maselkoo99/iStock via Getty Images

Getting to know the company.

Just over 20 years past, back in July 2002, a tiny platinum exploration company, Jubilee Platinum plc listed on AIM on the London Stock exchange following an IPO that raised £1,258,470 (net of expenses). They had secured exclusive rights to prospecting and exploration on a number of properties in the southeastern portion of the Bushveld Complex, known as the largest global deposit of platinum and platinum group metal (“PGM”) reserves, in an area about 300km (about 190 miles) east of Johannesburg, South Africa, in its Mpumalanga province. They also acquired options to explore for PGM mineralization on properties in the Thunder Bay district of north-western Ontario, Canada. Additional exploration opportunities for Madagascar, Ethiopia, and Sierra Leone were contracted on option agreements.

The early Jubilee Platinum exploration company was in essence a project manager reliant almost entirely on the skill sets of its directors for success. Its founding Chief Executive Officer and force behind Jubilee Platinum was Colin Bird, a veteran mining engineer and manager with extensive experience in mining in the UK, Africa, Canada and South America.

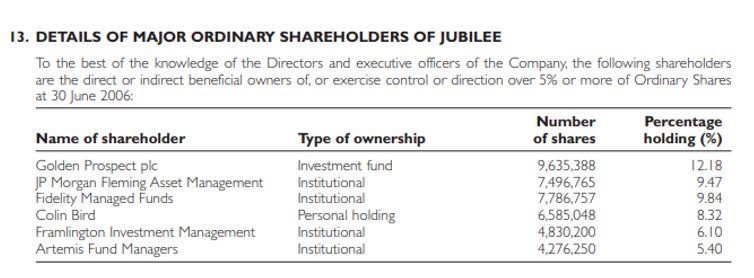

The directors of Jubilee Platinum were and once again still are highly respected, which gave them access to institutional funding and support. Shares have generally been held on buy-and-hold in institutional portfolios which kept the company out of the public eye. Here for example is the composition of shareholders holding 5% or more in 2006 from its application for a secondary listing on the Johannesburg Stock Exchange (“JSE”).

JMG website JSE Listing Application

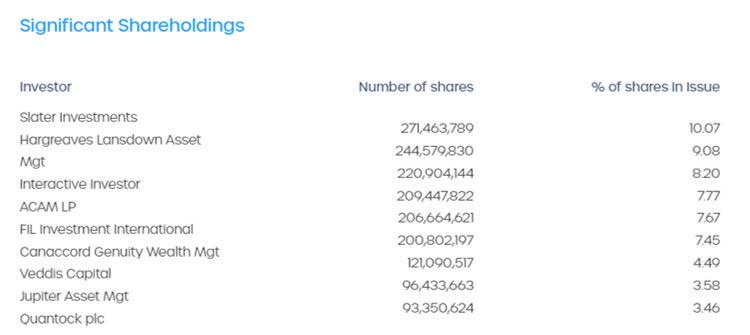

Jubilee Platinum plc, since renamed Jubilee Metals Group plc, still flies under the radar, and continues to be well supported by institutional investors. If anything, the institutional support has improved and the top 9 shareholders hold almost 62% of the company. We’ll also see that over time this relationship with institutional investors turns out a blessing and a curse.

JMG Website 2022 AFS

Jubilee Platinum plc achieved initial success with its Tjate Platinum Project shepherding it towards an independent bankable feasibility study, a significant milestone for any prospective miner, by the end of 2007. The real success came during the 2008 Global Financial Crisis when the company issued a SAMREC Code-compliant mineral resource statement for its Tjate Platinum Project and initiated the mining design for the project. The timing of the financial crash of 2008 and early 2009 saw the markets indifferent to the success of the company with little interest in its shares. The then chairman, Malcolm Burne, laments this development in the 2009 Annual Report:

“The year under review was very testing, with the economic crisis causing major brand names to collapse in the financial sector, resulting in the junior mining sector being ignored and company valuations being destroyed. Jubilee was disappointed to see the issue of Tjate’s mineral resource statement, a major milestone for the Company, attracting little interest and an insignificant share price movement.”

