Pavel_Chag/iStock via Getty Images

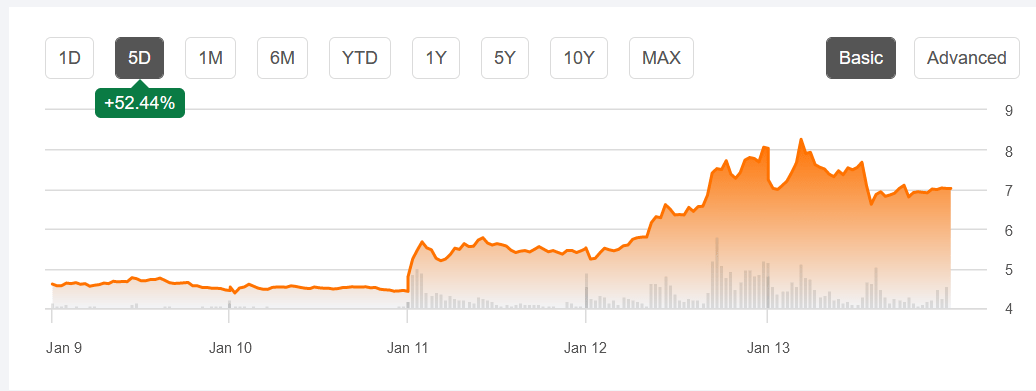

Carvana’s (NYSE:CVNA) stock price has jumped over 50% in a week without any improvement in fundamentals or positive news being released. The run-up appears to be from hype around stocks with high short interest, which also lifted BBBY last week. Once the hype has passed, we expect CVNA to reverse course and fall back to previous lows, as we don’t see a turnaround in the near term.

Seeking Alpha

The Journey So Far

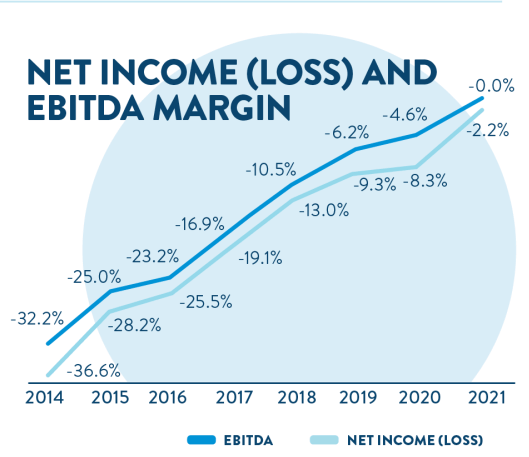

Carvana has never turned a profit, as shown in their own investor presentation below. The closest they came was in 2021, when EBITDA came in at 0% of sales and the company had a net loss of 2.2% of sales.

Carvana

Source: Carvana

EBITDA has since reversed course and was -13.5% of sales for the first 9 months of 2022, while net income came down to -7.5% of sales over the same time period. Carvana lost a whopping $1.5 billion in the first 9 months of 2022.

Carvana

Source: Carvana

Signaling Ahead

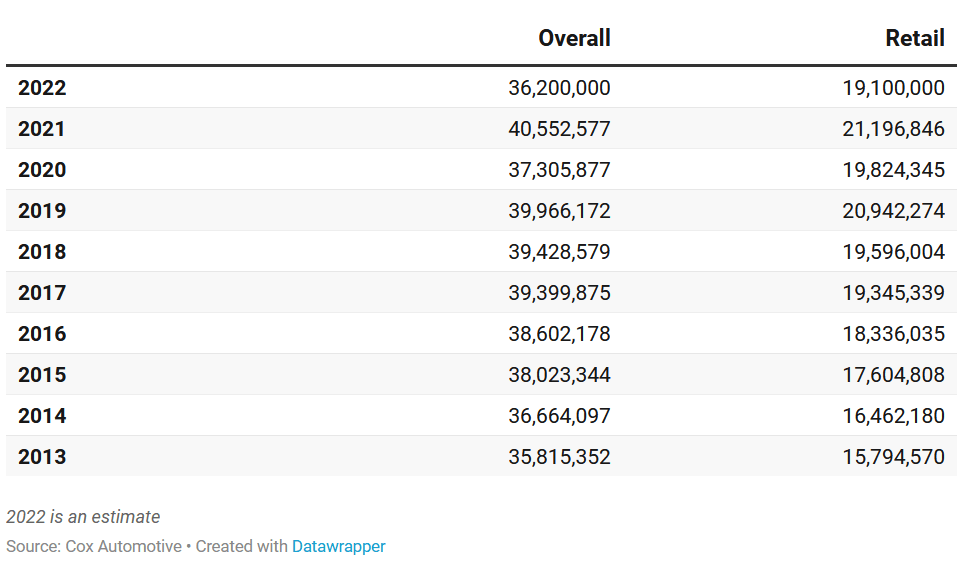

The table below shows the annual used car sales from 2013 to 2022. “Retail” sales represent the cars sold through dealers, which includes Carvana. Retail volumes fell almost 10% from 2021 to 2022, bringing sales volumes back to 2017 levels. Sales volumes are expected to remain lower as higher interest rates have impacted what consumers can afford.

