In this article, we’ll discuss two things. First of all, we are going to dive into some industrial numbers to assess whether or not it makes sense to invest in industrial companies. I’m using leading economic indicators that show an improved risk/reward as well as industry comments highlighting ongoing trends in the sector. After that, I will give you an ETF that allows you to buy diversified industrial exposure at a very fair expense ratio and favorable valuation. The Industrial Select Sector SPDR Fund (NYSEARCA:XLI) is home to a lot of my core dividend holdings, and I have little doubt that XLI will outperform the market as soon as industrial sentiment returns.

Now, let’s look at the details!

A Manufacturing Recession?

I’ve been fascinated with business cycles since I became serious about investing roughly 10 years ago. Business cycles are like low tide and high tide at the beach. While the perfect business cycle only exists in textbooks, we see cycles everywhere.

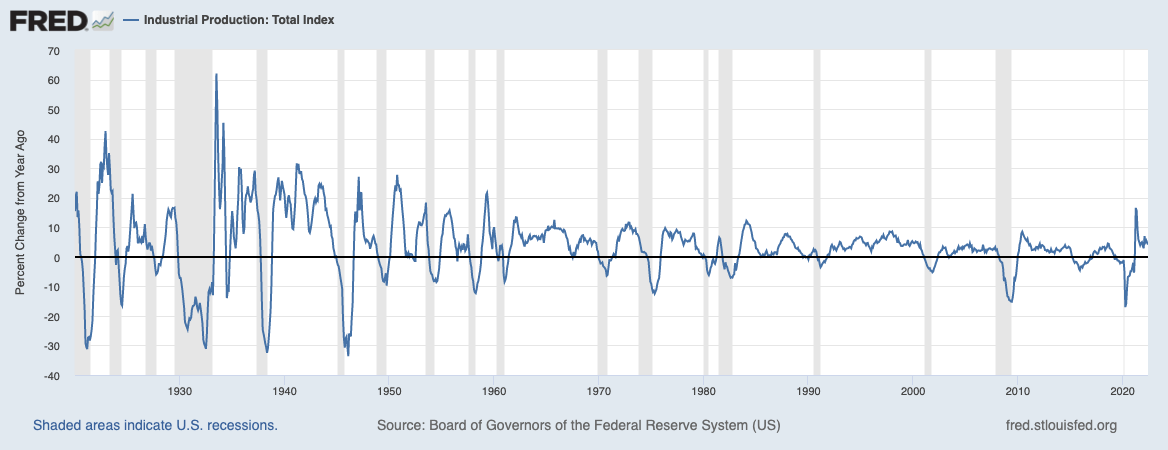

For example, industrial production (this is an industrial-focused article after all) is showing gradual declines and steep increases – even outside of “official” recessions like the decline in 2015.

St. Louis Federal Reserve

Business cycles are always unique as economies, geopolitical relationships, and technologies change. However, they are always triggered by something.

In the current environment, we’re dealing with an extremely tricky business environment. While it doesn’t mean much, it’s the most challenging macro environment I’ve witnessed in my rather short career in the industry.

We’re dealing with a mix of related issues like (but not limited to):

Supply chain issues in almost every single industry

An energy crisis (it’s worse in Europe than in the US)

Geopolitical tensions in Ukraine and to a lesser extent in Asia

High inflation

Low consumer sentiment

An aggressive Federal Reserve, which is determined to suppress inflation

This is a toxic mix for a number of reasons. One reason is the fact that the Fed is slowing into economic weakness. And as central banks cannot solve supply chain problems, they can only impact the demand side of the equation. Hence, killing inflation by force.