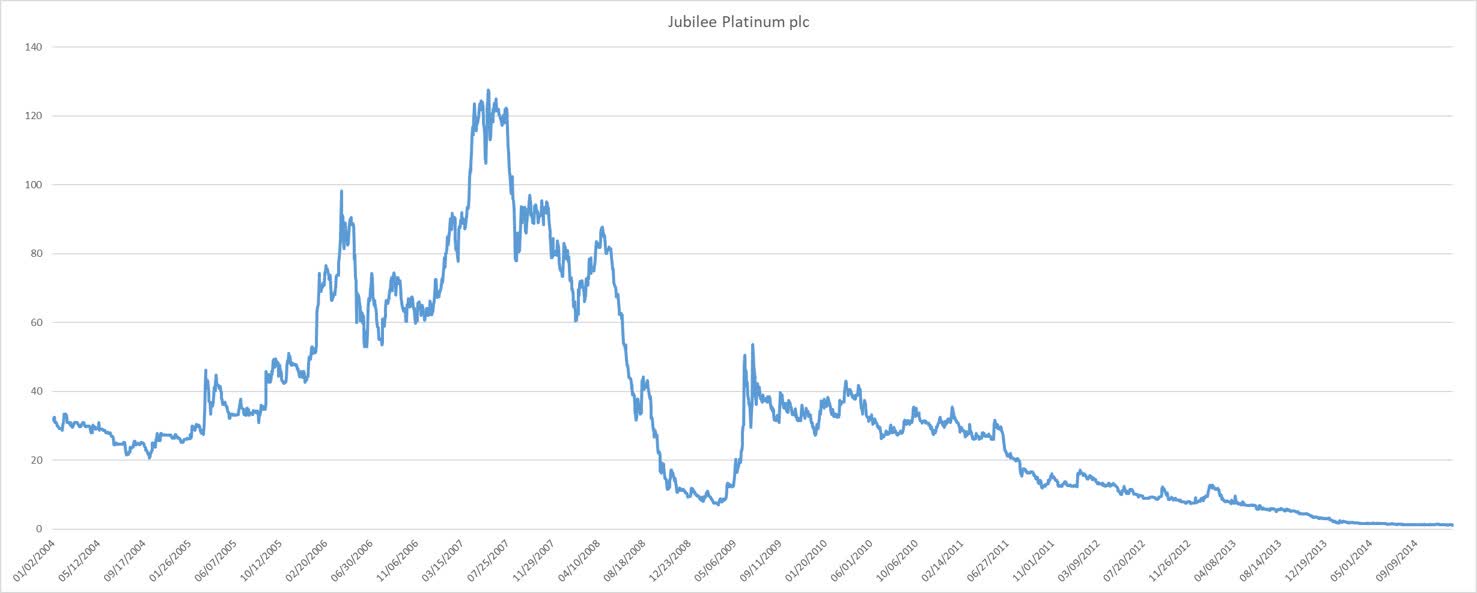

Jubilee Platinum plc transformed during 2009 from a project type exploration company to a junior miner and exploration company but the markets remained unconvinced of its success or potential. The share price did recover somewhat towards the end of 2009, but the Global Financial Crises relegated previously celebrated risk assets to the dustbin. The share price would eventually collapse by 99% to languish at around 1.2 pence a share by the end of 2014.

Sarel Oberholster, data from Investing.com

The 2009 CEO resigned and was replaced by a young Chemical Engineer and Metallurgist, Leon Coetzer in August 2010. It was in essence also the closing of the exploration and mining chapter and a new direction and new beginning for the company. The company pivoted towards a smelting and beneficiation strategy as a cashflow survival strategy while holding on to all its other projects with Tjate still the flagship project. It acquired the rights to the ConRoast process for PGM processing.

Jubilee Platinum had zero revenue in 2009 but the new survival strategy generated revenue of £950,000 in 2010 and £5.5mil for the year ending 2011. The company received and accepted an offer of ZAR75mil for the sale of an undeveloped portion of the Tjate project during the 2012 financial year contributing much needed capital though only concluding in the 2013 financial year. The smelting and beneficiation strategy continued to prove successful but a collapse in the platinum price from over $1800 in 2011 to eventually less than $800 by 2018 through to 2019 kept the company fighting on the back foot.

As can be expected, the years 2012 to 2019 were a long and testing battle for survival. The company’s share price slowly started to recover from the 1.2 pence level to reach around 4 pence by the end of 2019, still a far cry from the heydays of around 120 pence per share reached in 2007. Still, the company, in the background and under extreme testing conditions, built out its smelting and beneficiation strategy including provision of its own power supply to support smelting operations. They even entered into a contract with the South African government to supply it with excess electricity from their power plants.

The smelting and beneficiation strategy would lead them into the treatment and minerals recovery of mine waste, tailings, and slurry materials, securing contracts from a number of mines in the Bushveld Complex. The transition into the treatment and minerals recovery of mine waste took place over a number of years and the company’s rock bottom turning point was in 2015 with revenue for 2015 a meagre £48,899 while losses were piling up.

Jubilee sold its Middelburg smelter operation in 2015 as well as its electricity generating plant for ZAR110mil (about £5.3mil) and fully committed to the now prioritized platinum tailings venture. Little did they realize then that it would be the watershed which will see them return the company to financial health. They took 100% control over the platinum-containing Dilokong Chrome Mine surface tailings project and commenced with construction of the first platinum surface processing project. The transition completed in 2015 but financial success had to be carved out over the next 5 years.

Dilokong Chrome Mine Platinum and Chrome Surface Project (“DCM Project”) was commissioned and by financial year end 2016, had produced 15 188 tonnes (metric tonnes) of chromite concentrate (effectively from only two months of continuous operation). It is important to note the speed and skill of the company, to initiate and implement to cash generative status, a project of this scale. Management’s skill at exceptional project execution will become a hallmark of the company’s successes going forward and is an important consideration for any prospective investor, for the company will continue to leverage this skill to grow its portfolio of productive, cash and profit generating assets.

Parallel with expansions being added to the DCM Project, Jubilee also initiated the Hernic Tailings Project reaching 45% completion by June 2016 and 71% completion by September 2016. The company targeted 33,000 ounces of PGM production once both projects were in production.

The company announced on 6 February 2017 that the Hernic Tailings Project had been brought into production and that the first chromite concentrate had been produced. The strategy implemented with the chrome tailings treatments is to produce chromite concentrate as primary product and PGM as a byproduct but to have both value chains as profitable ventures.

The focus shifted, with both chromite tailings operations in production, to building the PGM recovery plant with the PGM circuit completed by the end of March 2017 and first PGM production announced on 29 March 2017. Management again demonstrated their technical and project execution acumen. Production of 3,682 PGM ounces was achieved by November 2017 at an incredibly low production cost of $476 per ounce. Most of these feats remained under the radar with investors uninterested in resources and PGM prices weak and unexciting. All the while management were cutting their teeth on PGM production in an extremely depressed market and succeeding brilliantly. Losses were shrinking and the vision of focused organic growth, even in a depressed market, was next on the agenda. More feedstock for the tailings and PGM recovery operations were secured including rights to 1,400,000 tonnes of new platinum-bearing surface material from Platchro.

