Michael Vi

Merger Arbitrage

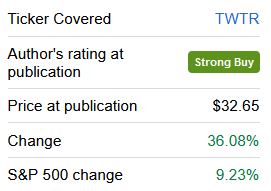

Here’s one more for the Golden Age of Merger Arb basket. My favorite of the bunch remains Twitter (TWTR).

SA

And my favorite way to play that remains buying calls, specifically June 2023 TWTR $47 calls. They traded at $2.25 when I first offered the idea, $4.20 when I reiterated it, and are still worth buying at $4.75 today. If the deal closes on original terms, they will be worth $7.20 for a better than 50% return. How long will this take? Probably wrapped up by year-end or so.

Who?

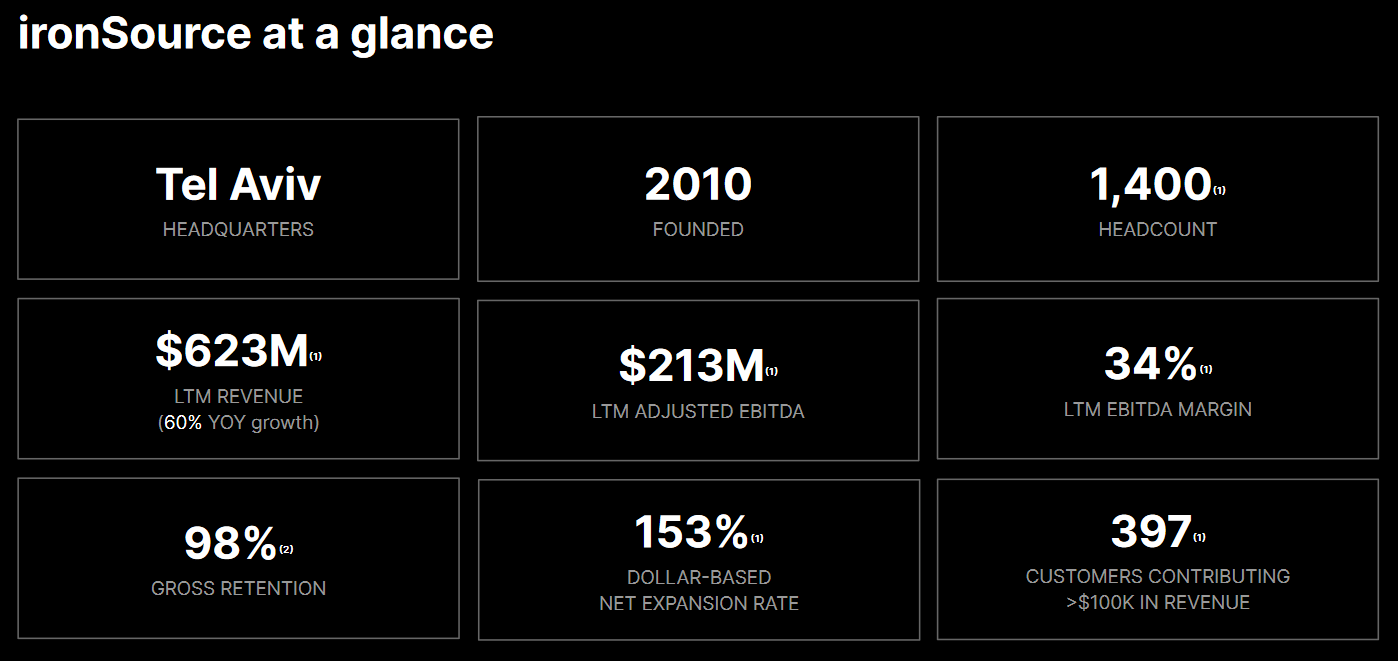

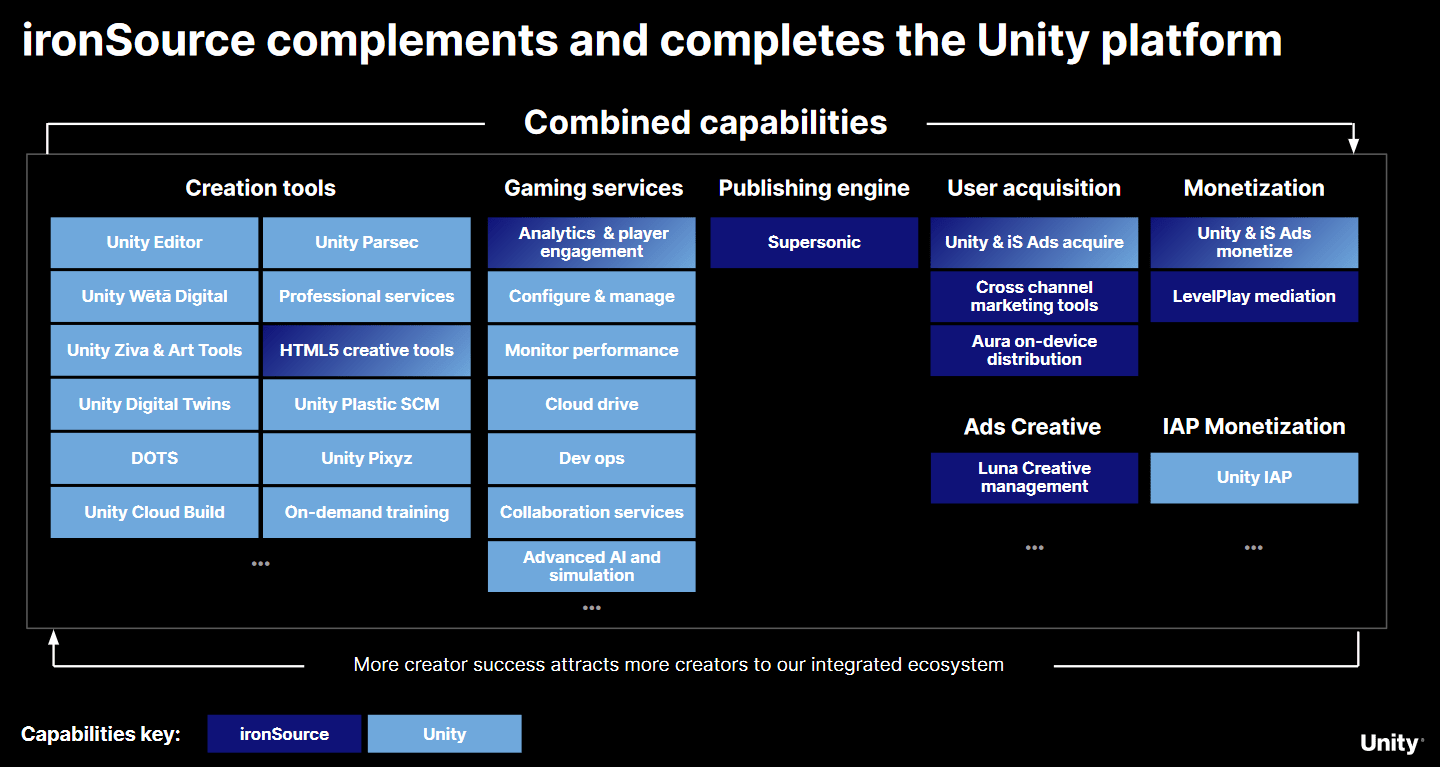

ironSource (NYSE:IS) is a business platform to support app developers and telecom operators.

IS

What?