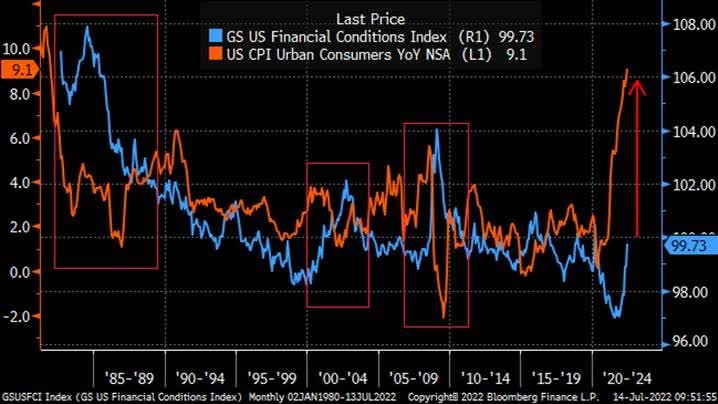

As my friend and colleague Nick Glinsman wrote in a recent article:

[…] the FOMC assumes that it will be necessary to slow demand before inflation will peak and begin to slow decisively. Several policymakers, including Chair Powell, have said that demand needs to slow before inflation can be brought to heel, and related to my favourite chart (below), since inflation is far above the target, it may take considerable slowing to get inflation anywhere near the 2% target.

Bloomberg

Due to elevated uncertainty about current inflation dynamics, the FOMC is focused on actual inflation outcomes, rather than leading inflation indicators to judge when inflation peaks. The policy response is backward-looking and somewhat best efforts. As such, the reliance on strictly backward-looking signals raises the odds the FOMC tightens more than strictly necessary to achieve the medium-term inflation target.

Right now, the market believes that the odds are higher than 75% that the Fed funds rate will exceed 350 basis points after the February 1 Fed meeting in 2023. The current fund rate (range) is 150 to 175 basis points.

In other words, a lot has been priced in and it’s hurting the economy.