Another trait of management to emerge is its prolific dealmaking at securing the economic rights to minerals targeted by it for production. Yet, another very important consideration for prospective investors. The scale of these acquisitions was pared with its organic growth vision and underpinned by the production success of the company. The targeted production of PGM ounces increased to 50,000 per annum. 2017 also sees the company putting out feelers towards opportunities in Zambia.

The new Jubilee posted its first operating profit in 2018 and the Group loss per share reduced by almost 84% and even at this relatively early stage moved to a positive cash flow from operating activities. Jubilee posted revenue of £14.14mil a mere 3 years after posting that dreadful £48,899 revenue number for 2015.

The Hernic Tailings Project (the expanded project since renamed the Inyoni PGM Operations) reached a monthly production level in excess of 2,500 PGM ounces, alone almost surpassing the 33,000 PGM per annum ounces target set by the company only two years previously in 2016 at a remarkable unit cost of production below USD 400 per PGM ounce produced. “… the project turned profitable within 2 months of commencing operations and within 16 months of commencing with project capital expenditure.”

The DCM Project produced 46 191 tonnes of saleable chrome concentrate in 2018. Jubilee management restructured the DCM venture with more dealmaking to expand the opportunity to include a new highly automated fine chrome recovery circuit as an industry first. This brings the innovative character of the company to the fore, another trait important to investors.

In yet another deal on the Platchro Project (the expanded project renamed Windsor Chrome Operations), Jubilee entered into a joint venture with Northam Platinum to jointly develop the Eland Platinum Project, planning to commence the production of PGMs during Q1 2019. The targeted production for the Eland Platinum Project was set at 2,800 PGM ounces per month (33,600 ounces per annum).

Dealmaking initiatives in Zambia continued during 2018.

The growth vision of Jubilee gained traction by 2019. Revenue was up 67% at £23.6mil, Group Earnings came in positive for the first time up 431% at £7mil and posting a first-time positive earnings per share.

Once again Jubilee management demonstrated a new trait, an environmentally conscious approach to mineral beneficiation. “We turn potential waste liabilities into assets through implementing our bespoke environmentally conscious metal recovery solutions that ensure a zero-effluent policy.” The company literally cleans up legacy mining waste with their expertise to implement mine waste recovery projects.

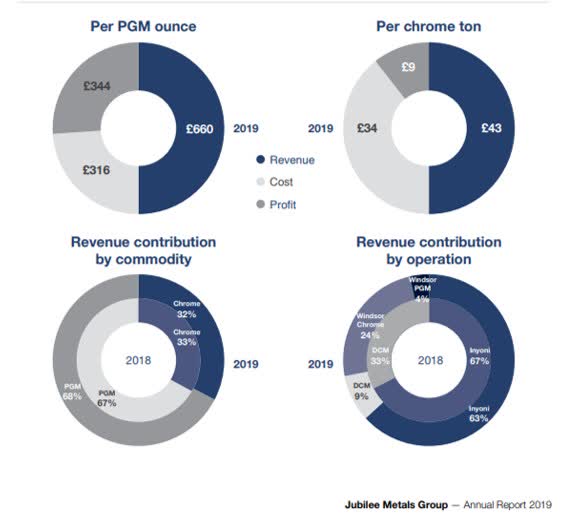

The incredibly low production costs and very healthy profit margin production footprint emerges as projects mature into stable production during 2019. Just be aware that the infographic is in £ and not in $.

JMG Website 2019 AFS

Chrome and PGM production technologies for on-surface mine waste had been implemented in a highly cost efficient, innovative, and environmentally friendly manner.

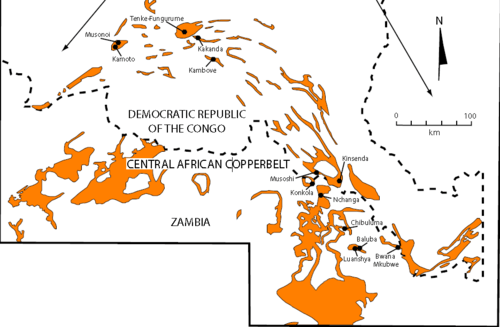

Jubilee increased its interest in Zambia during 2019 deploying once more its dealmaking, innovation and technical skills with the Integrated Kabwe Operations project, “a Zambian based multi metal refining facility currently under construction, which includes nearly 6.4 million tonnes of vanadium, zinc and lead containing surface material and further supplemented by third party ore supply.”

Jubilee identified an older Sable Zinc Refinery, located near their tailings and primary oxide ore for acquisition, refurbishment, and repurposing rather than to build a new plant. Initial overtures were made for this acquisition.

The new Jubilee has an aversion for the risks of below surface mining with a clear preference for mineral extraction and beneficiation from above surface mining waste materials in which they had developed specialist technologies, skills and IP. It meant that the Tjate platinum mining project was not prioritized but still advanced in the background towards a “spade ready” project and a valuable asset in reserve. The new Jubilee has established itself on solid foundations of low cost, profitable and cash generative projects and a sustainable business model which it continues to leverage into new projects. Opportunity in legacy mine waste recovery is almost limitless and they are alone and at the forefront of that space in PGM’s and base metals. Their internal IP is singularly an incredibly valuable asset and strong moat.

Unbeknownst to them, their foundations and newfound progress were about to be tested in 2020 with the arrival of the COVID pandemic. The new Jubilee took COVID in its stride simply powering ahead with its growth strategies. They secured the Sable Refinery which then opened the way to copper and cobalt production from legacy copper mining waste pollution across Zambia’s Copperbelt, an almost infinite supply of copper mining waste and tailings.

