John Sommer/E+ via Getty Images

IES Holdings, Inc. (NASDAQ:IESC) expects to benefit from both the increasing demand for data storage and future population growth thanks to a variety of business segments. Even considering potential competition from large players in the communication industry or the electrical installations sector, in my view, future guidance and expected free cash flow make IES Holdings undervalued.

IESC’s Business Model Is Well Diversified, Which Will Likely Offer Revenue Stability

Founded more than 60 years ago, IES Holdings is currently a company dedicated to the design and installation of electrical systems and technologies for a wide variety of end customers, including information centers, residential homes, shopping centers, and industrial establishments.

I believe that the company’s operations are well diversified, and target a variety of markets, which will likely lead to a more stable revenue. IES Holdings’ business model is divided into four segments, which cover all of its operations, from electrical installations to communication systems. These four segments are communications, residential, infrastructure solutions, and commercial and industrial.

The communications segment is currently working throughout the United States, facilitating its clients with the development, design, installation, and management of communication infrastructure, including data centers for both large corporations and smaller businesses.

The residential segment is intended for families and family complexes, which also offers the design and installation of electrical systems, including air conditioning, heating, ventilation, and plumbing services in some regional markets.

Infrastructure solutions, which is the segment that offers the lowest percentage of profit, consists of mainly electromechanical services for industrial establishments as well as appliance repair and customization of services engineering for these establishments and some information centers.

Ultimately, the commercial and industrial operations segment gathers the attributes of the previously named segments, offering design, construction, installation, and management services for commercial and industrial markets throughout the country, such as power generation markets and data centers.

Beneficial Guidance For The Long Term And Market Expectations Include A Median Sales Growth Of 22% And EBITDA Margin Close To 4%

Among the comments made by management in its most recent annual report, in my view, the most relevant were the words about future long-term demand. IESC believes that population growth, aging public infrastructure, and demand for data storage will likely serve as catalyst for revenue generation.

Over the long term, we believe that there are numerous factors that could positively drive demand and affect growth within the industries in which we operate, including population growth, which will increase the need for commercial and residential facilities, aging public infrastructure, which must be replaced or repaired, an increasing demand for data storage, and increased emphasis on environmental and energy efficiency, which may lead to increased public and private spending. Source: 10-k

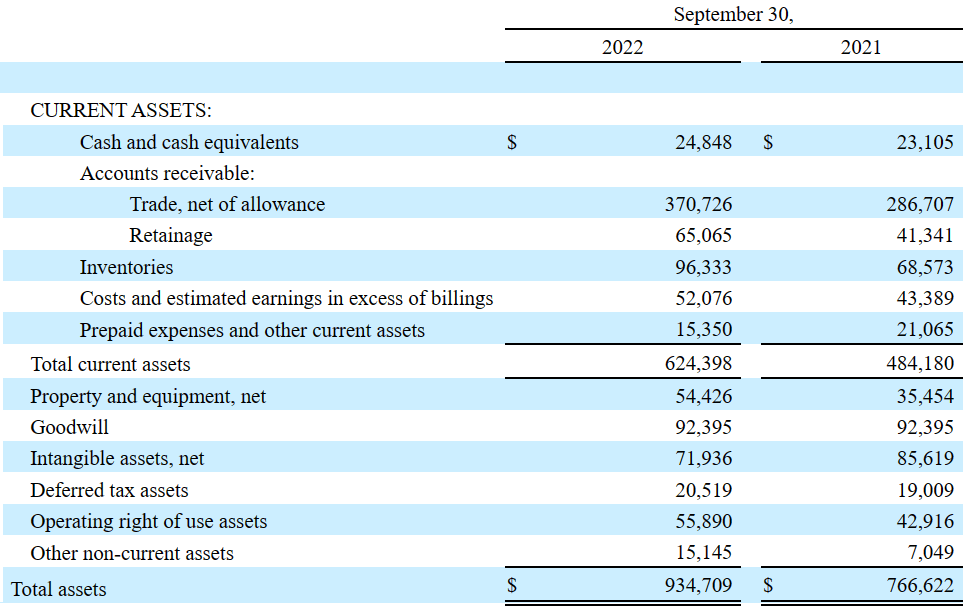

Considering the company’s business model, I believe that IESC’s future financial figures will likely not be far from the numbers reported in the last four years. In 2022, revenue was equal to $2.167 billion, net sales growth was equal to 41%, and 2022 EBITDA margin stood at 3.7%. 2022 EBITDA was close to $81.7 million with an operating profit of $56.2 million together with an operating margin of 2.59%. Finally, pre tax profit stood at $53 million with net income of $34.8 million.