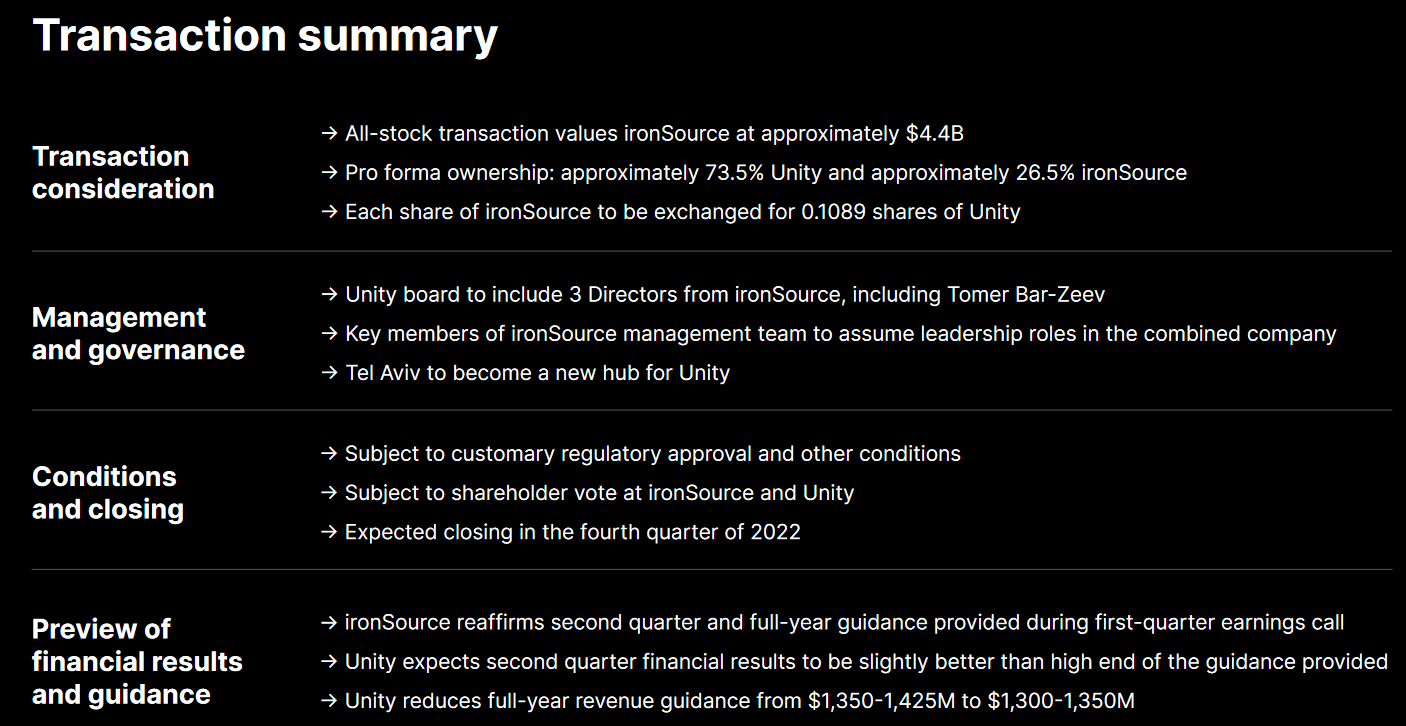

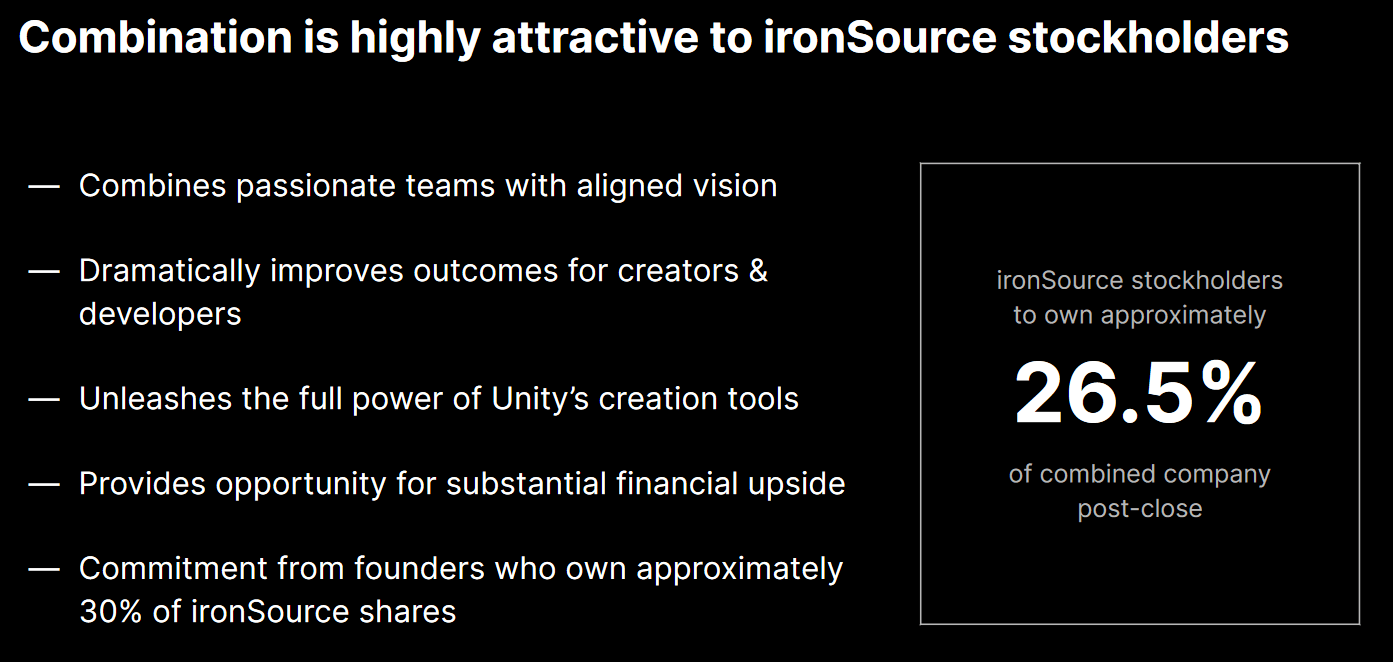

Unity (U) signed a definitive agreement to buy ironSource for 0.1089 U shares per IS. The deal is subject to approvals by both sets of shareholders, as well as regulatory approvals in the US and Israel. Israel needs to grant Registrar and ISA/.ITA clearances.

IS

When?

The deal will probably close by year-end.

IS

Where?

ironSource is located in Tel Aviv, Israel, and does business internationally.

Why?

The $1.41 net spread offers a 78% IRR if the deal closes by January 2023.

IS

Caveat

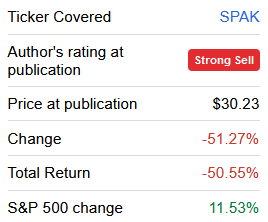

AppLovin (APP) made a non-binding offer for Unity conditioned upon their terminating this deal. Unity abandoning their current deal for that one is the biggest deal risk for IS. Additionally, IS’s history has not been a happy one for shareholders; it has been yet another disappointing de-SPACed equity. They have almost all been terrible. One convenient way to just short the whole lot of them is via Defiance NextGen SPAC IPO ETF (SPAK). I thought it was a strong sell last year.

SA

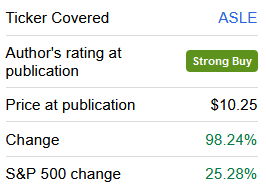

I think the same this year. Exceptions are few and far between (and fewer than I thought over the past few years… I was 90% skeptical, but should have been 99%). One of the vanishingly few exceptions remain AerSale (ASLE).

SA

It was a huge opportunity in its IPO at $10 (even setting aside the value of the free warrants) and has since doubled to $20. I expect it to double once more after their AerAware engineered product hits the market.

AerAware is my favorite one [proprietary engineered solutions]. I love it… We are very close to certification on it. We have a number of customers big and small… It is something we believe will be ubiquitous to the airlines industry… We expect margins in excess of 50% on engineered solutions.

– AerSale CEO, Nick Finazzo

Conclusion

Unity has strong corporate defenses and is unlikely to be successfully acquired on a non-consensual basis. They have a large voting agreement in favor of the current deal. The unsolicited bidder didn’t offer much of a premium and their shares reacted poorly to the offer, which constrains their ability to aggressively bump the bid. Further constraining the hostile bidder, they have a smaller market cap than their target. They are reliant on the unusual route of making a hostile bid with all stock, which has less scope to work. For those reasons, the best bet here is on ironSource.

IS

TL; DR

Buy IS.*

*Is this the shortest TL; DR ever?

Be the first to comment