Wikipedia

The Sable Refinery, an initiative of 2019, was acquired and turned into a productive asset by March 2020 when it produced its first copper cathode from tailings. Soon after, cobalt production was added. The speed and competence of the Jubilee team, in their now comfort zone, is frankly breathtaking and the company started branding their unique style as “The Jubilee Way”. Jubilee positioned themselves perfectly for the much coveted “battery metals”, copper and cobalt.

Jubilee’s initial estimate of copper tailings puts it at over 1 billion tonnes of mine waste dump and tailings, no typo, 1 billion tonnes of available materials to reprocess and to significantly improve the environment. Jubilee’s dealmakers went right ahead and in June 2020 secured the rights to 150 million tonnes of copper containing surface tailings as the first step.

The annual processing capacity for copper waste materials at the Sable Refinery is 14,000 tonnes of copper at an expected yield of around 1.9% per tonne of waste material, which means that Jubilee ‘s 1st sweep had secured enough material to feed this plant for around 200 years! That is, if we ignore the remaining probably still another 1 billion tonnes of waste materials waiting to be processed, then Sable is but a drop in the ocean. Clearly Sable was just a tiny beginning in a much bigger strategy.

PGM production reached 40,743 ounces for financial year 2020 up from 23,847 ounces in 2019 and well ahead of the 33,000 ounces target set in 2016, also well on its way towards the higher 50,000 ounces target set in 2017. PGM revenue jumped to £34.5mil in financial year 2020 from £15.8mil in 2019.

The ostensibly main product, Chrome Operations yielded 377 883 tonnes of chrome concentrate (2019: 181 947 tonnes), and generated chrome revenue of £ 17.2mil (2019: £ 7.8 mil). Revenue for the 2020 financial year increased by 132% to £54.8mil (2019: £23.6mil), Earnings grew 162% to £18.3mil (2019: £7mil). Cash from operating activities grew to £19.4mil (2019: 4.76mil).

The share price oscillated between 3 pence per share and 4 pence per share in the first half of 2020 and doubled to between 6 and 8 pence after results were published. Investors still had no appreciation for the successes and progress of the company and seemingly had (and still has) no comprehension of the incredible vision of the company and opportunity it is already actively exploiting.

JMG Website 2020 AFS

Nobody falls asleep at the wheel at Jubilee so the dealmaking team kept up the progress on securing additional supplies of mine waste feedstock and with the opportunities beckoning in Zambia, turned their eyes to another Southern Zambia opportunity, Project Roan. Also adding 115mil tonnes of copper and cobalt tailings (Project Elephant) along the way to take secured feedstock to around 270mil tonnes.

Jubilee closed the deal on Project Roan as a 50/50 joint venture, a project which targets a 100% increase in copper production in Zambia in the short term. Jubilee now targets production of 25,000 tonnes of copper per annum. Then there is also the zinc circuit planned for Sable which was delayed due to COVID sanctions and shifted for initiation to Q1 2021. Zinc will add yet another mineral to the portfolio to further diversify income streams. Most of the growth was financed organically given investor’s apathy towards the company but Jubilee was driving a relentless expansion even during COVID, nevertheless.

You will, no doubt, also have noticed the clever “circuits” strategy. Identify the most economically attractive mineral in the waste mix and get going on it asap but structure the plant as a general processor and circuits. Then add additional circuits almost like “plug-and-play” to reprocess materials from one circuit to the next, each time extracting yet another mineral from the mix. It often has double benefits such as removing chrome from the chrome/PGM mining waste feed improves the recovery of PGM ounces. It works the same way with the copper mining waste, remove the copper and cobalt becomes available. There is also a predictability effect because the main product (chrome and copper) is extracted first and then the much more valuable “by-product” is extracted. Any increase in production of the main products in one year already tells one in advance that more of the valuable byproducts are in the pipeline for the next financial year. Still, The Jubilee Way holds that every mineral must pay its own way and be profitable.

“…the chrome operations is the primary facilitator to our Platinum Group Metals growth as we extract the chrome from the materials and what remains is where we recover the Platinum Group Metals from.” CEO Loen Coetzer, Earnings Call 2022.

2021 The DCM and Hernic (now Inyoni) projects were designed and built with a specific feedstock in supply. The success of the company opened the door to a much greater variety of available feedstock, feedstock which the existing design never anticipated. Not wanting to pass the opportunity by, Jubilee jumped at the chance to grow even a stable and mature project to serve a greater range of customers and to diversify the feedstock into the Inyoni Project. An expansion and diversification of feedstock would by necessity cause disruption in the PGM and chrome production and income streams, but the potential long-term gain far outweighed the short-term sacrifice. The disruption was expected to mostly impact the 2022 financial year.

