Feverpitched

Introduction

Similar to many companies, 2022 was a difficult year for Barrick Gold (NYSE:GOLD) who saw their share price sell-off significantly but as my previous article highlighted, this left their shares representing the best deal in over 30 years. Subsequently, it was not a smooth ride, with rapidly tightening monetary policy weighing down their share price. As we now head into 2023, oddly, it seems that shareholders can simply sit back and wait for bad news on the economy that should actually bring about upside potential for their shares as the Federal Reserve pivots to a dovish stance, as discussed within this follow-up analysis.

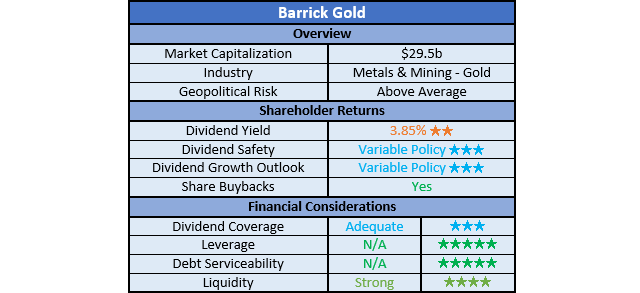

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

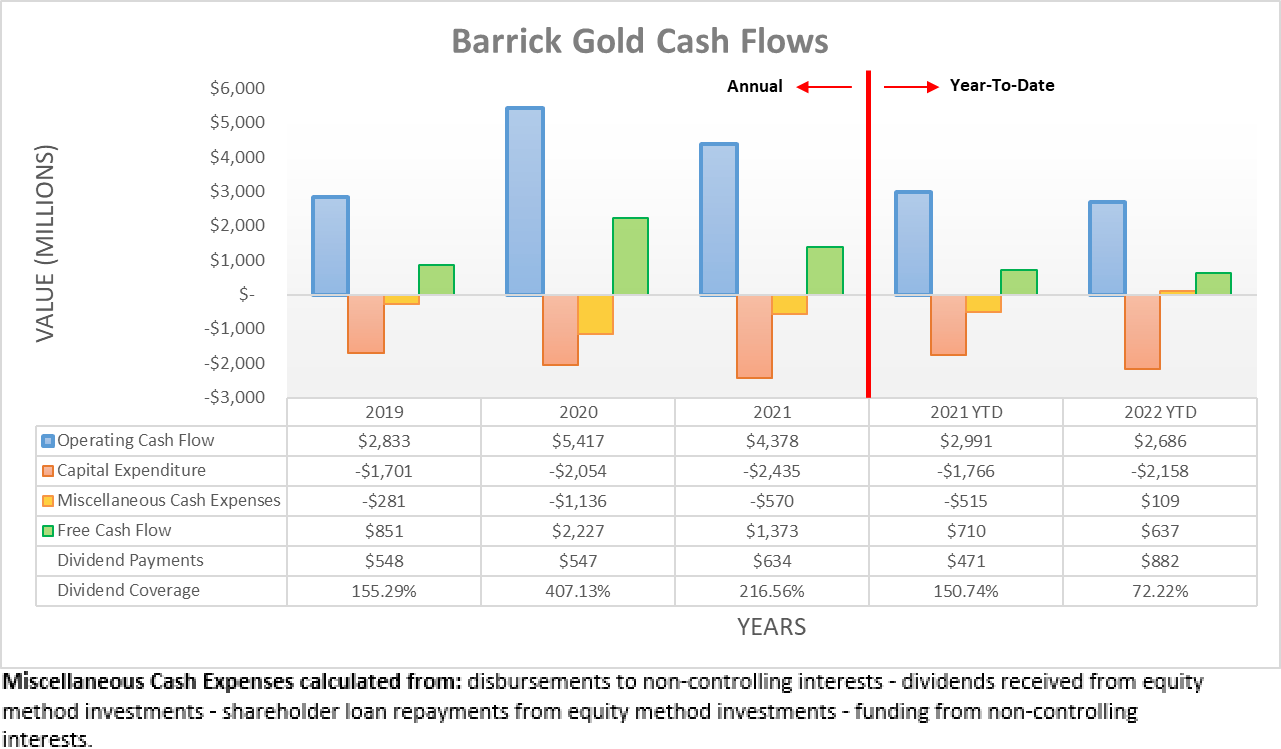

The second quarter of 2022 saw soft cash flow performance and disappointingly the third quarter was weaker sequentially once again. This was largely due to gold prices falling further from $1,861 per oz to $1,722 per oz across these same two points in time, as per their third quarter of 2022 results announcement. As a result, their operating cash flow during the first nine months landed at $2.686b and thus down slightly more than 10% year-on-year compared to their previous result of $2.991b during the first nine months of 2021.

