Kameleon007

Yesterday was a mixed bag for the major market averages. Goldman Sachs fell short of expectations, due to its reliance on investment banking, while Travelers warned of lower profits because of severe winter storms. That combo walloped the Dow Jones Industrials for nearly 400 points, but a decline in interest rates nudged the Nasdaq Composite to its seventh winning day in a row. After the close, United Airlines beat estimates and raised guidance significantly for the first quarter, leading to an after-hours rally in airline stocks. I think yesterday was a microcosm of what we will see this earnings season, which is a fairly even mix of winners and losers, but the focus will gradually shift to the next Fed meeting, which looms large two weeks from today.

Finviz

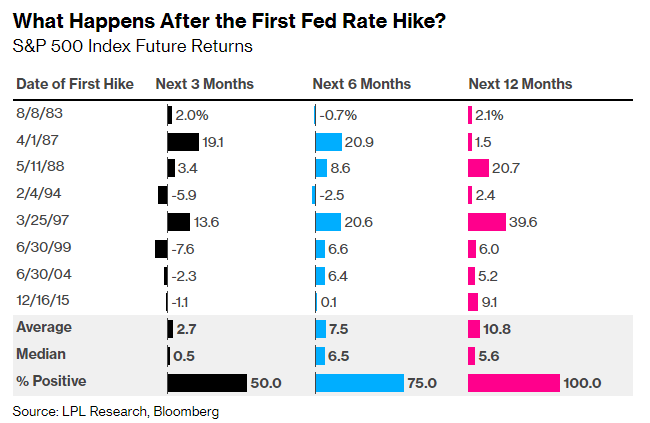

I can’t count how many times over the past three months that I have heard the old adage, “Don’t fight the Fed.” It had a lot more meaning when the Fed started raising rates last March, because the stock market does not have a great track record in the 3-month period following an initial interest-rate increase, as can be seen below. Yet the S&P 500 has been higher one year after the first rate hike 100% of the time if we look at the past eight rate-hike cycles. Can we make it nine? The index stood at 4,288 when the Fed first raised rates on March 16, 2022, so it is a distinct possibility.

Bloomberg

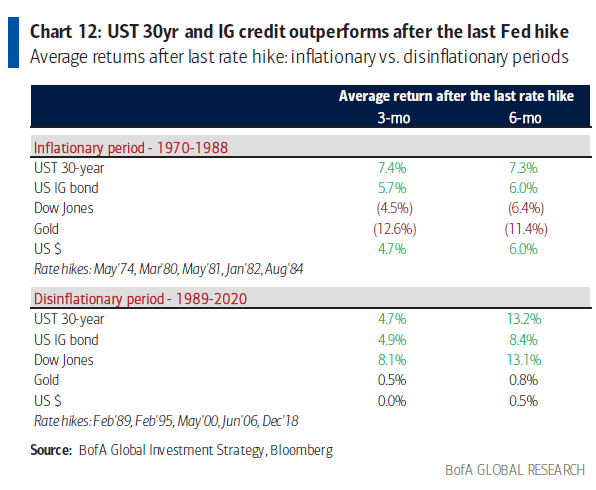

I am more interested in what happens after the rate-hike cycle ends, because it is pretty obvious that we will see that last rate hike in either February or March of this year. If you want to call investing in risk assets at this juncture “fighting the Fed,” then I am fighting the Fed with some powerful statistics as my tailwind. The critical divide is whether we are in an inflationary or disinflationary period moving forward, which some may view as still debatable, but I do not. Disinflation is defined as a period when the rate of inflation decelerates, and it has clearly decelerated from June of last year. That should continue through the remainder of this year, based on both the Consumer Price Index and Personal Consumption Expenditures price index.

Bloomberg

Market returns during disinflationary periods following the last rate hike over the past 40-plus years have been bullish for stocks and bonds. That was not the case during the inflationary period from 1970-1988. As if this wasn’t enough reason to fight the Fed, my conviction was emboldened by an extraordinarily rare and powerful technical development in the market that occurred last Thursday.

In yesterday’s Morning Brief, I discussed the recent outperformance of the equal-weighted S&P 500 and Russell 2000 index with the point being that the average stock has been doing a whole lot better than the large-cap weighted indexes. In other words, breadth has been improving, as more stocks are advancing than declining. I did not realize how powerful this move has been until learning that Breakaway Momentum had been achieved.

Walter Deemer is an esteemed technician who has been working at his craft since the 1960s and constructed this indicator. It measures points in time when the ratio of advancing to declining stocks on the NYSE exceeds 1.97 over a ten-day period. It has only occurred 24 times since 1945, and last week’s buy signal makes it 25. The forward returns after achieving a Breakaway Momentum buy signal speak for themselves. The S&P 500 has been higher 96% of the time in the 6- and 12-month periods that followed the buy signal.

TheStreet

Now we have the bullish precedent of market performance following the last rate hike in a disinflationary environment combined with an extremely rare Breakaway Momentum buy signal. I am growing less concerned about the Fed by the day, but that is not the case for the consensus on Wall Street, which should be the source of fuel for higher prices. According to the latest survey by Bank of America, fund managers have not been this pessimistic on stocks in 17 years, which can be seen in the degree to which they are collectively underweight US equities. Bull markets are born out of extreme skepticism, as the average stock starts to rise inexplicably, climbing the proverbial “wall of worry.” That is what I see happening today.

SeekingAlpha

Be the first to comment