MF3d/E+ via Getty Images

I last wrote about the KraneShares CSI China Internet ETF (NYSEARCA:KWEB) close to three months ago. In that article, I claimed that KWEB’s excessive regulatory and economic risk outweighed the fund’s strong growth prospects and cheap valuation. The risk was not worth the reward, in my opinion at least.

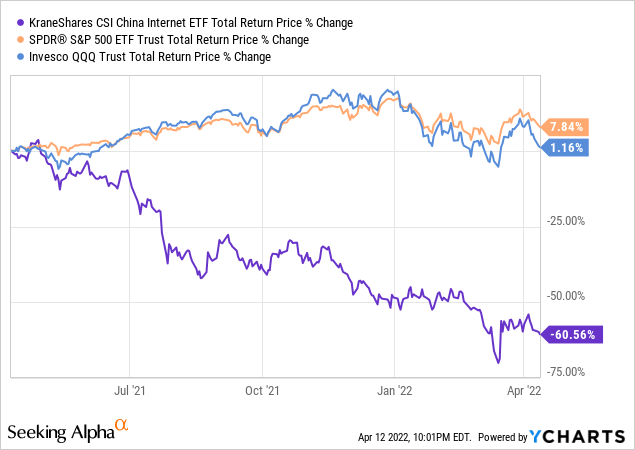

Since then, KWEB has plummeted by about 30%, significantly underperforming relative to its peers, due to increased regulatory risk, and the prospect of delisting from U.S. exchanges. Seems like it was the right call, at the time at least. As conditions have materially changed for KWEB since, I thought an update on the fund was in order.

KWEB’s plummeting share price means that fund prices and valuations are lower, while prospective returns are higher. Significant, strong, market-beating returns are a distinct possibility.

On the other hand, KWEB’s risks remain sky-high. Chinese tech giants are facing increased regulatory scrutiny from both U.S. and Chinese regulators. Sentiment remains bearish. Losses could mount.

In my opinion, KWEB continues to present an unfavorable risk-return profile. Risks are simply too high, and too difficult to quantify. KWEB would be a buy for me under a more favorable, softer, certain regulatory environment. Although there has been some movement in this direction, conditions remain broadly negative. KWEB is not a buy under current conditions, in my opinion at least.

KWEB – Quick Overview

A quick overview of the fund and its holdings before analyzing the current regulatory environment, the focus of this article.

KWEB is a Chinese internet equity index ETF. It is administered by KraneShares, a small investment management firm focusing on Chinese and Asian markets. KWEB tracks the CSI Overseas China Internet Index, an index of Chinese companies focusing on internet and internet-related activities, products, and services. It is a relatively simple index and fund, broadly tracking the Chinese internet equity market.