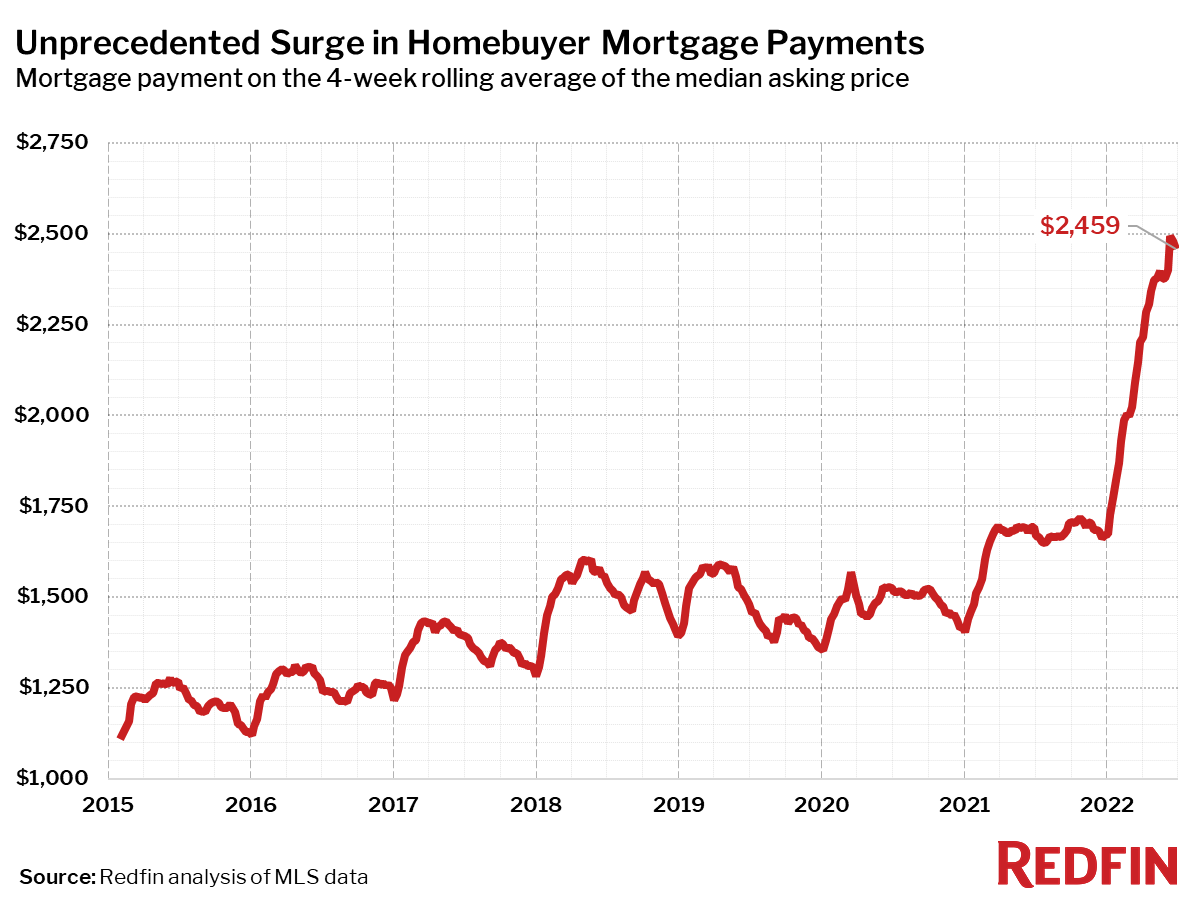

In a recent article, I highlighted the first cracks in the housing market. Homebuyers are now paying close to $2,500 per month to service their mortgage. This is up from roughly $1,500 prior to the pandemic.

