JHVEPhoto

Investment Thesis

Many have posited that Goodyear Tire (NASDAQ:GT) is incredibly undervalued at present levels when pre-pandemic normalized earnings are taken into account. In addition, the recent Cooper Tire acquisition is set to contribute to the company’s earnings. However, when one takes into account the > $1.5 billion in debt incurred during the pandemic to undertake the Cooper Tire acquisition and to ensure liquidity needs were met, one may begin to question if the company’s already poor balance sheet can handle such additional debt. In addition, GT was in decline before the pandemic, with consecutively lower revenue, earnings, and FCF annually. Given these risks and the company’s current market capitalization, it is my opinion that Goodyear Tire is fairly valued at present levels.

Background

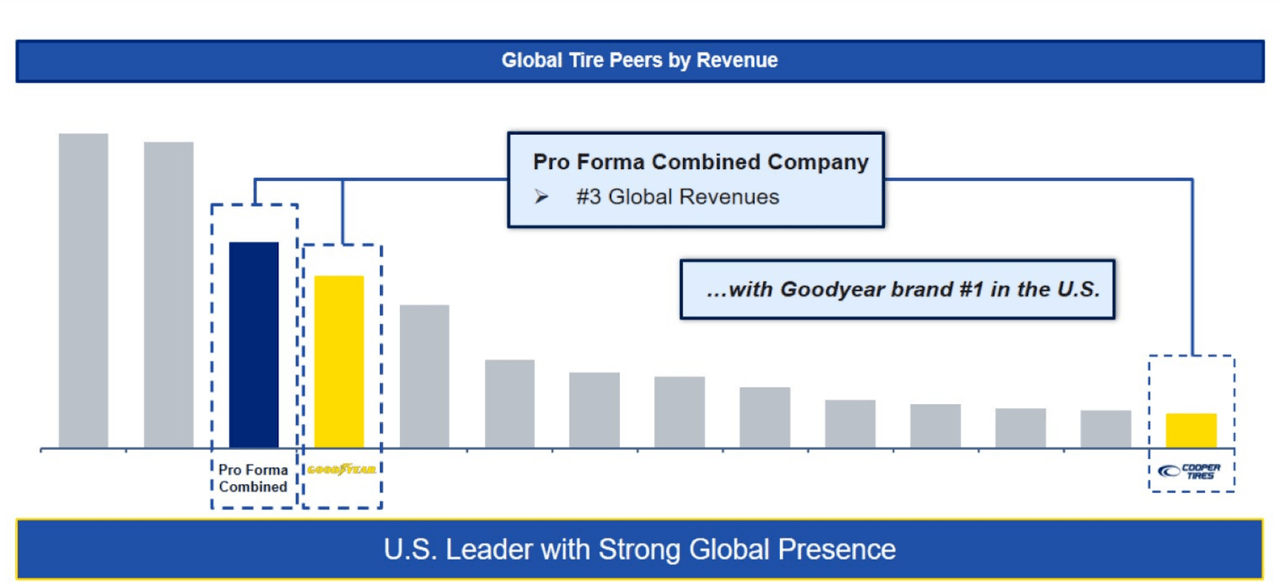

The Goodyear Tire & Rubber Company is an international leader in tire manufacturing, with operations in most regions around the world. Since the stock’s peak in 2017 at a share price of > $35, its stock has declined to around $12. The driver of these poor results has predominantly been poor operating performance. However, on June 7, 2021, GT acquired Cooper Tire (CTB) for an enterprise value of $2.5 billion. Combining GT and CTB revenues, the new company will produce $17.5 billion in revenue according to GT’s management. With the acquisition of Cooper Tires, GT will solidify its position as the third-largest tire manufacturer by revenue in the world. With the acquisition of Cooper and a rebound from the pandemic, the company’s earnings rebounded to $764 million and its revenue increased approximately 42% to $17.48 billion.

Prior to the acquisition of CTB and the coronavirus pandemic, GT’s revenue had been declining by 2.7% a year from 2016 to 2019. In addition, its earnings had declined from $1.26 billion in 2016 to a loss of $311 million in 2019. The pandemic exacerbated the company’s woes and the company posted a loss of $1.25 billion in 2020. However, FCF remained positive during the pandemic and even increased by 7%. The company’s normalized pre-pandemic FCF was incredibly volatile but averaged approximately $345 million.

Cooper Tire Acquisition

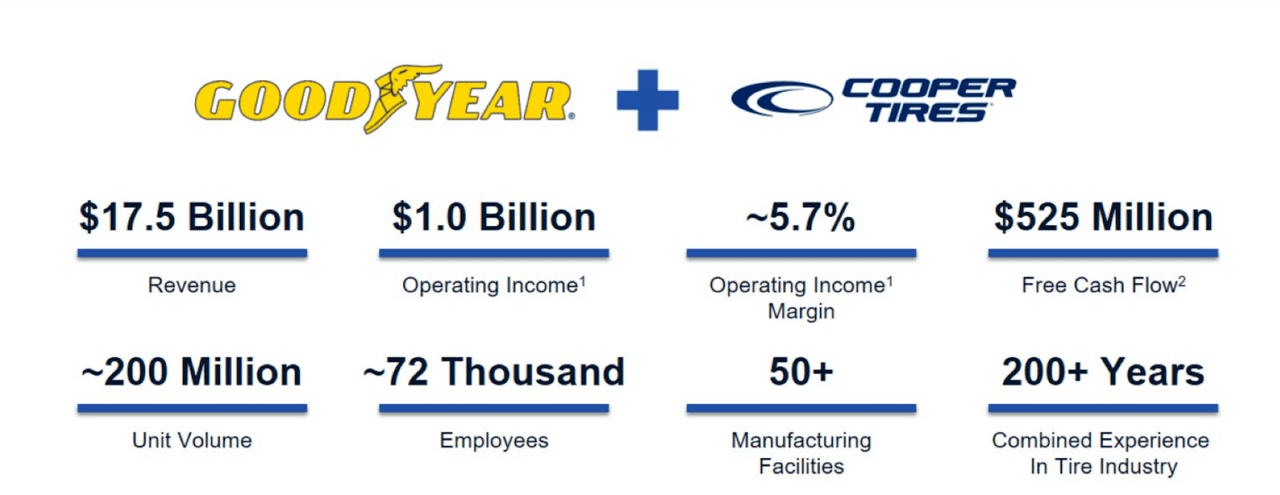

Prior to the acquisition, Goodyear was the third-largest tire company. After its acquisition of Cooper Tire, the world’s 13th largest tire company, it will solidify its position as the world’s third largest tire company. The combined company will have a total of $17.5 billion in revenue, $1 billion in operating income, and a 5.7% operating margin.

Global Tire Market Ranking by Revenue (Cooper Tire Acquisition Presentation)

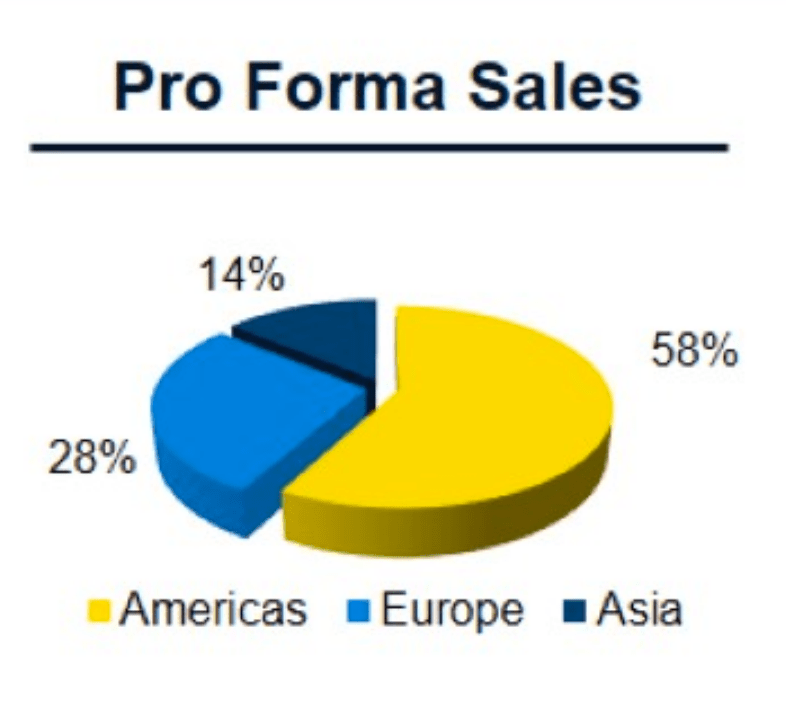

Cooper Tire is a leading tire company in North America in particular, being its fifth-largest manufacturer, but it also maintains a global presence. In fact, 18% of its sales occur in Europe and Asia, with the remaining 82% of revenue from the Americas. This is important as the US tire industry’s growth is much slower than emerging markets’ tire industries. Independent from GT, Cooper Tire has $2.8 billion in revenue and 10,000 employees.