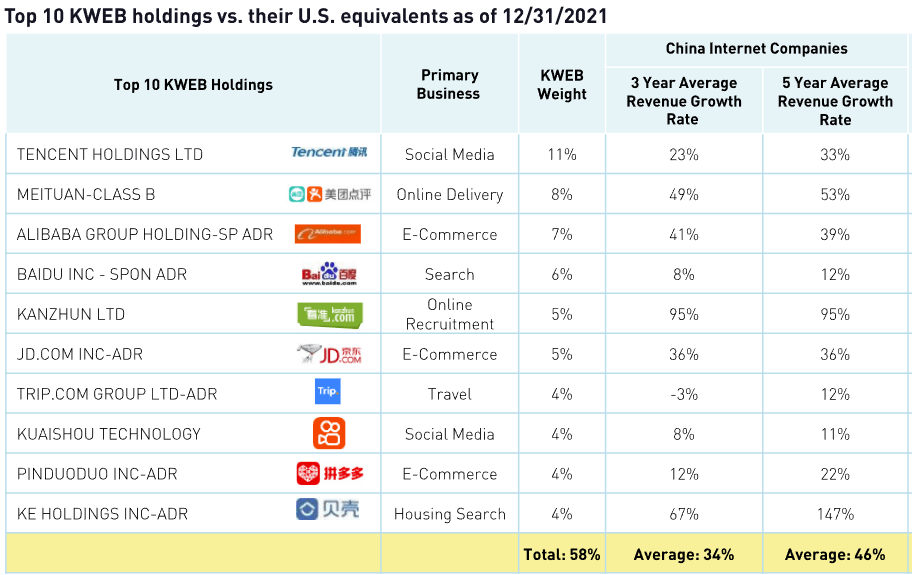

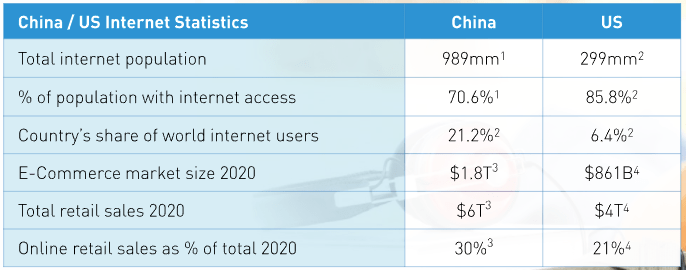

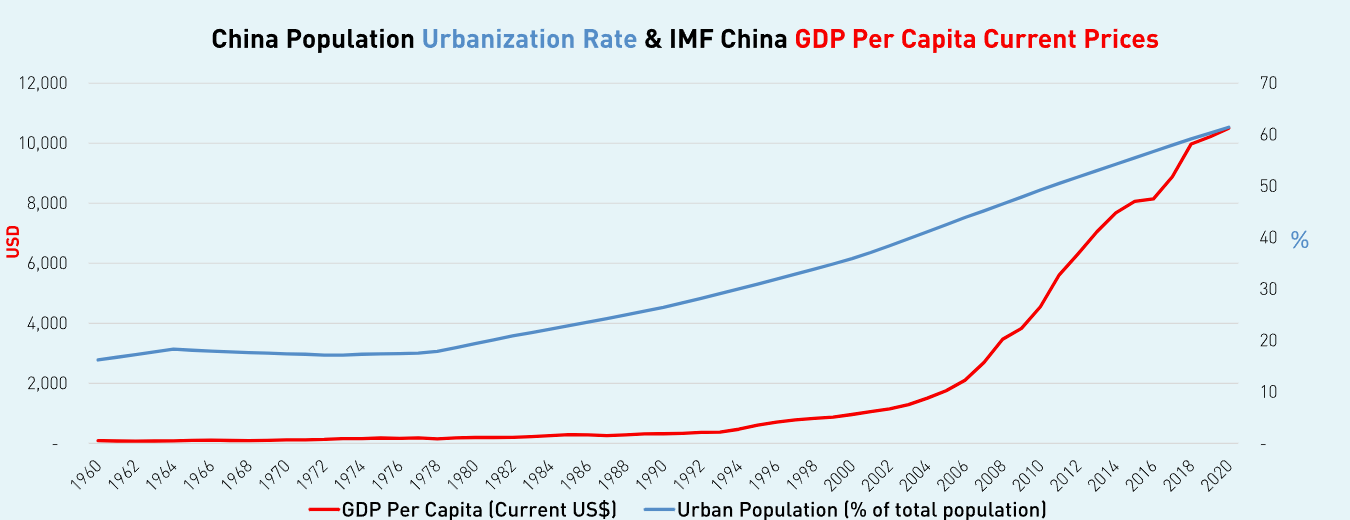

In general terms, KWEB’s underlying holdings are fantastic companies, with strong fundamentals and future prospects. KWEB’s underlying holdings have seen strong, double-digit revenue, earnings, and cash-flow growth for years. Growth is higher than the equity average, but roughly comparable results to those of most U.S. tech giants.

KWEB Investor Presentation

Growth is set to continue, as China remains a (comparatively) underdeveloped country, at least relative to most Western nations, but one which is rapidly catching up with the West.