Redfin

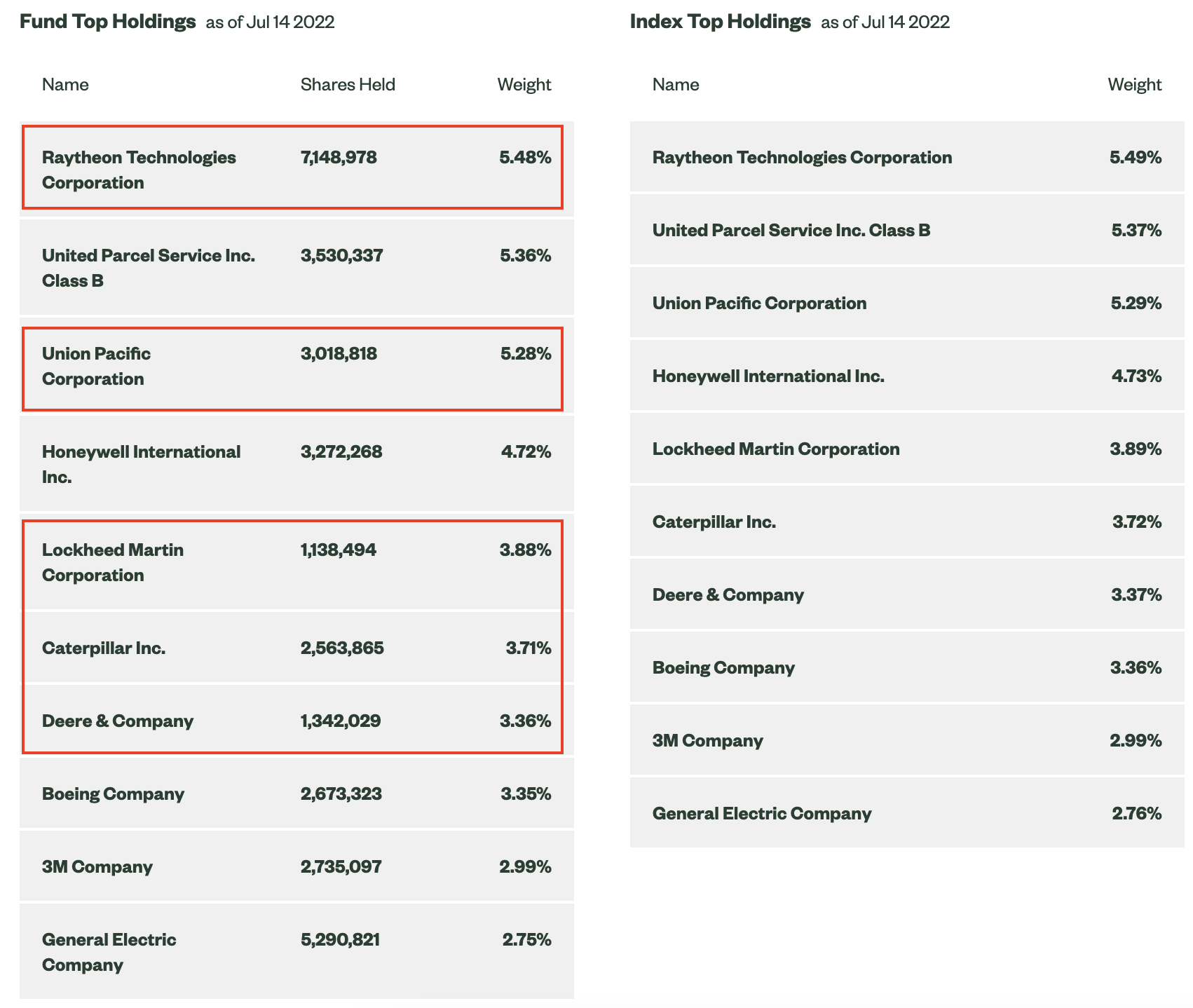

I’m highlighting housing because the industrial segment covers everything that has to do with the manufacturing and production of various goods and services. For example, the XLI ETF perfectly copies the S&P 500 industrial Index as the overview below shows.

State Street (SPDR)

The ETF/Index covers aerospace, which is a huge industry despite the dominance of just a handful of plane manufacturers as it incorporates a wide range of suppliers. The ETF also includes machinery, road and rail transportation, air freight, electric equipment, professional services, as well as huge industrial conglomerates that engage in almost every aspect of the already broad industrial supply chain.

Despite higher rates and growth fears, industrials aren’t doing poorly at all. In May, industrial new orders excluding defense and aircraft were 10% higher on a year-on-year basis. In June, industrial production was roughly 4% higher. Both are solid numbers.

St. Louis Federal Reserve

The problem is that a lot of this is pent-up demand. Cars couldn’t be produced during the past 2 years due to semiconductor problems (this is still an issue), companies lacked supplies from overseas, and various global lockdowns prevented things from getting back to normal the way a lot of people envisioned.