Automotive News

Source: Automotive News

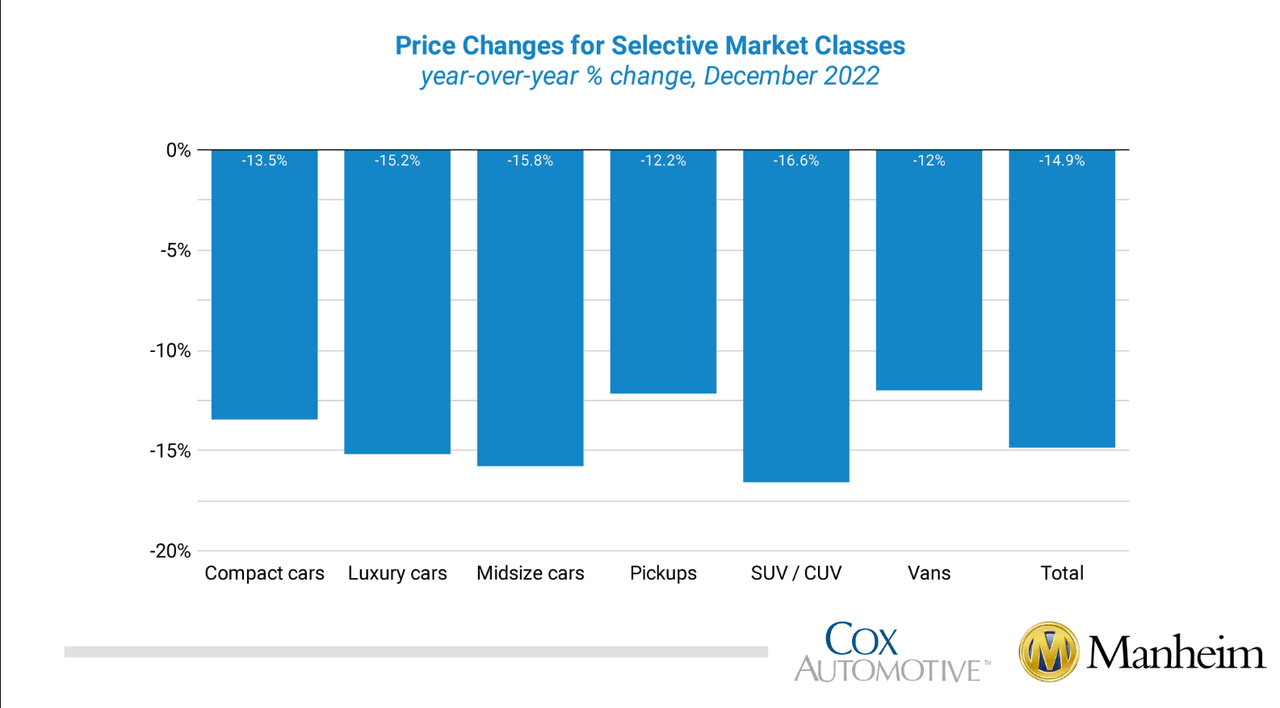

Used car prices have also dropped significantly since 2021. The chart below shows that as of December 2022, overall prices have declined by almost 15% year over year and that prices declined by at least 12% for all classes of vehicle. This trend is expected to continue as interest rates continue to increase and impact affordability. Falling used car demand and pricing do not bode well for Carvana, although Carvana has managed to stay ahead of industry trends as seen in their most recent Q3 2022 results, where they saw an increase in sales of 18.8%.

