Latch liquidation currently unlocks more value for investors.

mikkelwilliam/iStock via Getty Images

The spectacular decline in growth stocks has presented investors with some interesting net-net opportunities, and Latch, Inc. (NASDAQ:LTCH) is certainly one of them. Once labelled by Chamath Palihapitiya as the best SaaS company he’s ever seen, the stock now sells for less than cash net of all liabilities after falling a spectacular 91.39% over the past 12 months as of the time of writing.

The stock represents an interesting opportunity for net-net investors. Made famous by Benjamin Graham in his 1932 Fortune Magazine article, a net-net situation arises when a company’s stock sells below liquidation value. Latch along with a handful of other growth companies find themselves in that situation today.

A Look at Latch’s Q1 Balance Sheet

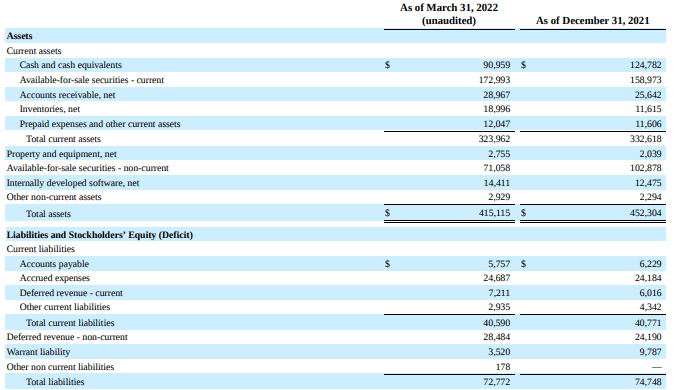

Latch has a high-quality balance sheet (Latch, Inc. 10-Q)

The two most important figures here are the cash and cash equivalents plus available for sale securities on one side, and the total liabilities on the other.

You can see that the company is worth $262 million based on the cash it has net of all liabilities. With 142 million shares outstanding at the end of the quarter, that would equate to a liquidation value of approximately $1.85, more than double the current price.

The Wrinkle in Latch’s Balance Sheet

Almost half of total liabilities are comprised of deferred revenue. That would have been good news if the company is profitable. In Latch’s case, however, it means the company will spend even more to realize that revenue. Obviously, some of what it will spend will be deducted from inventories and prepaid expenses and wouldn’t affect the liquidation value. However, for the sake of conservatism, let’s assume the company will expense these costs out of the cash it has on hand.

Looking at the income statement of Q2, the company lost $50.6 million on $13.7 million in revenue. Of that, $36.4 million were cash expenses. Applying the same margin to deferred revenue of $35.7 million, the increase in total liabilities would be $94.9 million. This lowers the liquidation value to $167.1 million, or $1.17 a share.

As I’ve mentioned there is upside to that number based on how much of the expenses come out from other assets like inventory and prepaid expenses, in addition to any potential improvement from management’s cost-cutting initiatives.

There is also an upside from collecting receivables. The company has accounts receivable of $29 million, with an additional $2.8 million in doubtful accounts. The quarterly showed that the company recovered $350k during the quarter, so there is potential to recover more in future quarters.

But focusing solely on the $29 million in account receivables, the sum would represent a significant boost to the liquidation value if the company can collect them. In this best-case scenario, the liquidation value could jump to $196.1 million or $1.38 a share. This represents an upside of 50%

There is an Empty Half of the Glass for Latch’s Story

The company has already failed to file its second quarter 10-Q which is an ominous sign. This means that the figures discussed in this article might have changed dramatically.

Also, the management team has been selling stock according to SEC Filings. I haven’t been able to find an open-market purchase by any member of the management team, which hardly inspires confidence.

But The Glass is Also Half Full

Despite its troubles, Latch is still growing revenue almost triple digits. Its gross margins on the software side are a whopping 89%. The company simply faces the problem many other smaller companies face as a result of disrupted supply chains and inflation. These issues have meant it couldn’t improve its gross margin profitability on the hardware side. While I personally wouldn’t understand why a management would continue to sell a product it loses on when liquidity is looking like an issue, the fact the product is growing this strongly should count for something. The company cut more than 30% of the workforce. Also, supply chain and inflation-related issues will not last forever. If these issues are resolved in time, there is potential for multi-bagger returns and not just the 25-50% return mentioned in this article

This is also a net-net situation after all so no investor should have an assumption that holding the stock will be a breeze. At the end of the day, Latch is a relatively small company with $50 million. Almost every company, regardless of how invincible it may be today, has faced a similar challenge to what Latch is facing today. So just because it seems like the company faces an uphill battle today, doesn’t mean it is doomed to fail.

Having said that, it is my opinion that no investor should concentrate into net-net stocks. They work best as a portfolio due to the high bankruptcy risk. In my personal experience, most net-nets I’ve seen work was because they were either liquidated or because they got lucky with their turnaround efforts. However, the absolute majority of net-nets I have come across burned through their cash and the stock ended up languishing lower than when it first became a net-net. That is why it is better to buy net-nets as a portfolio. It’s the few winners that will more than make up for the losers. Ben Graham described investing in net-nets better than I ever will:

I consider it a foolproof method of systematic investment–once again, not on the basis of individual results but in terms of the expectable group outcome.

Conclusion

Latch’s spectacular decline of more than 90% over the past 12 months makes it a compelling part of a net-net portfolio. The company’s liquidation value based on the latest quarterly fillings could be between $1.17-$1.38 a share, as much as 50% above the current share price.

The stock does come however with the usual risks associated with net-net stocks. Management failed to file Q2 earnings in time so the balance sheet could already be much different than it was in Q1. Despite that, its business remains actually extremely strong on the revenue side which is rare for a net-net.

The stock is a buy for investors who do allocate a portion of their funds to net-nets. Latch’s stock must only be bought as part of a larger portfolio of net-nets in my opinion. Investors should avoid buying the stock on its individual merits as there is a real risk of a permanent loss of capital.

Be the first to comment