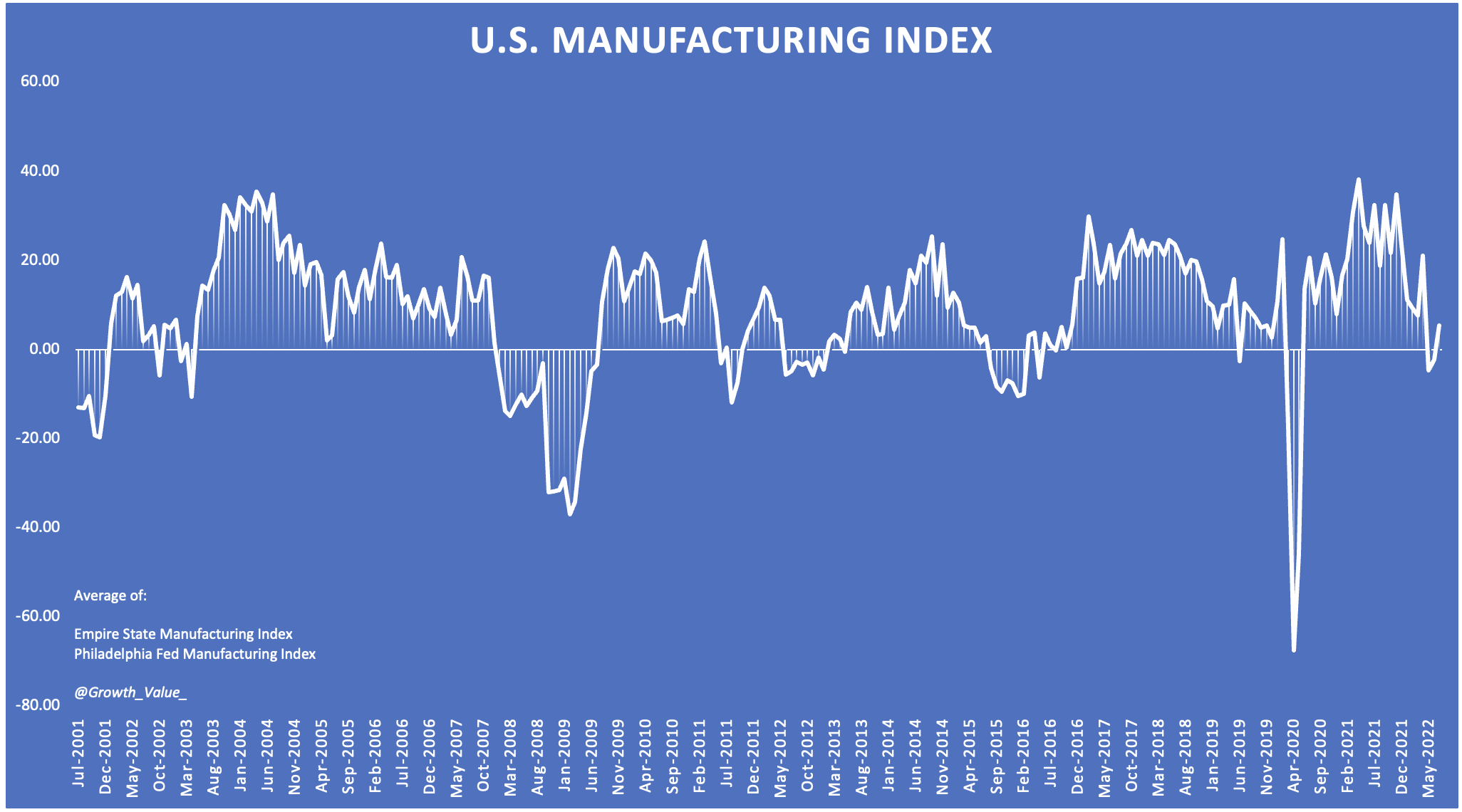

When using forward-looking indicators, we see that a lot of bad news is expected. Regional manufacturing surveys have been in a steep downtrend since the second half of 2021. They entered contraction territory in 2Q22. Now it’s looking like July is an improvement, yet I’m still waiting for Philadelphia Fed data, so don’t put too much weight on the July rebound.