Manheim

Source: Manheim

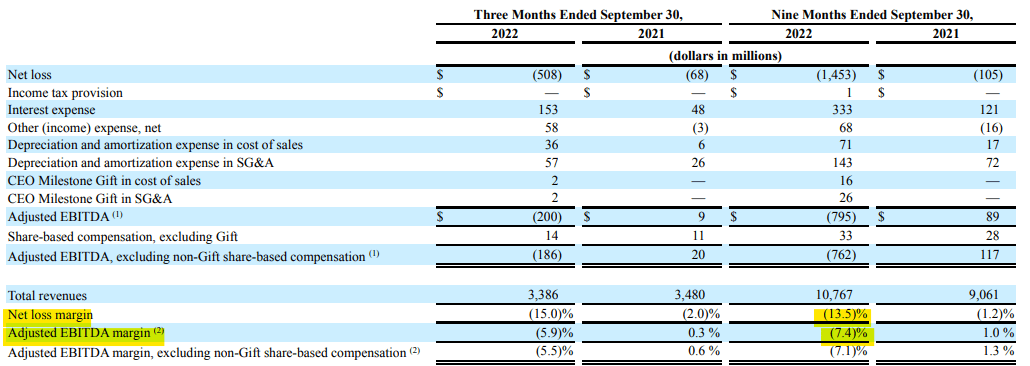

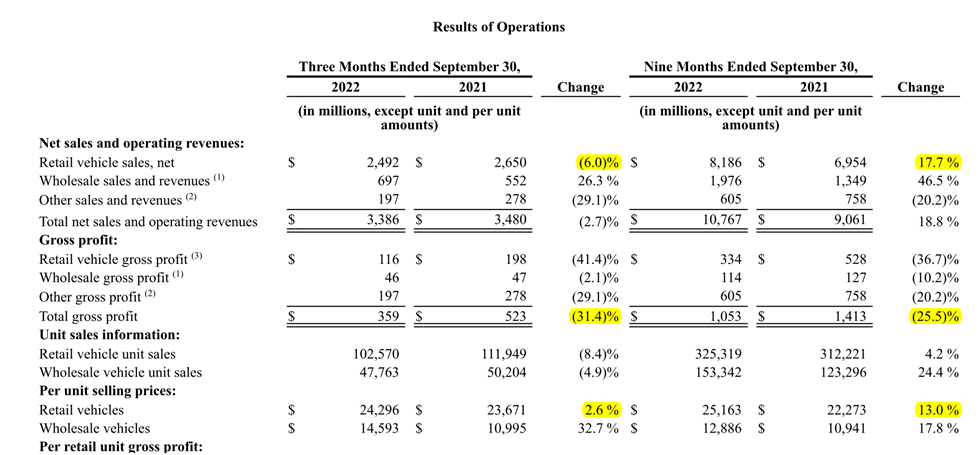

Despite managing to buck the industry trend, likely due to aggressive marketing, Carvana did not see an improvement in the bottom line. This is clear evidence of poor expense management and lack of control over costs. Against a 18% increase in net sales, Carvana saw a 25.5% decline in gross profit.

Carvana

Source: Q3 2022 Form 10Q

The Q3 2022 10k cites increased vehicle acquisition costs as the main driver of increased cost of goods sold. Carvana sources used vehicle inventory directly from customers and at used-car auction market. In both cases, Carvana relies on proprietary algorithms that evaluate vehicles available for purchase and determine an appropriate offer. This is in contrast to traditional in-person sourcing methods used by dealerships. This model does not appear to be working in the favor of Carvana as the reliance on the software has resulted in rising acquisition costs outpacing revenue.

Looking ahead to Q4, we can view the recent CarMax results as a sign of what to expect for Carvana. CarMax is the largest used car dealer in the United States and reported earnings on December 22, 2022. Although the business models are different – CarMax is more of a traditional car dealer with physical locations, CarMax earnings can be used to gauge how used car demand and pricing have impacted sales and profitability in more recent months.