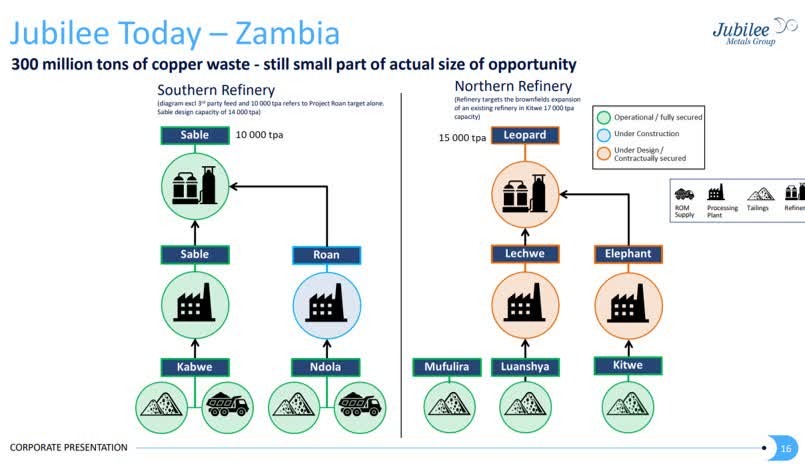

Jubilee signed up Project Roan in August 2020 and aimed to commission a new copper concentrator at Project Roan by Jan 2022. The initial copper production target for the southern Zambia production stream was set at 10,000 tonnes per annum. Sable and Roan combined for 10,000 tonnes per annum with capacity to increase to 14,000 tonnes per annum. The northern Zambia strategy incorporating new acquisitions, and named Leopard which includes Elephant and Lechwe, targets production of 15,000 tonnes of copper per annum with capacity to increase to 17,000 tonnes per annum. Achievement of the 25,000 tonnes combined target was initially set for four years. Jubilee then announced that they had, post the 2021 period under review, entered into a deal with Mopani Refining Facility in northern Zambia which will allow the 25,000 tonnes per annum target to be achieved in two years rather than four years.

JMG Website Corporate Presentation

The unique positioning of the company was once again reiterated when an opportunity arose to investigate “quite sizable”, believed to be high grade in both copper and gold, mine waste dumps in Cyprus for potential retreatment and beneficiation. The Jubilee dealmakers signed an option and commenced research and testing of the mine dumps. Dealmaking also progressed across all the other minerals being produced by Jubilee.

Jubilee achieved its stated target of 50,000 PGM ounces, by producing 50,162 PGM ounces for FY2021, year-end 30 June 2021, (2020: 40,743). PGM revenue more than doubled to £88.8mil (2020: £34.6mil). All in cost per PGM ounce produced US$537 (FY2020: US$541). PGM revenue per ounce $2,248 (2020: $1,070).

Jubilee produced 751,223 tonnes of chrome concentrate (2020: 377,883 tonnes), doubling chrome revenue to £34.5 mil (2020: £17.2mil).

Copper production, as part of enabling operational readiness, reached 2,026 tonnes and Sable Refinery achieved positive earnings.

Jubilee entered the 2022 financial year with its Inyoni Project under construction to transform it from a single feed facility to a multi feed facility. The project was completed on time and within budget, commencing new format production in March 2022, just 3 months before the 30 June financial year end. The expanded multi feed plant was also optimized with the latest know-how of Jubilee, expanding overall operations by 45% with capacity of 44,000 ounces PGM production and 1.2mil tonnes of chrome concentrate capacity (up 85%). Early production costs savings on PGM’s indicated a cost reduction of around 10%, on top of already spectacularly low production costs.

Copper production in Zambia accelerated with Project Roan achieving expected production capacity in September 2022. Project Roan produces copper concentrate for refining to cathode copper at the Sable refining plant. The copper production target for the full financial year ending June 2023 was already 10,000 tonnes making excellent progress towards the overall target of 25,000 tonnes of copper, a target set for achievement within two and a half years of entering Zambia.

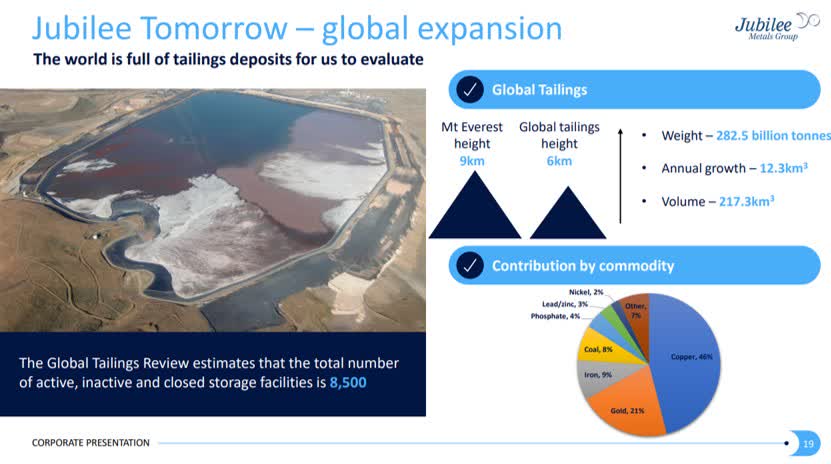

Some clarification of Jubilee’s copper ambitions in Zambia will give context to that 25,000 tonnes target. Jubilee is well aware of the total opportunity available to them, and it is huge.

JMG Website Corporate Presentation

The investment case for Jubilee is not about the price of copper or PGM’s for the next 12 months, that’s the approach towards a mature mineral producing entity. Jubilee is just beyond proving its business case with exceptional economics and leading IP. Their growth journey is just starting, and the opportunity is almost overwhelming. They have rebuilt and realigned the company on a shoestring budget with very little new capital or even debt support yet achieved constant exponential growth. The ambition for Zambia where they have access to copper mining waste accumulated over many decades and estimated at more than a billion tons of waste material, goes far beyond just 25,000 tonnes of annual production and an “old, dilapidated refinery” (Sable). From the 2022 EC.

Step 1

“And that took us to Zambia in end of 2019 where we acquired an old dilapidated refinery, set a target to repurpose that refinery, recapitalize it while building a new greenfields copper concentrator to process the perceived waste, to produce a copper concentrate that we could refine to metal, to implement the first fully dedicated waste to metal copper facility in Zambia.”

Step 2

“…because everything we’ve done in Zambian copper is purely a demonstration. As significant as it might be, it’s as pure demonstration to the industry and to Zambia of what is to come as we now step from the southern refining copper into the northern refining copper, where we look to expand on a multiple of size compared to what we’ve done in the south.”