Author

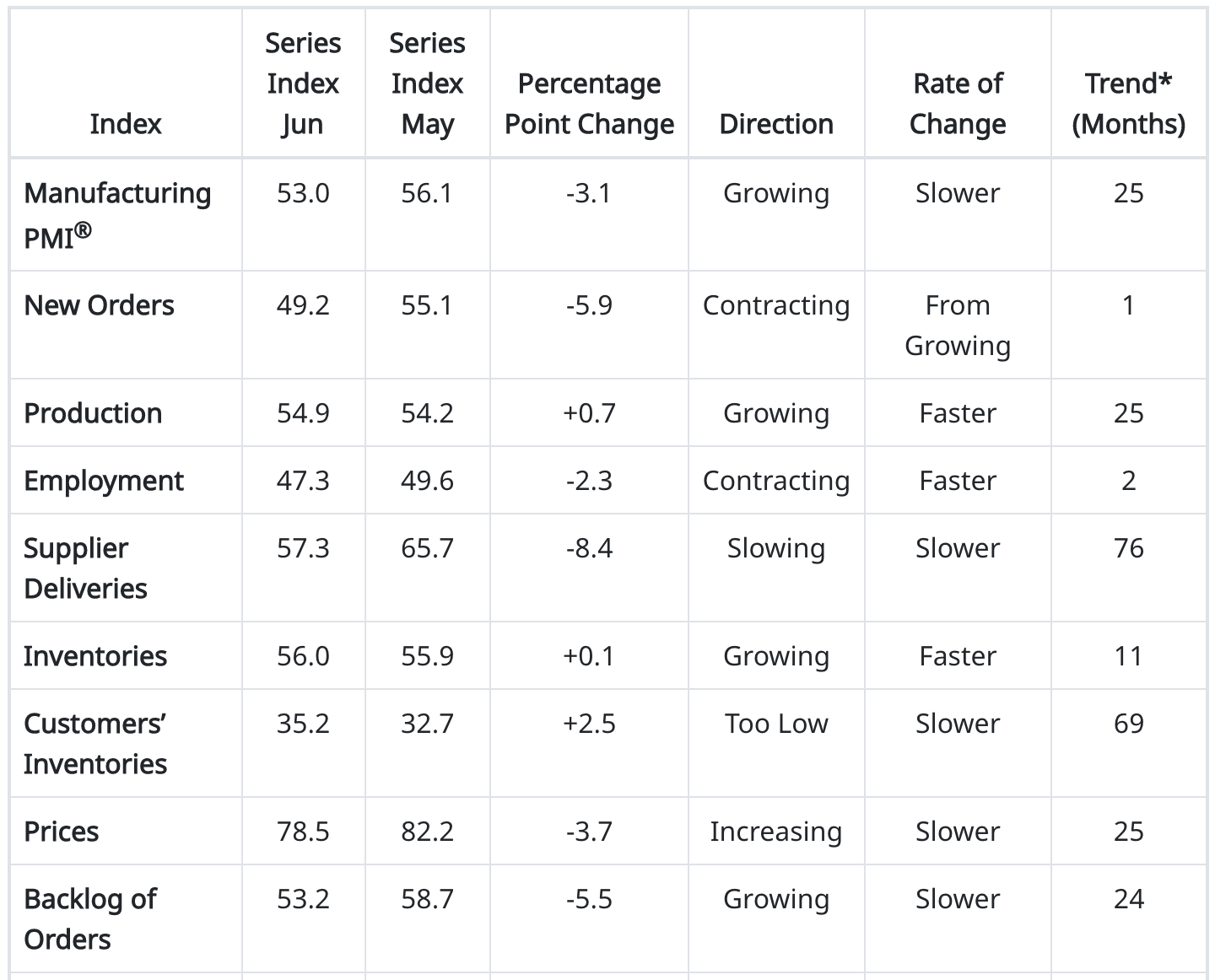

The official ISM manufacturing report for the month of June confirms the trend in the chart above. While the manufacturing PMI remained in expansion territory (above 50), it dropped by 3.1 points. New orders dropped into contraction territory with a decline of 5.9 points. Employment also turned negative.

Institute for Supply Management

It also doesn’t help that a lot of commodities remain in short supply. The following commodities saw shortages according to the ISM. The number indicates the number of consecutive months the commodity is in short supply.

Electric Motors

Electrical Components (21)

Electronic Components (19)

Hydraulic Components (2)

Labor — Temporary (14)

Packaging Products (2)

Paper (3)

Plastic Resins (2)

Rubber-Based Products

Semiconductors (19)

Steel — Fabricated & Machined Components (2)

Steel — Stainless; and Steel Products (3)

Hence, the report included the following comments (among others):

“Our suppliers are experiencing a softening of orders. We are still running at the same high level we did throughout 2021 and in early 2022.” [Machinery]

“Orders and production continue to be strong, but material availability is holding us back. Cannot run enough hours to eat into the backlog.” [Electrical Equipment, Appliances & Components]

The Risk/Reward

With that being said, I have added to my portfolio, which includes industrials. The other day, I wrote an article, which covered my purchase of additional Norfolk Southern (NSC) shares, a freight railroad (industrial company).

