DNY59

The recent bout of market volatility – or, if we’re honest, all of 2022 – has brought inverse products into focus once more. There are countless inverse stock exchange-traded products that short indices, or even individual stocks, if you want to express a bearish stance. However, one way traders have been able to express those bearish positions for some time now is through volatility proxies.

The VIX is a measure of volatility that is derived from options prices. If traders are paying more for options – implying higher volatility levels – the VIX rises. This tends to happen during weak periods in the market, so by extension, being long volatility has had a pretty strong correlation to being short stocks during past periods of market turmoil.

That led to a variety of exchange-traded products that try to track volatility, because the VIX cannot be directly traded. One of the more popular options is the iPath Series B S&P 500 VIX Short-Term Futures ETN (BATS:VXX), which, as the name implies, tracks short-term VIX futures. You can read about the ETN here.

What is VXX?

In short, VXX offers exposure to a daily rolling long position in the two most forward months in the VIX futures curve. For instance, right now VXX has ~80% of its money in October VIX futures, and the balance of 20% in September futures. The balance changes throughout the month but basically, VXX owns what amounts to current VIX futures in an attempt to mimic the spot price of the VIX.

In practice, this should allow investors to have a piece of the action when it comes to the VIX, but as we’ll see, this product has significant tracking error, and in general, hasn’t necessarily correlated with the direction of volatility in certain cases.