Author

If viewing their quarterly operating cash flow, it easily shows their result of $758m during the third quarter of 2022 was the lowest since their previous result of $639m during the second quarter of 2021. However, the latter was weighed down by a larger working capital build than the former that, if excluded, sees their underlying result during the second quarter of 2021 at $836m and thus actually above their latest result of $810m. This means the third quarter of 2022 was the weakest quarter since at least the beginning of 2021 and furthermore, it was accompanied by capital expenditure of $792m, which consumed the entirety of their operating cash flow.

Whilst their financial performance is interesting, their outlook for the future heading into 2023 is far more important, especially in light of these abnormal times. Obviously, gold prices will continue playing a central role influencing their results, which are inherently volatile, similar to every commodity. The biggest influence on gold prices throughout 2022 was the Federal Reserve hiking interest rates rapidly to combat high inflation, thereby tightening monetary policy far greater than myself and many others expected earlier in the year. As a result of their hawkish stance, it strengthened the USD to levels not seen in decades, which in turn placed downward pressure on gold prices.

This dynamic continues to play out throughout recent weeks, with gold prices climbing certain days on signs of weaker economic conditions and accompanying prospects for the Federal Reserve to make a dovish pivot on the back of lower inflation. Or alternatively, signs of economic strength that foretell continued high inflation and thus a continued hawkish stance have also seen gold prices dropping on other days.

Thankfully, there are reasons to expect a change heading into 2023, oddly because of the outlook for bad news on the horizon, economically speaking. Whilst the November employment numbers remain particularly strong, as widely discussed throughout recent months, this is expected to change during 2023 as the dramatically higher interest rates take their toll on the economy with many in the market seeing a recession as likely or if not, weaker economic conditions. Elsewhere, the United States treasury yield curve is inverted, which means that longer-dated yields are lower than shorter-dated yields. Apart from signaling a recession on the horizon, it also signals the Federal Reserve is expected to end their interest rate hikes or, possibly, even start cutting during 2023.

Even though a recession is normally considered bad news, it should ease inflation and, thus, finally see the Federal Reserve pivot to a dovish stance. By extension, this should also weaken the USD from its recent incredible strength, thereby providing a boost for gold prices and as a result, their financial performance. Apart from creating upside potential heading into 2023, it also makes their shares a hedge against market turmoil that may arise as economic conditions falter.

Barring a sudden black swan event, I cannot imagine the Federal Reserve getting more hawkish than as seen during the last few months with respect to both the pace at which interest rates are increasing and the expected length of time they are to remain elevated. When combined with the recent gold price rally, I suspect the worst is now over and whilst no one can necessarily predict down to the month when the Federal Reserve will pivot, the day will eventually come, likely in 2023.