KWEB Investor Presentation

KWEB Investor Presentation

KWEB Investor Presentation

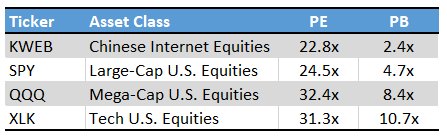

KWEB’s underlying holdings also trade with comparatively low prices and cheap valuations. The fund’s PE and PB ratio are both slightly lower than those of the S&P 500, even though KWEB’s holdings grow significantly faster than the average U.S. equity. The fund’s valuation metrics are also moderately lower than those of most U.S. tech equity indexes, even though growth rates are roughly comparable between these.

ETF Filings – Chart by author

KWEB’s fundamentals are incredibly strong, and could plausibly lead to sky-high, market-beating returns. Double-digit growth plus a double-digit valuation reset could easily lead to +30% annual returns for years, enriching investors. Although this seems like a plausible scenario, there are significant issues and risks to consider as well. Let’s have a look.

KWEB – Chinese Regulatory Risk

KWEB’s underlying holdings are fantastic companies, in my opinion at least, but the Chinese government seems to disagree. China’s top government leaders want the country to focus on “hard technologies”, including high-tech manufacturing, semiconductors and chips. That means de-emphasizing consumer technologies and services, including most consumer apps, video games, delivery services, etc. Chinese tech companies mostly focus on the latter, due to the economies of scale inherent in providing software products and services to a billion plus Chinese consumers.

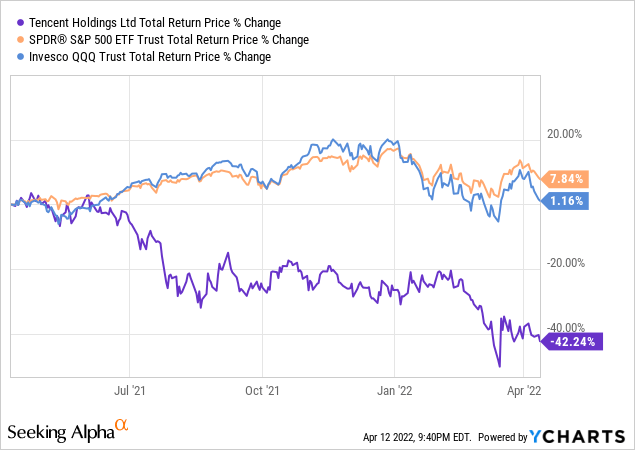

De-emphasizing consumer technologies is a significant blow to many Chinese tech giants, and that includes several of KWEB’s holdings. As an example, we have Tencent (OTCPK:TCEHY), the fund’s largest holding. Tencent has many business segments, including a large video game developing arm. Video games are an industry which Chinese leaders wish to de-emphasize, and they have taken drastic steps to do so. China significantly reduced the amount of time teenagers, a key video game demographic, can play multiplayer games last year. The regulation remains in effect, significantly reducing the popularity of video games in a key demographic. China has also put a freeze on new video game approvals for close to a year. No new video games means plummeting sales, as customers are not going to buy the same games twice. These two actions are incredibly harmful to video game developers, which helps explain Tencent’s significant underperformance for the past year or so.

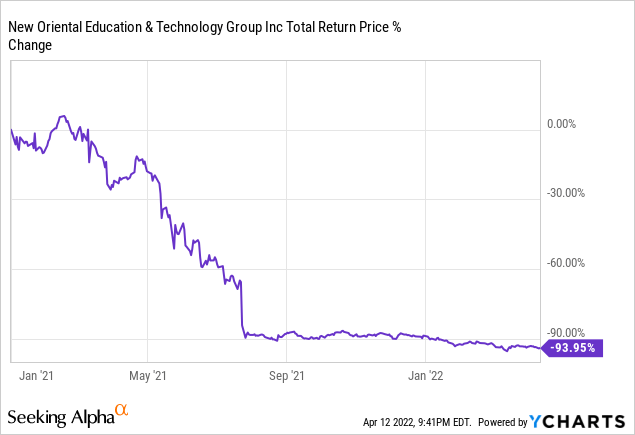

It is a similar story for other industries and stocks. China effectively banned private tutoring services for school-aged children, shuttering down most of the industry overnight. Industry losses were significant, swift, and effectively unrecoverable.