Source: marketscreener.com

Healthy Balance Sheet

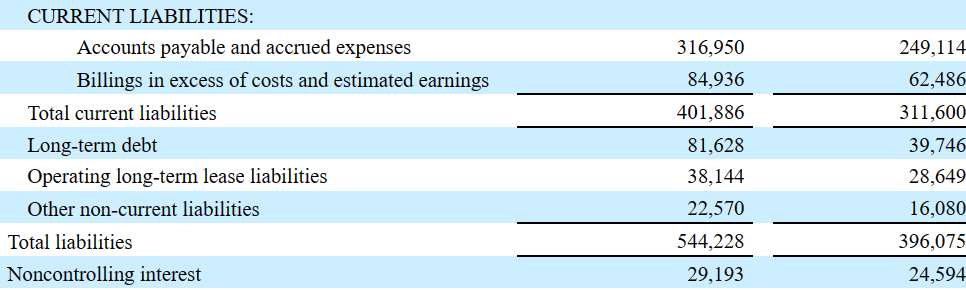

As of September 2022, the company reported cash worth $24.848 million. In addition to accounts receivable worth $370.726 million, inventories stand at $96.333 million, with cost and estimated earnings of $52.076 million and prepaid expense close to $15.350 million. Finally, total current assets are equal to $624.398 million. The ratio current assets/current liabilities stands at more than 1x, so I would say that IESC does not report a liquidity issue.

Management reported property and equipment of $54.426 million with goodwill worth $92.395 million, intangible assets of $71 million, and tax-deferred assets of $20 million. Besides, operating right of use assets were worth $55.890 million accompanied by other non-current assets of $15.145 million. Finally, total assets stand at $934.709 million, close to 2x the total amount of liabilities.

Source: 10-Q

IESC’s liabilities include accounts payable worth $316 million with a billing in excess of cost and estimated earnings of $84.936 million. Besides, total current liabilities are equal to $401.886 million. The company’s long-term debts stand at $81.628 million with operating long term lease liabilities worth $38.144 million. Finally, total liabilities stand at $544.228 million with a non controlling interest of $29.193 million.

Source: 10-Q

Successful Expansion Of Offering Of Plumbing and HVAC services Would Result In A Valuation Of $111 Per Share

Under my base case scenario, I assumed that IESC’s current strategy would be successful. Future demand will likely provide a strong and consistent flow of capital. Besides, management will be able to maintain a stable position with a large presence in the market as well as low-cost services in relation to its competitors.

I also assumed that management will successfully develop new products, which will not run the risk of becoming obsolete in the near future. More in particular, I assumed that the expansion of the company’s offerings of plumbing and HVAC services will bring economies of scale and free cash flow generation. The company offered more information in this regard in a recent annual report.

Our long-term strategy is to continue to be a leading provider of electrical services to the residential market, and to continue to expand our offerings of plumbing and HVAC services. The key elements of our long-term strategy include a continued focus on maintaining a low and variable cost structure and cash generation, allowing us to effectively scale according to the housing cycle, and to opportunistically increase our market share. Source: 10-k

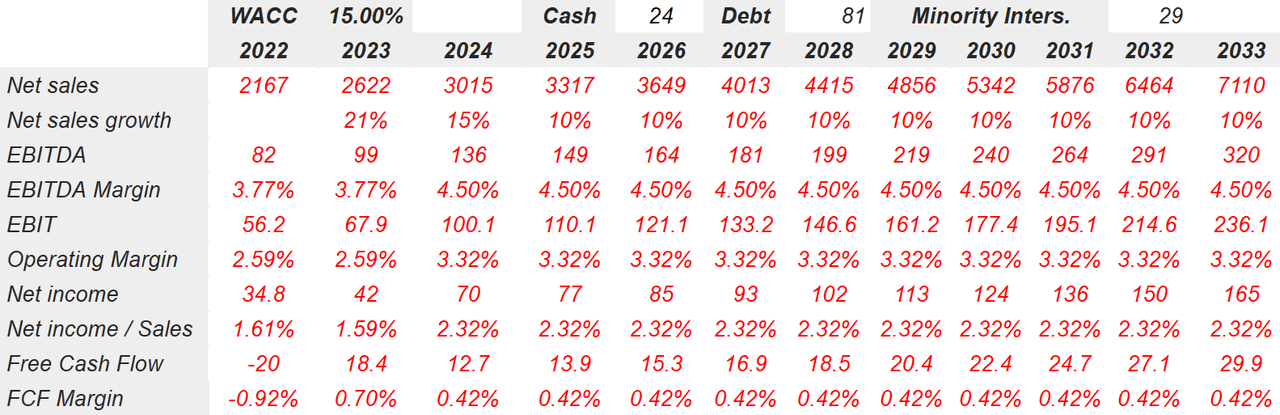

With the previous conditions, I included 2033 net sales of $11.677 million together with a growth of 11% in net sales. Besides, I also assumed 2033 EBITDA of $571 million together with an EBITDA margin of 4.89%, 2033 EBIT of $433.2 million, and net income of $316 million.