Author

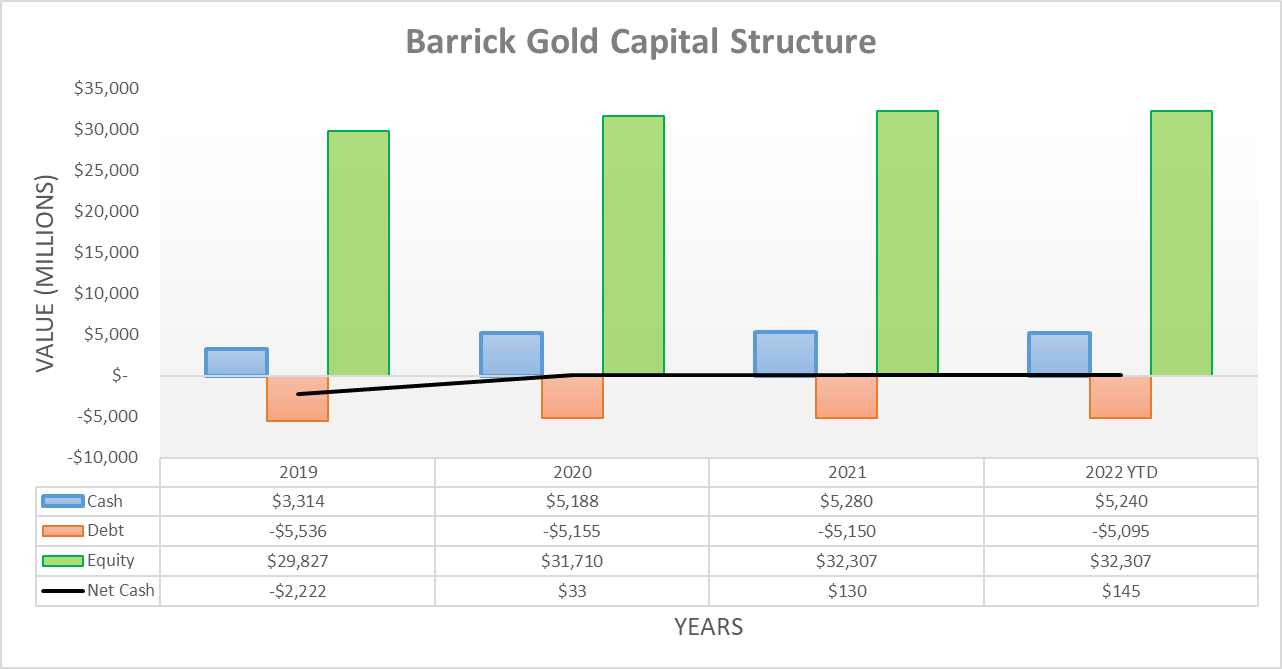

Following their lack of free cash flow during the third quarter of 2022, it saw their shareholder returns drawing down their net cash position, which plunged to $145m from its previous level of $636m following the second quarter. As a result, their net cash balance is now sitting beneath $500m and as such, their dividends attributable to the third quarter were cut to $0.15 per share, thereby in line with their variable dividend policy that links payments to their net cash position at the end of the quarter, as outlined within my other article when this policy was first unveiled.

Going forwards into 2023, their cash flow performance will continue fluctuating with gold prices and therefore, so too will their net cash position along with their dividends. Whilst the future remains uncertain by nature, the prospects for the Federal Reserve pivoting to a dovish stance skews the outlook towards the upside instead of the downside, at least in my view. If nothing else, their financial position is clearly rock solid, which affords them the luxury of waiting and thus by extension, it obviously would be pointless to assess their leverage or debt serviceability in detail because they clearly have zero leverage, nor any issues with interest expenses.

Author

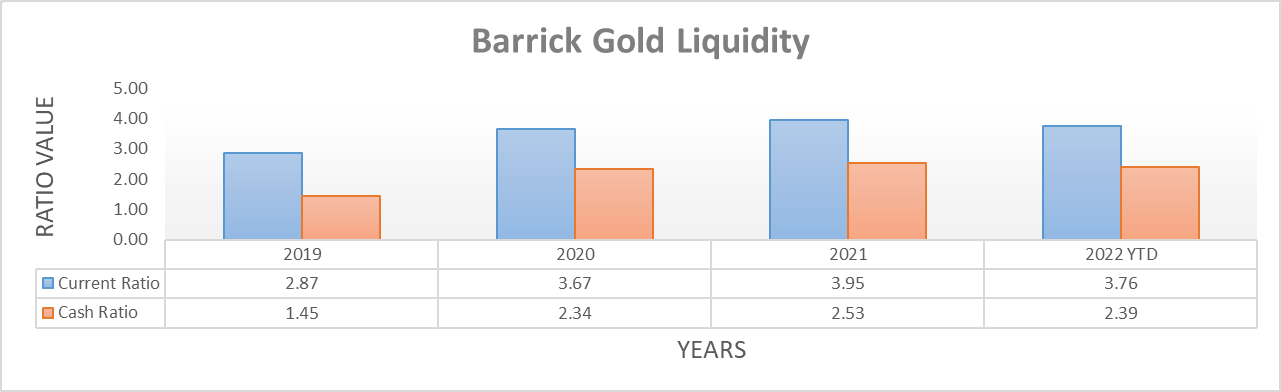

Even though the third quarter of 2022 endured weaker financial performance, their liquidity easily remains strong with a current ratio of 3.76 and a cash ratio of 2.39, which are only down slightly from their previous respective results of 3.95 and 2.59 following the second quarter. Going forwards into 2023, this should not change given their variable shareholder returns policy and accompanying net cash position. The latter of which also removes any issues regarding future debt maturities, even though as one of the largest gold mining companies, they should retain easy access to debt markets if required, regardless of where monetary policy heads.

Conclusion

Oddly, what is normally considered bad news is actually good news in this situation, as a recession or if not, weaker economic conditions, should see the Federal Reserve pivot towards a more dovish stance compared to their presently very hawkish stance. In turn, this would remove one of the key pressures currently weighing down gold prices and thus create upside potential, despite otherwise deteriorating economic conditions elsewhere.

Even though reaching this point may take months, if not a number of quarters, they are one of the largest gold miners in the world and carry a financial position whereby the discussion centers around its net cash position, not its debt, which means they can afford the luxury of waiting. In my eyes, it seems the worst for gold prices is over barring any sudden black swan events with the Federal Reserve already as hawkish as possible. When wrapped together, I see no reason to believe that my strong buy rating is no longer appropriate, especially as their shares could double as a hedge against market turmoil during 2023 as the economy weakens.

Notes: Unless specified otherwise, all figures in this article were taken from Barrick Gold’s SEC filings, all calculated figures were performed by the author.

Be the first to comment