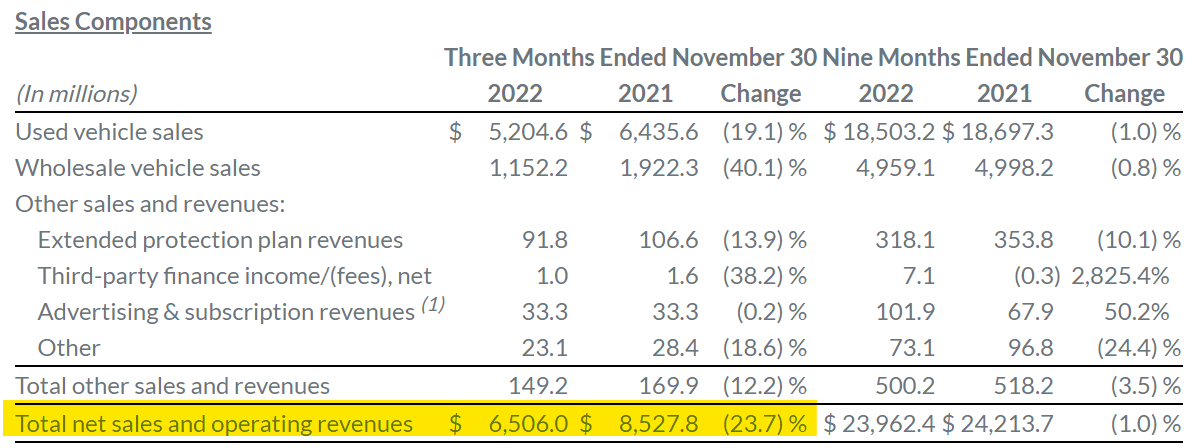

As we can see from the table below, CarMax sales dropped across the board in the latest quarter compared to the prior year – an overall decline of 23.7%. The company attributed lower sales to vehicle affordability challenges due to inflationary challenges, climbing interest rates, and low consumer confidence.

CarMax

Source: CarMax

As a result of declining sales, CarMax earnings dropped 86.1% year over year. Carvana reports their Q4 earnings at the end of February. Based on what we have seen for CarMax, we do not expect positive news from Carvana.

CarMax

Source: CarMax

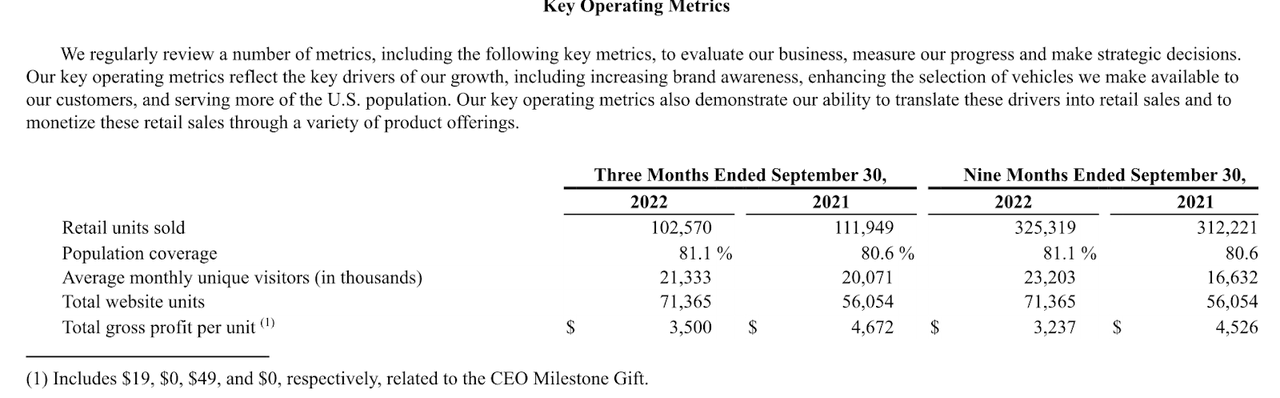

In the earnings call for Q3 2022, management targeted a gross profit per unit (“GPU”) of $4,000 to be profitable. Gross profit per unit is a key operating metric derived from total revenue divided by number of retail units. The gross profit per unit for the most recent quarter is $3,500. To cover Carvana’s total expenses and interest ($808 million for the most recent quarter), the company would need to drastically increase their GPU and units sold. At the management target of $4,000 GPU, Carvana needs to hit volumes of approximately 200,000 units. Both the GPU and volume required to turn a profit seems unattainable given their current business model and the industry headwinds discussed above.

In the Q3 earnings call, management admitted that fourth quarter GPU is expected to decrease even more relative to the third quarter as a result of the spread between retail and acquisition prices and increase in daily depreciation rates of vehicles. Based on these comments and the expected across the board decline in the used car industry, we do not expect positive developments in fourth quarter results. We believe the GPU and retail sales will continue to disappoint. If the stock price has not fallen to previous lows by then, the fourth quarter earnings will no doubt provide the reality check necessary to bring the valuation to more realistic levels.

Carvana

Source: Q3 2022 Form 10-Q

A Race Against Time

While we do not believe Carvana is at immediate risk of bankruptcy, given their access to short-term revolving facilities and unpledged inventory and real estate, tapping into their financing options will only result in increased interest expense and pressures on the bottom line.

Carvana is scrambling to stay afloat through cost cutting initiatives in a period of turbulence for the used car industry. Carvana is in a race to turn a profit before it runs out of funds, a race it is sure to lose.

Be the first to comment