If we also assume a discount of 9.7% and 2033 free cash flow close to $94.6 million, and include a FCF margin of 0.81%, the net present value of free cash flow would stand at $299.2 million.

Source: Malak’s DCF Model

Besides, with an EV/EBITDA of 9.7x, which I believe is quite conservative, a terminal value of $5.53 billion is expected with a NPV of terminal value of $2 billion. My results also included equity of $2.32 billion, a fair price of $111 per share, and an IRR of 6.50%.

Source: Malak’s DCF Model

Competition In The Communication Services Segment And The Industrial Solutions Segment Would Imply A Valuation Of $28 Per Share

First of all, I would highlight that as far as the residential services segment is concerned, competitors are mostly small contractors that have limited access to the market and capital. They also do not have a long history of relationship with consumers and long-term labor relations as it is in IES Holding. This is undoubtedly an advantage in positioning in this regard. At the other extreme, we find the commercial and industrial services market, which, although it has a limited amount of access at the national level due to the necessary infrastructure and commercial relations and experience in the field, is the segment in which IES Holding has greater competition due to the very nature of this market. In addition, it does not compete with small contractors but with companies of a similar size and a growth plan in a similar phase to that of the company.

Regarding the communication services segment, competition is established with small providers at a regional and national level as well as companies with a national position and access to the flow of capital that allows them to scale their positions.

Lastly, regarding its competitors in the industrial solutions segment, IES Holdings also operates in a highly competitive market occupied by small providers as well as large corporations. In this case, IES details that its differential, in addition to the credibility of its products and the track record in this regard, lies in the possibility of developing high-tech products as well as the design of these customized ones in relation to their clients. Due to the large number of particularities that exist in this type of market, IES competes with companies that can provide a comprehensive service as well as small companies that have developed their business in the provision of a single specific product or service.

Besides, we will comment on the risks to which IES is exposed both commercially and financially. Mainly, it happens that the services that IES provides are subject to economic variability and in many cases the accessibility of certain segments of the population to contracting these services, especially if we remember that the segment of residential services is the one that facilitates the greatest income.

We can also add that the jobs of its employees, in many cases, are prone to accidents. In this case, IES declares that it does not have a most adequate coverage service. Any conflict in this regard would affect the positioning of the company and its credibility. Brand damage may lower revenue growth expectations, which would push the company’s fair valuation down.

In my view, the services that the company offers as well as a large portion of its commercial clients don’t seem currently oriented towards the reduction of environmental damage, nor do they seem to have projected compliance with global business trends in relation to the reduction of emissions or improvements in waste management. In this sense, any change in regional or national regulation as well as the possibility of legal requirements for commercial activities could affect and force IES to urgently rearrange its business segments and active operations.

Finally, let’s point out that IESC noted that 2023 could include a revenue growth decline because of the company’s single-family housing business. Under this case scenario, I assumed that reality would be a bit worse than what the company expects.

Based on current trends in demand for housing heading into fiscal 2023, we expect that a revenue decline in our single-family housing business, where we typically do not enter into long-term contracts, will offset, or more than offset, revenue growth from our multi-family housing and other backlog-driven businesses during the year. Source: 10-k

Under the previous dramatic assumptions, I included 2033 net sales of $7.110 billion with 2033 net sales growth of 10%. 2033 EBITDA would stand at $320 million along with a 2033 EBITDA margin of 4.50%. Besides, 2033 EBIT would stand at $236.1 million with an operating margin of 3.32%. The net income would stand at $165 million together with a net income / sales of 2.32%. Finally, I anticipate free cash flow of $29.9 million coupled with a FCF margin of 0.42%.

Source: Malak’s DCF Model

With the previous figures, the NPV of FCF would stand at $95 million, with a terminal value of $2.4 billion and a NPV of terminal value of $515.8 million. If we sum the terminal value and the discounted FCF, the enterprise value stands at $640 million with equity of $583 million, a fair price of $28 per share, and an IRR of -3.66%.

Source: Malak’s DCF Model

Conclusion

IES Holdings offers a diversified business model with a number of business segments targeting a wide variety of end customers. Besides, I believe that the residential segment will likely benefit from future population growth, and the communications segment may benefit from the growing demand for data storage. Yes, there are risks from diminishing demand in 2023, however considering the company’s long-term guidance, in my view, the company appears undervalued. Under normal conditions, I believe that IESC is worth $111 per share.

Be the first to comment