choness

Kilroy Realty Corporation (NYSE:KRC) is one of the top owners and operators of office, life science, and mixed-use properties, with a sizeable presence in the west-coast markets. In addition, they also have an expanding footprint in the fast growing Austin, Texas region.

Shares are currently down about 40% over the past year and are up just under 4% YTD. This is underwhelming compared to the broader market, which is up about 7% over the same YTD period.

Despite the weaker share price performance, their operating portfolio has numerous characteristics that sets them apart from their related peer set. For one, their net operating margins run in the 70% range versus in the mid-60s elsewhere in the sector.

Their properties are also newer and more amenitized, which is a demand premium in the current market environment. And for income investors, their strong track record of dividend growth is a reprieve from the numerous cuts announced by several of their office-focused peers.

At year end, these strong portfolio metrics largely held up. Looking ahead, however, management does expect lower occupancy and retention levels, especially in the first half of the year. This could weigh on shares in the near-medium term until there is further clarity regarding current lease-ups and the backfilling of newly vacated space. Though shares remain a quality portfolio holding, investors are unlikely to miss much by waiting another quarter or two before initiating a new position.

Current Portfolio Metrics

During Q4FY22, KRC executed nearly 330K SF of leases. This includes 102K signed within their development portfolio. Of the total completed during the quarter, over 70% was attributable to new signings.

Overall cash spreads realized during the quarter came in at 12.3%. This is significantly improved from the 1.2% realized in Q3 and also above their 11% annual run-rate. Retention, however, did take a hit, ending at 32% compared to 58.6% last quarter.

Looking ahead, retention is expected to hover around the low end of their historical averages, which is typically in the 50%-range. The lower rate is due in part to a few larger known move-outs, such as Amazon (AMZN) and DirecTV.

With regards to DirecTV, KRC took back about 150K SF of space at the end of the quarter, effective January 2023, leaving the tenant with about 530K of space. While the recapture may enable KRC to backfill it with a better quality tenant, the near-term vacancy is expected to weigh on 2023 occupancy and earnings.

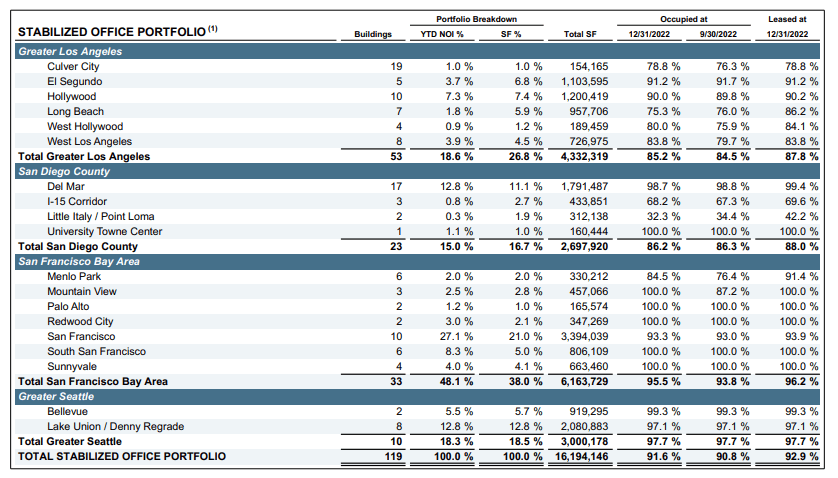

At year end, portfolio occupancy came in at an occupied rate of 91.6% with a leased rate of 92.9%. This was up 80 basis points (“bps) and 30bps from Q3’s reported occupied and leased rates, respectively. But looking ahead to 2023, the occupied rate is expected to average between 86.5% and 88%.

That is a notable decline from 2022. Most of this, however, is driven by their known move-outs of AMZN and DirecTV. In addition, there is also a known move-out at their West 8th property in the Denny submarket within Seattle. But this could prove to be an attractive mark-to-market opportunity, as the building is in a premier location within the district.

Aside from expectations of lower retention and occupancy, the overall portfolio remains healthy. And year end occupancy did come in ahead of their full-year guidance. Furthermore, in individual markets, their largest market by share of net operating income (“NOI”), San Francisco, ended the period at an occupied rate of 95.5% and leased rate of 96.2%.

Q4FY22 Investor Supplement – Stabilized Office Portfolio Occupancy By Region

Liquidity And Debt Profile

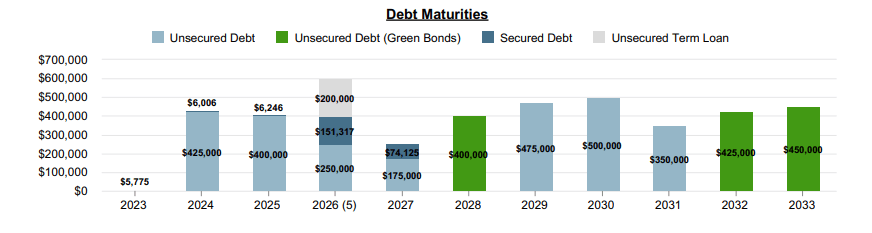

While current guidance assumes no acquisitions in 2023, their balance sheet remains well positioned to capitalize on any dislocations in the market. At period end, leverage stood at about 6x. There are also no maturities until late 2024.

Q4FY22 Investor Supplement – Current Debt Maturity Schedule

In addition, about 95% of their debt load is unsecured and fixed rate, both of which are credit positives. Ample cushion on key debt covenants also provides them with additional breathing room.

All considered, KRC has total available liquidity of +$1.7B. Aside from the availability on their revolver and term loan facility, this includes a sizeable cash balance of +$290M.

In January 2023, the company amended their term agreement to allow for up to +$500M of borrowings. At present, +$200M has been drawn. And looking ahead, management does expect to draw on the remaining +$300M through the fiscal year. This, combined with their other sources of liquidity is expected to fully fund their capital priorities for the year, including their sizeable development pipeline.

Dividend Safety

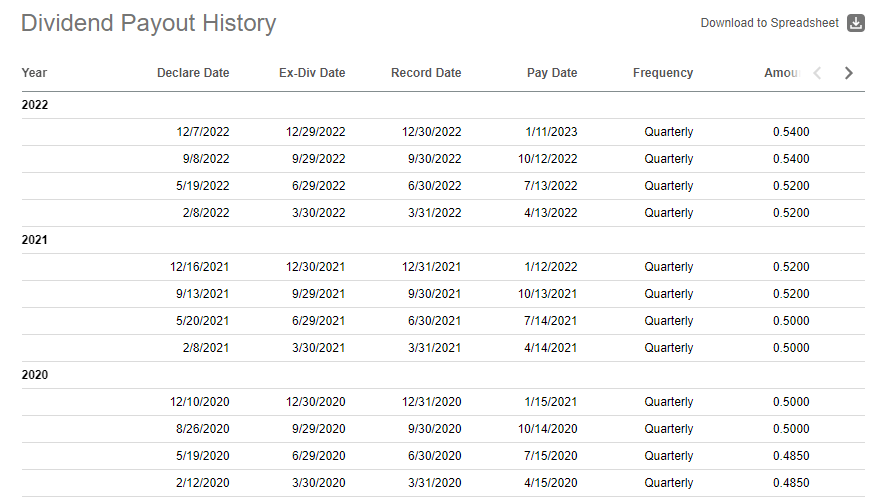

KRC currently provides a well-covered dividend that is growing at a 5-year compound rate of 5%. The stability and growth rate of the payout is one feature that sets them apart from most other office-related REITs.

At present, the current quarterly payout is $0.54/share. This is up about 4% from where it stood in the first half of the year. And at current trading levels, this represents a yield of 5.3%, which is modest, given the current alternatives in the current rate environment.

Seeking Alpha – KRC Dividend Payout History

The payout is not only backed by a strong track record of growth, but it is also well-covered by earnings and available funds. At year end, the payout ratio stood at 45.6% and 60.9%, respectively. This is competitive to peers and should be reassuring to investors who may have had their payouts cut with other holdings.

Main Takeaways

KRC remains a quality operator of office, life science, and mixed-use properties. Their growing exposure to the life sciences industry, in particular, is one growth driver that could propel current operating performance to new heights.

As it is, their exposure to the industry represents over 15% of their NOI. And looking ahead, the company is currently experiencing high demand for their in-process projects. Upon delivery of these projects, life sciences could grow to 20% of their portfolio NOI. Even further ahead, its share is expected to grow to 30%.

In addition to their exposure to higher quality sources of revenue, KRC is also maintaining sector-leading operating margins. At year end, NOI margin was 70.3%. While this is down from 73.5% last year and their weakest quarter of the year, it still outperforms both the sector at large and their west-coast peers, who typically run in the mid to high 60s.

KRC also boasts some of the newest property classes in their portfolio. This is especially important for those tenants seeking quality space. According to management, citing research provided by JLL, newer buildings are generating a 60% premium in rents compared to other properties. Furthermore, the supply of these properties appears to be on the decline. This bodes favorably for KRG in their ability to continue driving rents in future periods.

Though the portfolio remains healthy, management is projecting a decline in average occupancy in 2023. Retention rates are also expected to hover at levels lower than historical averages. This stems largely from known move-outs, but there could also be some level of uncertainty regarding ongoing lease-ups at play as well.

Furthermore, their portfolio is exposed to concentration risk due to their heavy west-coast presence. This could open them up to further losses if return-to-work rates remain lower than national averages and/or if there is a greater amount of subletting.

At less than 10x forward earnings, KRC is trading at a bargain, especially relative to historical averages. Consensus estimates peg shares with about 20% upside. And this is plausible. Though the tread higher may be slow, especially during the first half of the year, as the company works through their move-outs. For investors, the upside and corresponding dividend yield is there, but there is an elevated degree of uncertainty, at least for the first half of the year. This warrants a hold on positioning until at least their Q1FY23 release.

Be the first to comment