No fancy PR, just some straight, honest talking directly from the CEO, no frill no fuss. We’ve rebuilt a new Jubilee, placed it on a sound financial footing, have grown production, revenue, earnings and expanded its production footprint but please do be aware that what we have done so far is simply a demonstration of what we a really capable of doing. No boasting, just a matter-of-fact delivery. Is, was anybody listening? No analysts, no press, nobody to take notice present at the earnings call. The last time anybody wrote an article on Jubilee for Seeking Alpha was in 2010 (oh no, that article is misallocated and has nothing to do with Jubilee, so the answer is never)! Now that’s what I call an uncrowded value opportunity.

JMG Website 2022 AFS

I digress, let’s get back to the 2022 results. The 2022 financial year was a steppingstone year, a year of consolidation and expansion. PGM prices dropped by between 30% and 40% during this period with revenue per PGM ounce declining from $2248 for 2021 to US$1 615 for 2022, a decline of just over 28%. One would expect that, with Inyoni under construction for ¾ of the financial year returning to full production only in March 2022 and a 28% decline in the most important income and profit generator, that results would slip badly in 2022. It slipped but not by much given the circumstances.

Revenue unexpectedly increased to £140mil (2021: £132.85mil). Operating profit dropped to £25.64mil (2021: £45.38mil). Profit before taxation dropped to £26.5mil (2021: £43mil). Earnings per share (pence) dropped to 0.73pence (2021: 1.81pence).

Revenue per PGM ounce $1,615 (2021: $2,248). Cost per PGM ounce net of byproduct credit $408 (2021: $456). Chrome revenue £71.15mil (2021: £34.91mil). Net copper revenue £18.3mil (2021: £8.92mil). Revenue per copper tonne $9,210 (2021: $8,657). Cost per copper tonne sold $5,386 (2021: $5,076).

Growth focused Financial Analysis

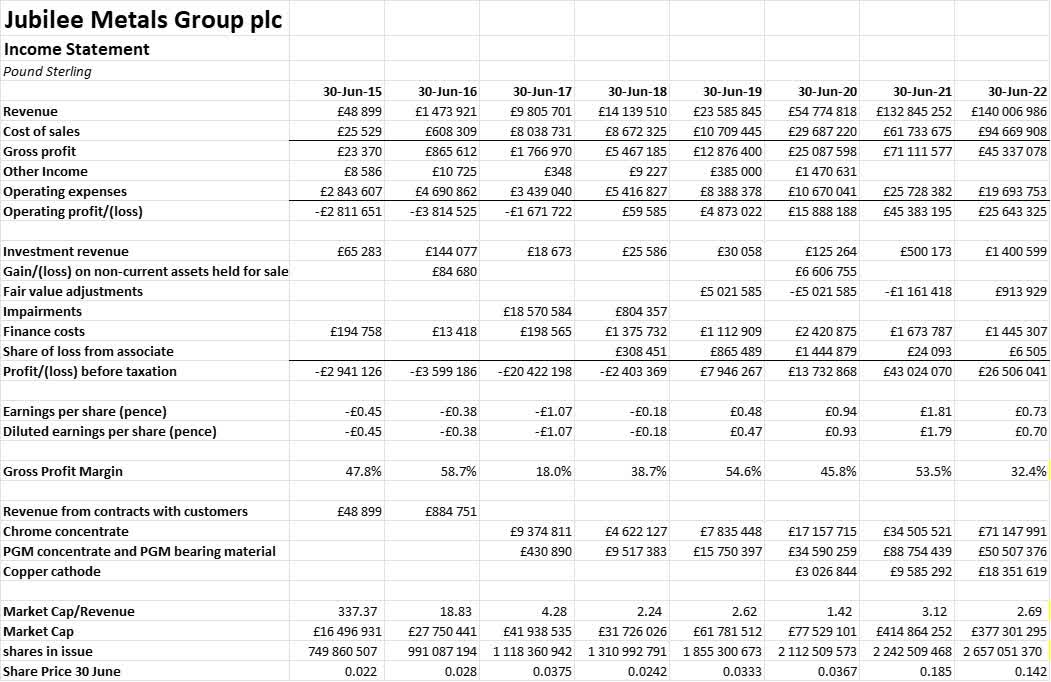

This is the reported Income Statement of the new Jubilee from that watershed 2015 strategic change in direction.

Sarel Oberholster compiled from the AFS’s published on the website of JMG

The growth in Revenue, Gross Profit, Operating Profit and Profit before tax is nothing short of spectacular. We see the expected pull-back in 2022 as a result of repositioning for a new phase of hopefully equally spectacular growth. Perplexing is that the share price performance is shockingly lagging the growth performance but there is a very good reason for it.

Jubilee has been financing growth from its own cash generation and the shortfall to finance that growth was obtained from issuing new shares mostly through issuing warrants. That was a safe and prudent approach, but it weighed heavily on the share price, creating a very unusual appreciation opportunity. Jubilee is also almost without debt and probably far too conservative with regards to its debt management. Accessing growth capital via share warrants was a blessing and a curse for Jubilee, giving it a protected growth opportunity but at a very steep capital cost.

The need to continue to tap into new share issues via warrants is fast dissipating given the investments in new growth and those investments already generating cash (see below). The share price has appreciated somewhat which helped limit the new issuance requirement. More important is that the investments in new growth are about to catapult the company to a new level and the share price should follow. I would also expect a lot more investors to start taking a keen interest in Jubilee.

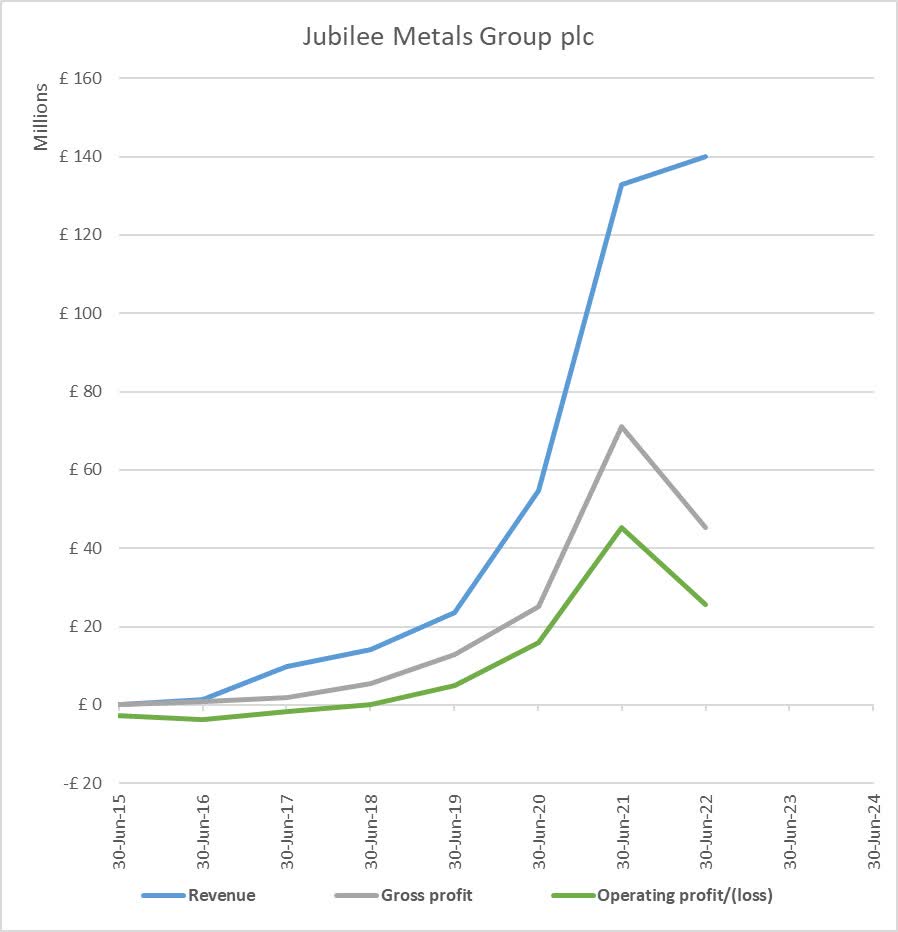

This is what the growth story looks like from 2015.

Sarel Oberholster, data from JMG

Growth momentum in revenue is maintained even during the repurposing of its main production unit but losing some production and depressed PGM prices saw profitability decline.

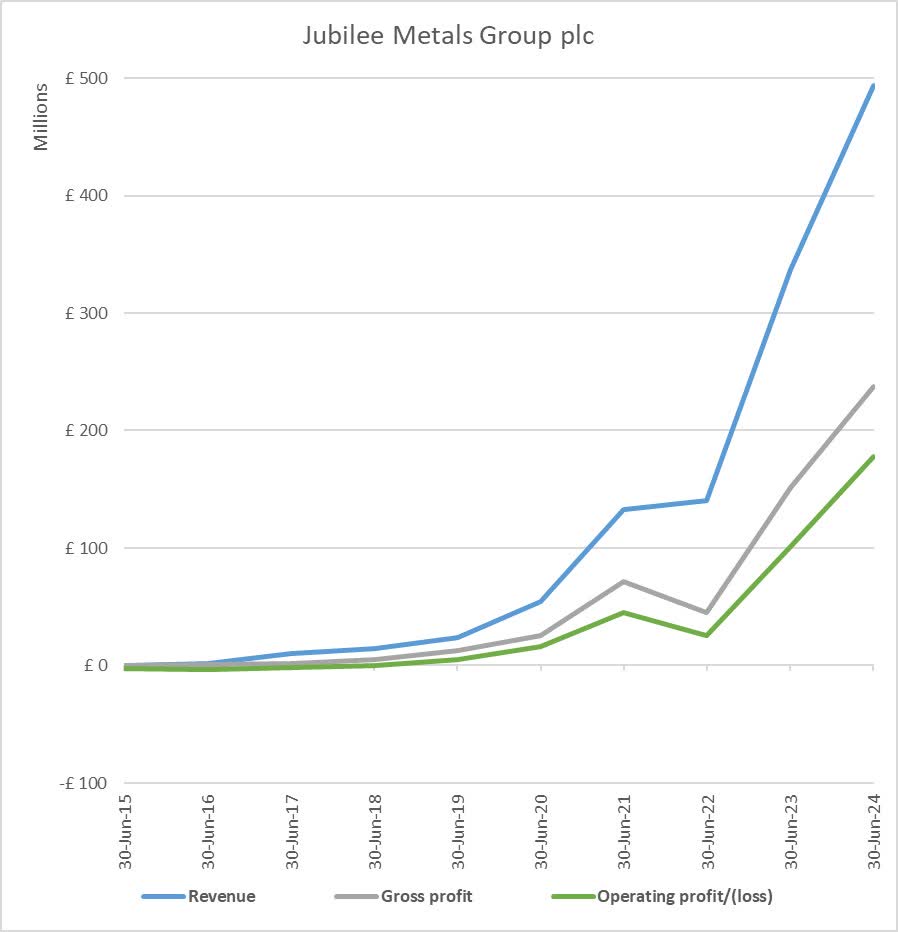

The question now is how will the growth initiatives play out once production capacity levels are returned?