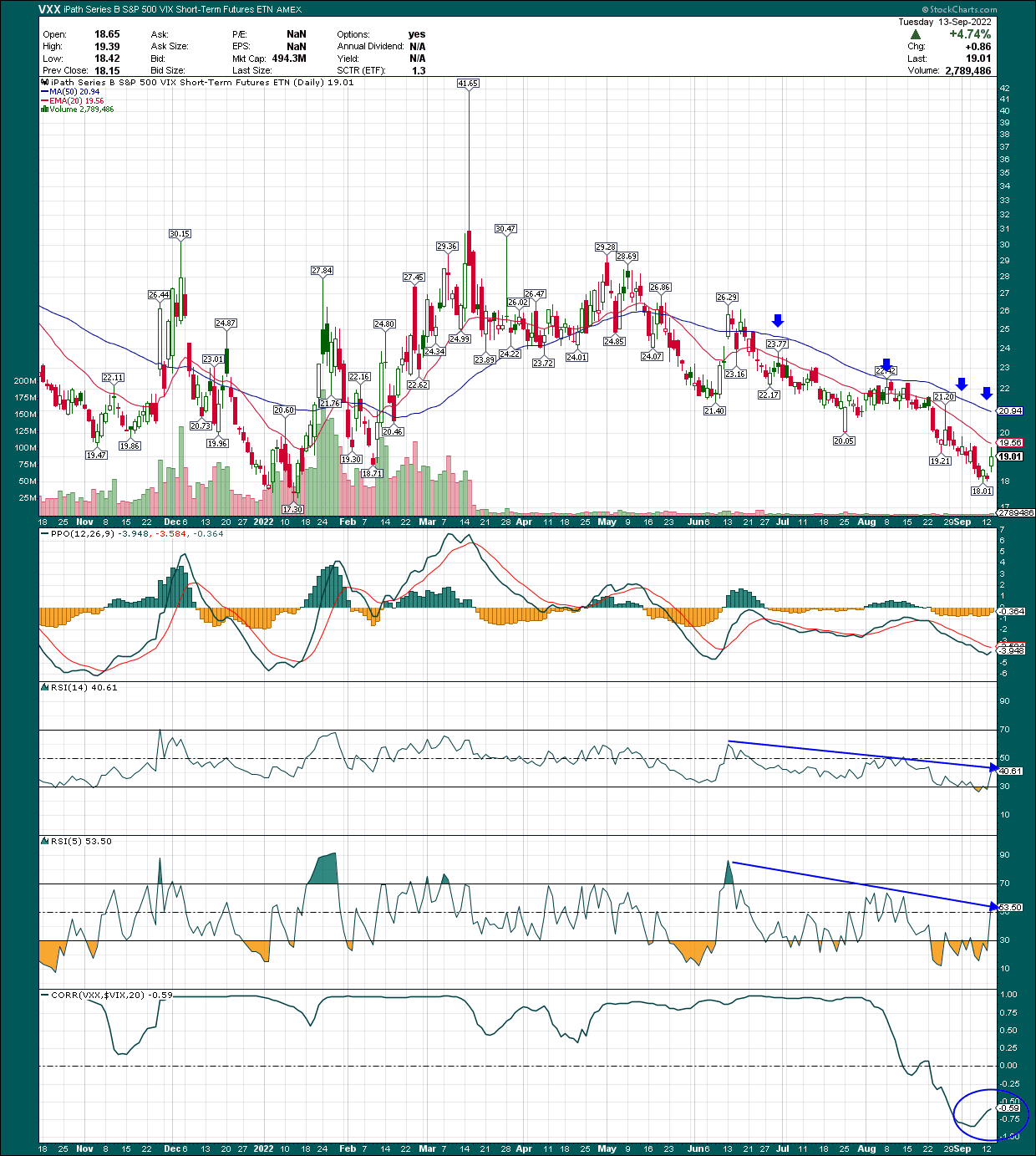

An ugly chart

Let’s start with a look at the chart to get us going on a big reason why I don’t think VXX is worth your capital.

StockCharts

We can see huge spikes and declines in VXX over time, which you’d expect during tough market periods. The VXX should rise during equity selloffs, and sometimes it does. However, the VXX doesn’t correlate really much at all with the VIX at this point, meaning if you buy VXX, it may not being doing what some investors would expect it to do.

The bottom panel in this chart is the 20-day (about a month of trading activity) rolling correlation of VXX to VIX, which should be reasonably positive considering the objectives of the fund. At times, it has been very high, as you can see above, implying VIX and VXX move in the same direction. Today? That correlation is -0.59. We can see that since the beginning of August, VXX is actually moving in the opposite direction from the VIX, and in a big way. This may confuse investors that think they’re buying somewhat direct exposure to volatility. Indeed, this is a big departure from how VXX and VIX have traded in relation to each other in the past. It’s something to be aware of.

The chart itself is ugly if you owned this product, part of which is due to the rollover costs associated with the ETN’s structure. Basically, as the fund rolls its positions from one month to the next, which happens essentially continuously, it is paying for next-month futures that are generally higher than current-month futures, resulting in frictional losses that have nothing to do with the performance of the VIX itself. That’s why the VIX is up almost 40% this year while VXX is up about 6%.

When we add in the 89bps it costs to own the VXX annually, there’s significant drag on the ETN’s value for holders.

So what do we do?

In my opinion, the first and best thing you can do relative to the VXX is to avoid buying it as even a medium-term hold. If you think volatility is going to rise over a short period, VXX could work for a quick trade. Over time, however, it loses value due to the cost of rolling over its holdings constantly, creating a massive uphill battle for the value of the fund. Could you catch an up move in volatility over the short-term? Absolutely, and one could argue that’s the value of the product. VXX does move up at times, obviously, but the odds are stacked against you given the constant drag on returns.

Second, if you’re one that is willing to take on some risk, you can either short VXX outright, or use long puts (or short calls) to express a bearish position on VXX. I would expect at some point for VXX to perhaps start to track the performance of the VIX again in some way, but right now it just isn’t, as we saw earlier. With the VIX remaining elevated in the high-20s, it will fall again as equities regain their footing. That, plus the constant rollover cost (and inherent value destruction) should lead to lower VXX prices. Even if the VIX remains where it is, the rollover cost alone should lead to an ever-declining VXX price over time.

Puts are priced accordingly, so if you choose puts as your method of shorting, just know you’ll pay a premium over a comparable call. In general, you’d expect options pricing to be efficient enough for a call and put at the same expiration and strike price to trade for roughly the same price, excluding intrinsic value. That’s not the case with VXX puts, because investors know its long-term bias is down. One way to get around this is to use put spreads, or to short calls instead. These strategies are not for everyone, but you certainly have some options, one of which is to just not mess with VXX in any capacity.

Shorting outright carries its own risks, as if there is a parabolic move in volatility, you should see some sort of large move in VXX higher. That could create big losses if you short the ETN outright, so that’s one risk to consider.

Final thoughts

Many exchange-traded products have some sort of tracking error associated with them, particularly if they’re leveraged products. However, VXX has unique characteristics, including rollover costs, that make it something investors should do significant due diligence on before buying. Noting that the VXX and VIX have decoupled in the past month is significant to say the least.

Given this, the only logical thing to do – in my view – with VXX is to either ignore it altogether, or short it in some way. Shorting carries significant risk and isn’t for everyone. But what is for everyone is avoiding buying this product under most circumstances. If you’re bearish on equities, you can either go to cash, or short equity indices, as I see those as better ways to take advantage of market weakness than VXX.

Be the first to comment