Scott Olson/Getty Images News

FOMO (fear of missing out) is a real thing when it comes to value investing. That’s because nobody can time a perfect bottom on every stock, and when a stock finally takes off, it’s too late to buy more at low prices. With the recent market rally, some stocks, such as Walgreens Boots Alliance (WBA) has gotten more expensive very quickly.

However, it’s worth reminding that it’s a market for stocks rather than the stock market. A bunch of names haven’t participated in the recent market rally last week. This brings me to Kraft Heinz (NASDAQ:KHC), which actually declined in value last week while the S&P 500 (SPY) surged. In this article, I highlight why KHC is a worthy value pick for income investors, so let’s get started.

Why KHC?

Kraft Heinz is the third-largest food manufacturer in North America, with iconic brands such as Oscar Mayer, Heinz Ketchup, Velveeta, and Kraft Mac & Cheese. The company has a strong presence in both developed and emerging markets, with over 200 brands in its portfolio and sales in 190 countries.

KHC has been no stranger to challenges, but management has made the right moves in recent years by divesting non-core businesses, while investing in core brands and improving efficiencies. It appears that their turnaround efforts are bearing fruit. This is supported by strong third quarter results, with net sales growing by 2.9% YoY.

While this may not seem too impressive on the surface, it’s worth noting that this includes the negative 6.4% impact from divestitures and acquisitions as well as a negative 2.3% impact from currency (stronger U.S. dollar).

Importantly, organic net sales rose by an impressive 11.6% compared to the prior year period. This was driven by KHC’s pricing power, as prices rose by a robust 15% over last year, demonstrating strong price elasticity. This more than offset the 3.8% decline in volume, driven primarily by supply constraints and higher prices.

Also encouraging, management intends to realize $2 billion in savings driven by efficiencies by 2024, including $400 million in the current fiscal year. This would enable more capital for either debt reduction, shareholder returns, and/or investments into key brands. As such, it appears that KHC is focused on sustainable long-term profitability over short-term boosts.

As with food and beverage peers, KHC’s premium brands face competition from private label, and while consumer downtrading may be a concern, it appears that KHC premium brands have been able to keep up with this pressure. This was noted by management during the Q&A session of the recent conference call:

Q: As we look across the store, private label share has been up at a lesser rate over the past few months, although it seems like it’s gone up a little bit more so in your categories. I just want to get a sense of if you see incremental risk in your categories from private label share gains as you take more pricing where you have more pricing that’s been put in place?

A: On private label, a few things. First of all, as we have been continuously reiterating our exposure to private label have reduced significantly after the divestures mid last year. So now the average market share in our portfolio is about 11%, wherein across food and beverage is 20%. So that were not impacted.

Second, during the past 3 years, as part of our transformation, we have been directing a lot of our effort and energy around the core. So resources have moved that. We have been renovating the core in a very systematic way, so our portfolio is stronger.

Third, the private label have been increasing the price together with the rest of the players. So as recent as the last 4 weeks, including already 3 weeks of October looking at sellout data, our sellout price is about 17% up, whereas private label is 16% up. So price gaps are widely preserved.

We don’t want to be even over optimistic that depending on how consumers eventually shifts behavior in a very drastic way, things can change, but there is no indication of that as of right now. And honestly, I mean, despite all the environment, food is proving to be very resilient. The brands are being very resilient.

Meanwhile, KHC maintains a BBB- investment grade rated balance sheet with a long-term debt to capital ratio of 28%. It also pays a well-covered 4.3% dividend yield, with a 59% payout ratio. Turning to valuation, I find KHC to be attractive at the current price of $36.99 with a forward P/E of 13.7, sitting well below the 15 to 20x P/E range that consumer staples stocks generally trade within. For comparison purposes, The J.M. Smucker Company (SJM) stock currently carries a forward P/E of 16.8.

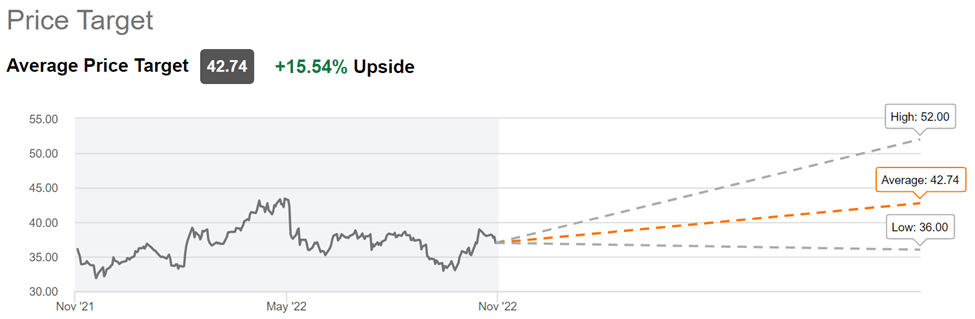

Morningstar has a $52 fair value estimate, highlighting the company’s potential for consistent profitable growth. Plus, analysts have a consensus Buy rating with an average price target of $42.74, which implies a potential one-year 20% total return including dividends.

KHC Price Target (Seeking Alpha)

Investor Takeaway

Kraft Heinz is an enticing investment opportunity in the consumer staples sector. The company has a strong portfolio of well-known brands that should continue to perform well from a pricing power standpoint despite pressure from private label products. In addition, KHC sports a solid balance sheet and pays a well-covered dividend yield. I believe the stock is attractively valued at current levels and should be considered for purchase by long-term dividend investors.

Be the first to comment