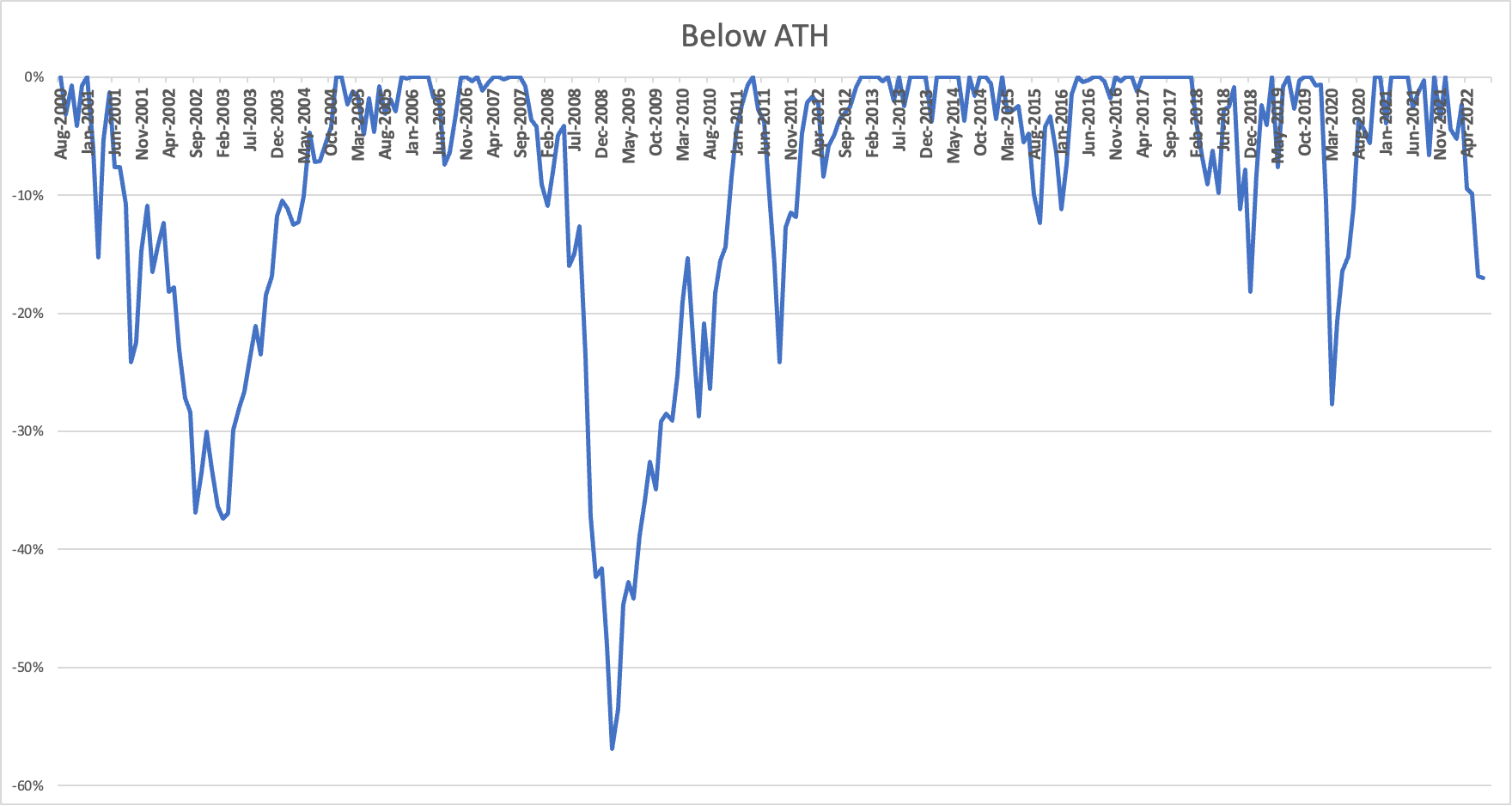

The reason I’m bringing this up is that the risk/reward has improved. The chart below displays the year-on-year performance of the XLI ETF. For the month of August, I used the total drawdown from its all-time high.

As one can see, industrial stocks have perfectly followed business expectations lower. On a monthly closing price basis, we’re now in a sell-off comparable to the one in 2015.

Author

When looking at the total drop from the all-time high, we’re also in a situation comparable to 2018.

Author

This is fantastic news for the risk/reward and it caused me to buy more industrial stocks for my long-term portfolio.

This does not at all mean that the bottom is in, but as I said, the risk/reward is simply more attractive at this point. Investors know that the Fed is in a tricky spot, hence Fed rate hike expectations are so high. Moreover, housing weakness has been priced in, to a very large extent as homebuilders are currently down 31% – using the iShares U.S. Home Construction ETF (ITB) as a proxy.