China’s leadership is also emphasizing “common prosperity“, which means focusing on (what they perceive to be) the prosperity of common Chinese workers and consumers above those of the tech giants. Chinese regulators are cracking down on the industry’s excessive 9-9-6 working hour system, providing greater benefits for the country’s army of gig workers, and fomenting unionization drives in the industry. These policies all (aim to) benefit Chinese workers and consumers, but increase tech costs, reducing profit margins and earnings.

Due to the above, Chinese tech companies have significantly underperformed for the past year. KWEB itself has plummeted more than 60% for the past year, dreadful results.

China’s regulators continue to crack down on the industry, and losses continue to mount. There have been no signs of a softening regulatory stance from the country’s leadership. As such, investors should assume the crackdown will continue, leading to further losses and underperformance.

KWEB – U.S. Regulatory Risk

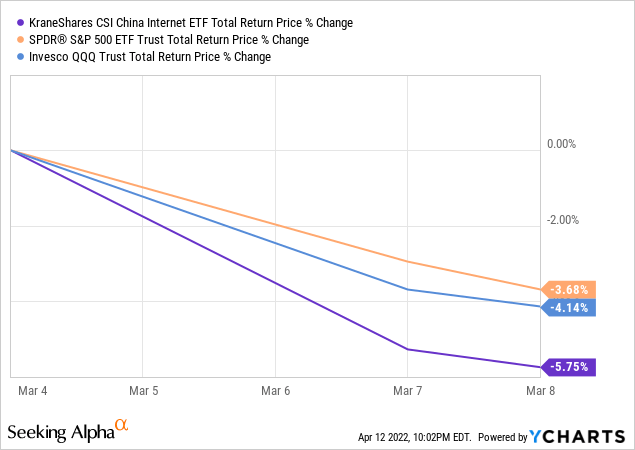

KWEB’s underlying holdings have also seen increased regulatory scrutiny from U.S. regulators, mostly due to the country’s lax financial reporting / audit standards. To trade in U.S. exchanges, foreign stocks must comply with U.S. regulatory standards, including (reviews of) audits by U.S. regulators. Several Chinese stocks have failed to comply with said standards, and the SEC has implied these could be delisted. Although delisted stocks can still trade OTC, meaning investors won’t lose their investment, being delisted significantly reduces liquidity, and hence prices. KWEB itself about 5% since the SEC implied Chinese stocks could be delisted for failing to adhere to relevant regulations. These are relatively large losses for such a short period of time, although not significantly greater than the stock market average.

At the same time, companies which are delisted from failing to comply with U.S. financial reporting standards are at heightened risk of accounting issues, including fraud. Companies hide their books for a reason, and that reason could very well be fraud. This was the case for Luckin Coffee (OTCPK:LKNCY), a Chinese stock, and something of a canary in the coal mine for the industry’s current woes. Luckin Coffee’s accounting was fraudulent. Accounting fraud means delisting, for failing to comply with regulations, and as punishment / deterrent. Accounting fraud also means significant financial penalties, which resulted in Luckin Coffee’s bankruptcy. Technically the bankruptcy had little to do with the stock being delisted, but only unsafe, extremely risky companies get delisted, and these are prone to bankruptcy. Being delisted from U.S. exchanges is simply a huge red flag, and one which investors should avoid.

KWEB – Uncertainty

KWEB’s risks are quite clearly significant, but difficult to precisely estimate or quantify. Chinese stocks are at the mercy of regulators, especially Chinese regulators, and I have no inside knowledge or educated opinion on their expected future actions. As such, and in the interests of risk-reduction, I’m assuming the worst. This is something of a judgement call, and so other investors might assume differently.

Conclusion

KWEB’s regulatory risks are excessively high, and difficult to precisely estimate. As such, I would not be investing in the fund at the present time.

Be the first to comment