Goodyear’s management claims its FCF is $437 million, although my estimation is $345 million, and Cooper’s FCF is approximately $88 million according to Goodyear management. By these estimates, the combined FCF of the two entities would be $525 million. Management estimates that the cost synergies from the acquisition will approximate $165 million, leaving the combined entity with $690 million in FCF per year. Using my conservative estimate of Goodyear’s present FCF, this figure would be $598 million. Therefore, even when the dilution of 46.06 million shares is taken into account, this acquisition was still immediately accretive to Goodyear’s shareholders and still leaves potential upside when future cost synergies are taken into account.

Pro Forma Company Highlights (Cooper Tire Acquisition Presentation)

Industry Prospects

The North American tire market shrunk in 2020 largely due to Covid. However, for 2021-2026, the North American tire market is expected to grow at a CAGR of 1.9% according to Orion Market Research. While this moderate growth may seem satisfactory for a company trading at a normalized FCF multiple (based on my estimates) of < 10, its revenue growth (excluding the acquisition of Cooper Tire) has been nonexistent. This revenue trajectory may revert itself or eventually stagnate, conservative investors cannot solely rely on mean reversion to anticipate future operating results. This is why it is crucial that Goodyear maintain and expand its sales internationally. The anticipated CAGR for the global tire market is 4.2%, making GT’s international operations poised for growth. Given that the sales from outside the Americas will constitute 42% of the combined entities’ revenue, it seems a reasonable assumption that as GT’s international sales continue to increase relative to its domestic revenue, revenue stabilization and potential growth may materialize. This would indubitably lead to multiple expansion for the beleaguered stock.

Pro Forma Post-Acquisition Sales (Cooper Tire Acquisition Presentation)

Balance Sheet

Prior to the Acquisition of Cooper Tire, GT’s balance sheet was already disconcerting for many investors. In 2020, GT held approximately $6.9 billion in debt, and by 2021, it had > $8.4 billion in debt, increasing its interest expense by around $63 million. This reduces its normalized pre-pandemic FCF to < $300 million. It should be noted that this reduces management’s projected post-acquisition FCF estimates of $650 million to $535 million. Given that, GT’s trailing twelve-month interest expense is $412 million. Furthermore, GT has already undertaken almost $1 billion in additional debt in the last 6 months, suggesting that interest expense could increase, and therefore, FCF could decrease further still. This leaves the most exuberant estimation of GT’s interest coverage ratio (using unlevered FCF) of 2.58. Using my projection of FCF and no change in interest expense, this ratio shrinks to 2.2. These ratios are not necessarily indicators of impending bankruptcy, for an already declining company, these ratios are not ideal. While one may counter this ratio is actually a sign of the company’s strength when EBITDA supplants FCF, such an argument is not applicable to a company such as GT with enormous maintenance capex.

Conclusion

With a maximum market CAGR of 4% internationally, it appears that management’s projections for operating results in general and FCF, in particular, can only be met by an expansion in market share. However, recent history does not bear out these projections, as Goodyear’s revenue has declined by 2.6% in the four years prior to the pandemic in a growing domestic and international tire market. If an investor were to base their valuation on management’s estimates, they may well be sorely disappointed. While I do not believe management’s projections are impossible or even unreasonable, I do not believe that they are likely. While all investment results are somewhat based upon management’s competence, at the present moment, GT shareholders are especially reliant upon management to produce excess returns.

Using my conservative estimate of normalized FCF (less the aforementioned additional interest expense), GT currently trades at an FCF multiple of approximately 7. And although GT possesses some probability of revenue growth in the foreseeable future, when its enormous debt and poor historical performance are taken into account, this multiple is justified.

Be the first to comment