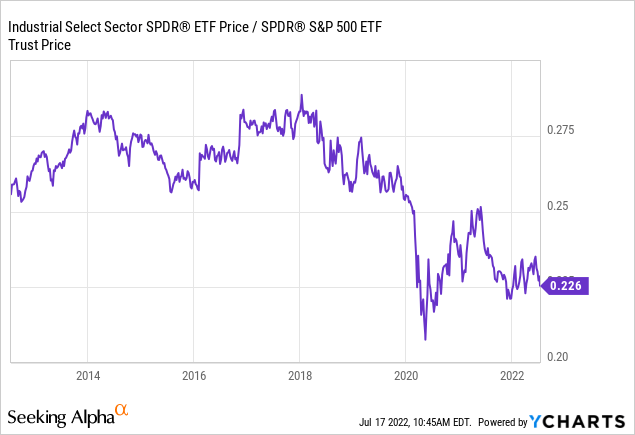

Meanwhile, industrial stocks have not underperformed the S&P 500 during the most recent downturn. The bad news is that underperformance is still significant since the highs in 2018. In 2018, global growth slowing put pressure on industrials. Then, the 2020 pandemic made things even worse. So far, the XLI/SPY ratio was unable to retake lost ground, which I believe is a result of ongoing aerospace weakness and supply chain problems that prevent a lot of industrial companies from turning demand into actual finished products.

I believe that the next upswing in economic expectations will allow industrials to outperform the market in a meaningful way. If we’re “lucky” the next upswing will be free of any COVID headlines and without supply chain problems that cause investors to ignore industrial companies.

With that said, there’s some info I need to add here.

What’s XLI?

I already discussed it a bit, but this ETF is one easy way to buy the “entire” industrial sector as it copies the S&P 500 industrial sector.

Established in 1998, this ETF has become the largest industrial ETF with an expense rate of 0.10% per year, which is very decent. Please note that you’re not directly paying this, it is automatically priced into the ETF.

XLI has total assets under management volume of $11.8 billion.

None of its 72% holdings have more than 5.5% exposure with the top three all weighing between 5.2% and 5.5%. In the table below, I highlighted the stocks that I own in my long-term portfolio.

State Street (SPDR)

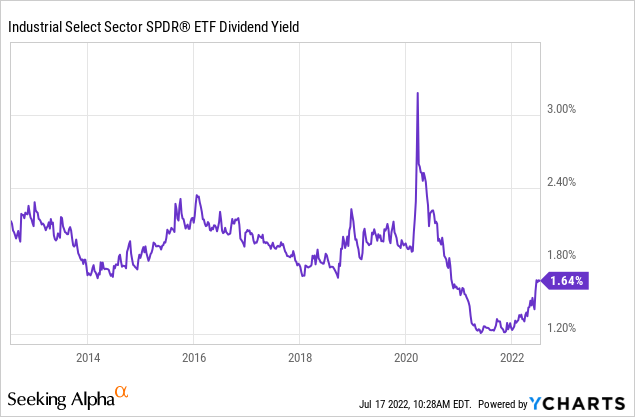

With that said, XLI is also yielding 1.7%, which is a nice bonus for investors.

However, the yield remains less than average (on a 10-year basis), and dividend-focused ETF investors are better off buying diversified dividend (growth) ETFs in my opinion. For example, this one.

Takeaway

Industrial stocks are in a tough spot. The market has priced in a manufacturing recession as a mix of toxic macro-economic and geopolitical developments put an end to the post-pandemic recovery.

Leading indicators show that demand is weakening, causing investors to de-risk their portfolios by selling cyclical assets. Hence, industrials continue to be unable to beat the market.

Yet, I am buying industrials for my long-term portfolio. While it’s hard to call for a bottom, I do like the risk/reward. The sell-off has priced in a lot of weakness (the upcoming earnings season for industrials will reveal a lot of news), pushed up dividend yields, and lowered valuations for a lot of companies.

For people who want to avoid stock picking, the XLI ETF offers opportunities. It’s the largest industrial ETF tracking the S&P 500 industrial sector. This well-diversified fund has a low expense ratio of 0.10%, and some of my favorite holdings in its top 10.

I believe that if growth expectations are bottoming indeed, we’re looking at a tremendous risk/reward for a lot of stocks in the industry (for this ETF as well) and outperformance over the S&P 500 as supply chain problems slowly fade.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment