naphtalina/iStock via Getty Images

The iShares Global 100 ETF (NYSEARCA:IOO) is mostly just a US ETF. Where it isn’t US exposed, it’s mostly consumer staples which can be relied upon in most economic scenarios that we can expect. Overall, we think there are reasons to be optimistic about the broad economy. Firstly, declines have already happened, and the increment should be positive. While we expect rates to continue to rise for a while longer and broadly pressure equities, we don’t think that it’s going to last. Major markets are devaluing, such as residential housing (and hopefully soon rents), and we’re seeing a reversal in commodity prices and a loosening in bottlenecks like logistics. Things are worse than before, but we’ve already had the appropriate correction. The US in particular is going to benefit from the new world order that sees Russia out of the western hemisphere and Europe dependent on US trade while paying the bill for ostracising Russia. They are already showing resilience, and it’s likely to be a flattish situation for the next year followed by resumed growth.

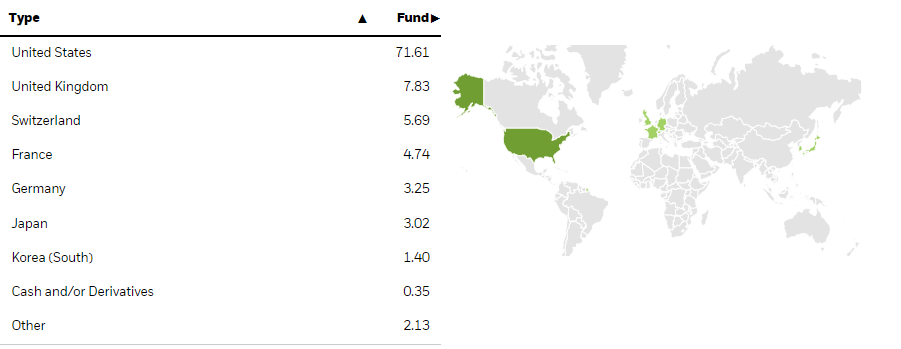

IOO Breakdown

The geographical breakdown shows that the majority of the exposures are in the US.

Geography (iShares.com)

The exposures in the UK and Switzerland are often healthcare oriented, like Novartis AG (NVS) or AstraZeneca (AZN). Their exposures in terms of markets are not excessively towards the EU, no healthcare company has large EU wallets because there’s so much more money to be made in the US, but they are listed in those countries.

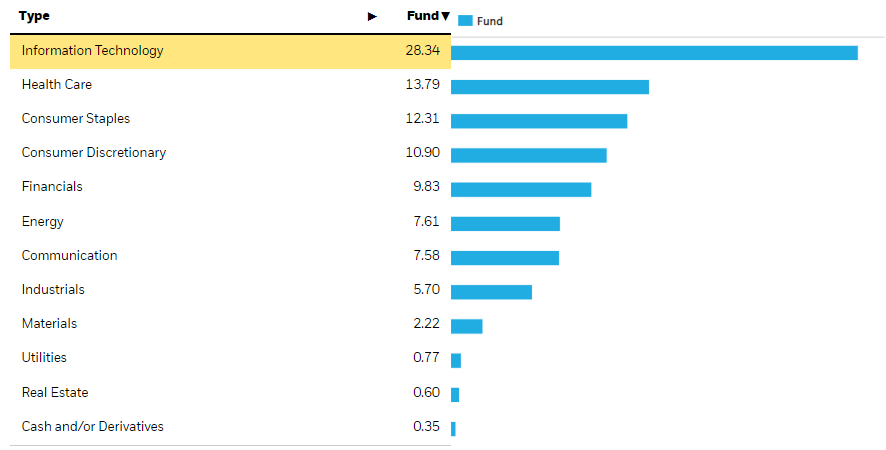

Sectoral Exposures (iShares.com)

Sectorally, the exposures end up being mostly in tech, reflective of the high US weighting in this ETF, and then in healthcare and consumer staples. Healthcare and consumer staples, which includes more European exposures than tech, should both be resilient, even if demand is much softer in Europe than in the US. The tech exposures are substantially in the US and will drive the IOO.

Bottom Line

Why do we trust in US markets? We think that the geopolitical supremacy of the US has been utilised fully in the current economic regime, and will keep the US’ head above the economic riptides caused by the major dislocation in energy markets.

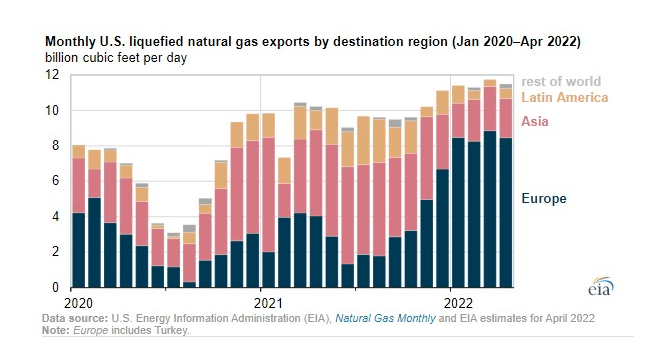

Firstly, the US is self-sufficient. While inflation is happening there, lots is demand driven. Energy prices and energy bills haven’t inflated to the same extent. The other thing is that the dangerous markets have had people rushing to safe haven currencies like the dollar. While rate hikes are going to cool down the US economy, especially as the US rate hikes are so much higher than in EU and Japan, the momentum in safe haven assets like Treasuries, now yielding higher, has weaponised the dollar. It values highly their energy sector which is dollar denominated, and forces exchange in dollars as it’s the reserve currency for energy, and it also improves the current account deficit and US finances, because export will be strong despite a more expensive currency since the US is a major alternative partner for energy trade, especially for LNG. LNG used to get flared off since it was so cheap that its economic value was negative comprehensive of storage and transport costs, while now it’s a profitable commodity.

US LNG Export (api.org)

It has also been good for important industries like defense and strategic technologies.

At any rate, the US is doing good, while the EU is doing really bad and taking the brunt of the fallout from the Russian invasion. The reserve status of the dollar and a well-timed rate cycle have for now insulated the US from damage. Jobs reports are still strong, inflation is peaking as supply side factors recede, and earnings aren’t bad. An unemployment-earnings decline spiral is nowhere in sight. A major recession is not going to happen.

Meanwhile, a resilient IOO is discounted 13% YTD, despite strong healthcare and consumer staples exposures. Tech will see headcount reductions, and is already seeing signs of pressure especially those with ad exposure, but the secular tailwinds remain in the growing cloud industry and other sectors that represent a large share of US tech value. The downside with the IOO is the pretty high expense ratio for a passive ETF at 0.4%. While the PE is smaller at 16.5x because of more European exposures compared to the iShares Core S&P 500 ETF (IVV), which is at 19.7x, the higher expense ratio is a pain for long-term, diversified allocators. Since the IVV and the IOO are going to be very driven by the US, probably the IVV is a better broad bet. Still, we are optimistic about the US economy as it wins geopolitically.

Be the first to comment