The first calculation is to test revenue at the new capacity levels, then to estimate gross profit and operating profit. This is my expected scenario:

- Chrome concentrate production is expected to increase to 1.9mil tonnes by 30 June 2023 (up 55% from 1 222 452 tonnes in 2021 mostly as a result of an 85% increase in capacity at Inyoni) and to 2mil tonnes by 30 June 2024. An average chrome price of £62 per tonne is applied compared to around $67 in 2022 and an average chrome price of £68 is applied to June 2024, based mostly on demand pressure from the reopening of China.

- PGM ounces for FY2023 is estimated at 57,000 ounces (compared to 50,162 ounces already achieved before the refurbishment at Inyoni) and 62,000 ounces for FY 2024 as at 30 June 2024. The PGM basket price for FY 2023 is set at $2,000 and $2,100 for FY 2024.

- Copper cathode production is set at 14,000 tonnes for FY 2023 given that capacity production at Roan was already achieved in September 2022 (AFS 2022, p36) and at 24,000 tonnes for 2024 just short of the targeted 25,000 tonnes. The copper prices applied were $9,200 per tonne for FY 2023 and $11,000 per tonne for FY 2024.

- Jubilee has been very successful at achieving economies of scale on their projects resulting in Gross Profit percentages (“GPP”) of less than 50%. A 45% GPP is applied for FY 2023 and 48% for FY 2024.

- Operating expenses are estimated at 15% of revenue for FY 2023 and 12% of revenue for FY 2024. This is a difficult estimate and some margin of error, positive or negative is likely.

I’m reasonably satisfied with this scenario but also believes that the outcomes risk is that I may have been too conservative rather than to the downside. Here is the result.

Sarel Oberholster, data from JMG

The success of implementing a dual strategy of growth in copper while also repurposing the Inyoni plant jumps right at us.

Sarel Oberholster, data from JMG

The spectacular growth up to 2022 now looks positively pedestrian. And the CEO had taken pains to explain that this is just the beginning, just a demonstration! It is highly likely that Jubilee will attempt to scale £500mil in turnover by June 2024 and with economies of scale post an operating profit pushing £180mil. They have a history of containing general and financing costs, which suggests that the company could increase net profit before tax fourfold to over £100mil by June 2023.

The share price does not reflect any of the above growth nor any of the longer-term strategic growth as a result of the warrants issuance strategy, and because the company is essentially unknown to most investors. The Jubilee team is totally task orientated and focused on developing their technologies and plants, reveling in the operational successes.

That is why I had told you the story of this company from its inception, warts and all, so you can get a sense of its character, its dedication, success achieved with minimal financial resources and support, and spectacular success achieved in spite of significant headwinds.

I have indicatively valued the company’s shares based upon revenue growth at 41 pence against its present around 12.5 pence share price, but that calculation does not capture a reasonable allocation to the strategic growth potential. I therefore place a target price of 50 pence on the share based upon the expected results for FY2023 which should be available by early August 2023. Interim results should be available by late March 2023 and together with an update of the corporate presentation should provide more than adequate confirmation for the expected 2023 full year results. My price target for FY 2024 is 80 pence. I will do a full review once interim results are published.

Risks to this investment thesis

- This is a penny stock and a relatively small company which can result in very significant share price movements and volatility.

- Jubilee has published the company specific risks in its AFS pages 26 to 32.

- The most important risk for a seller of minerals is that the price of its products is established internationally outside of its control and significant movements in those prices can and will have a material effect (positive or negative) on any investment case. Here it is very relevant to mention that the Jubilee strategy of primary mineral and byproduct mineral with subsidized costing has proven resilient in the face of declining prices. The diversification into a larger basket of minerals and adding additional “circuits” for mineral recovery further support that resilience.

- The jurisdictions within which Jubilee operates have political and infrastructure risks for which it must have a proven competence to manage, and it does, but it may cause disruptions from time to time.

- Jubilee is a leading innovator in the extraction of PGM’s and base metals from mining waste, but all innovation carries greater risks. Jubilee has been very successful at managing its innovation risk and maximizing gains from it.

- All production at Jubilee depends upon the smooth and on purpose functioning of plants which they design and build. Breakdowns or failures can alter the investment outcomes.

Conclusion

Jubilee Metals Group plc has built a company of substance under the radar of most investors with a unique new approach steeped in metallurgy, technology, and innovation. Is this a mining company with incredible IP and technology or is this a technology company involved in mineral reclamation and beneficiation? You decide, but it has proven its business case over-and-over, growing spectacularly on a shoestring budget while almost all its successes went unnoticed.

This had created one of those rare opportunities where shares are undervalued, underappreciated and almost unknown. Those unique value investment opportunities which are so seldom encountered. The intrinsic value of this company’s technologies and IP is simply not recognized in its share price or in its financial statements, yet it’s there and proven in its growth and the many remarkable successes.

Management of this little gem is task orientated, spending little time on PR, dancing girls, or dog and pony shows. They keep toiling operationally, calling money by way of very expensive warrants from time to time when they want to implement yet another growth initiative. They are technically skilled, innovative, dedicated, entrepreneurial and excel at deal making and execution. New projects are initiated and brought to fruition with speed, skill and above all with excellent profit margins in place, then further improved and economies of scale harvested. They do not just grow revenue and hope for profits later, they grow revenue and profits together! What else would one want from the management of a company one wants to invest in?

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment