steadily rising gold/silver prices so far in 2023. My stake size is now in the average range vs. about 10 other gold/silver mining holdings in my personal portfolio.

Given a rapid ascent in gold and silver quotes during 2023-24, I am projecting potential CDE upside to $10 or even $15 a share. Of course, this will depend on management hitting its forecasts, and following through on deleveraging, as laid out in the Investor Day Presentation.

What could go wrong? Plenty. The company and its mines are smaller. So, operating issues at any of its producing assets could hold price down. In addition, if the Rochester mine assumptions and forecasts prove overly optimistic, Coeur will be stuck under $5 a share, until gold/silver really get moving in a bullish direction (the bullion advances since September have been relatively mild historically for precious metals swings). Lastly, if my estimates of a large rise in gold/silver are wrong, and the metals do not jump appreciably this year, Coeur may be stuck under $4 in 2023.

I am modeling worst-case downside risk to $2 per share this calendar year (operating cost issues on top of lower gold/silver values) vs. best-case upside to $10. This equates to potential total return losses of -40% vs. gains of +200%. This risk/reward analysis suggests a bullish outcome is most likely over the next 12 months. I am upgrading my Coeur view to Strong Buy. An expected 50% jump in company-wide silver production (at lower unit costs) over the next 18-24 months is well worth the price of entry and investment risks acquired.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Be the first to comment