WoodenheadWorld

Thesis

General American Investors (NYSE:GAM) is an equity focused closed end fund. The vehicle has a low leverage ratio of 14.6%, and aims to replicate the S&P 500 returns. The fund has an extremely long track record, being in this business for over 50 years. Portfolio managers come and go though, so we are going to be focused on its latest performance and its 5-year track record.

The fund has been successful at producing a total return in line with the S&P 500 in the past year, and in effect has outperformed in 2023 due to its technology tilt. The particularity of this fund resides in its ‘old school’ build where it does not distribute artificial dividends – the fund has a semi-annual distribution where capital gains and income are passed to investors (if there is anything to distribute). From that angle this fund is not here nor there given that CEF investors are accustomed to monthly ‘fat’ dividends, which are not always supported.

Given its long track record and ‘no surprises’ approach, the CEF has a very steady discount to NAV, which does not move around much. The discount is currently at -17%, but do not expect this to go to zero when the equity markets are back in rally mode. Expect a -15% discount, which is the top of the range here.

GAM is a robust, tried and tested CEF that matches the S&P 500. There is nothing to be overly enthusiastic here, but nothing to hate either. Investors who, for some reasons, do not like to accumulate capital gains via an outright index position, can conversely invest in GAM. From our standpoint we prefer CET, which we have covered here.

Performance

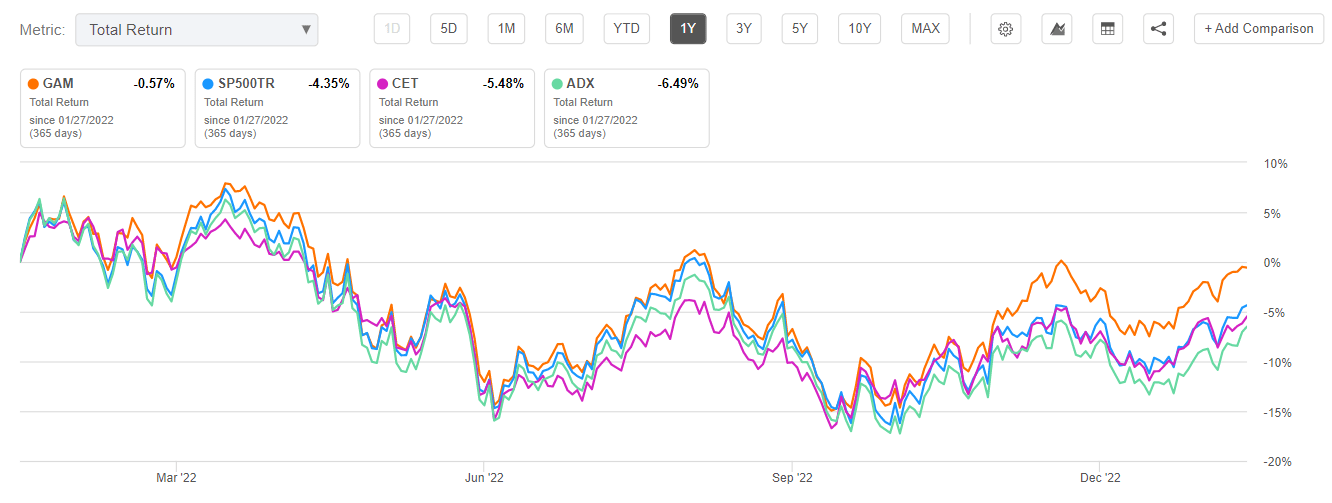

The fund has slightly outperformed the S&P 500 in the past year:

Total Return (Seeking Alpha)

We can see that GAM’s outperformance has started after the intermediate bottom in October 2022. Versus its peers Central Securities (CET) and Adams Diversified Equity Fund (ADX), GAM has done better as of late. The reason behind this modest outperformance is the technology tilt for the fund. Beaten down technology stocks are up significantly this year, with the poster child for unprofitable tech ARKK, up more than +30%.

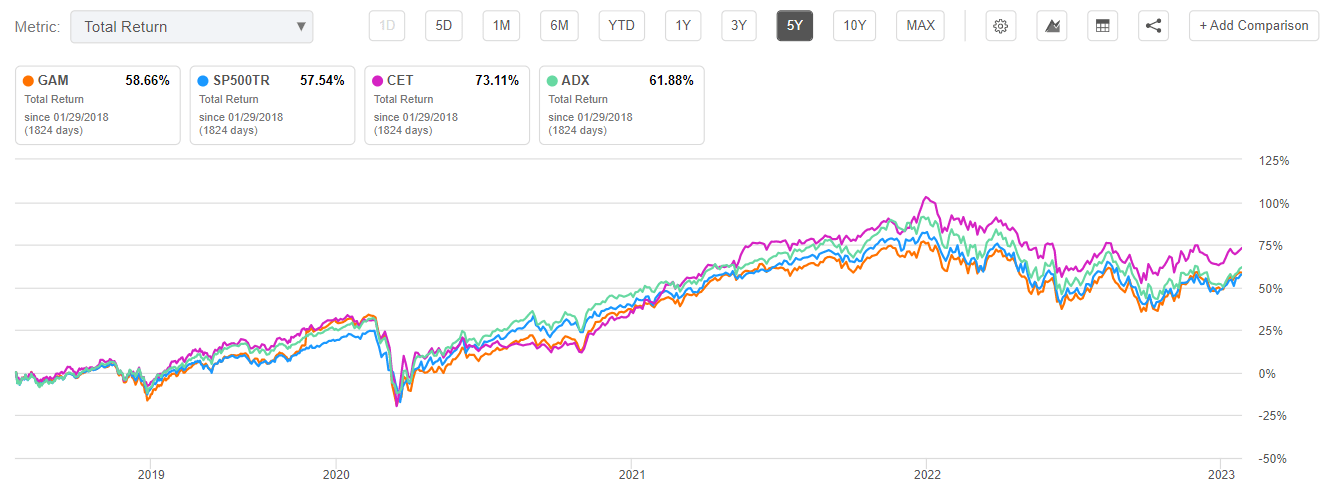

If we smooth out the recent performance by looking at total returns on a 5-year lookback we see GAM matching up with the S&P 500, but being outshined by CET and ADX:

Total Return (Seeking Alpha)

The cohort has a very low returns dispersion, but CET does outperform here for long periods of time. We would have expected GAM to do a little better after the 2020 Covid meltdown due to its leverage. Unfortunately it is not the case. GAM has a solid, robust performance, in line with the S&P 500 but no overshooting here.

Holdings

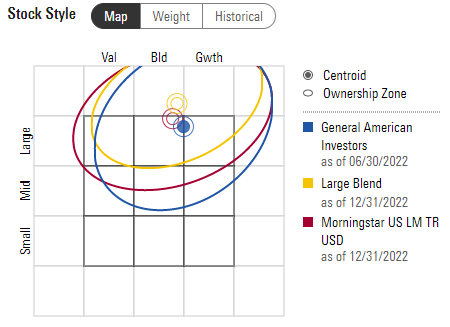

The fund’s portfolio falls in the Morningstar Large Cap / Growth box:

Style (Morningstar)

The fund tries to replicate the S&P 500 index total returns, but by holding fewer stocks, and following a “bottom up” construction approach:

We approach portfolio diversification by selecting companies individually, as described above, without reference to industry weightings in the Standard & Poor’s Index. We believe that adequate diversification can be achieved with a limited number of holdings (50 to 70) in diverse industries. Individual security weightings depend upon our assessment of the company’s potential for growth as well as the market liquidity of the security.

This is a smart approach, similar to what other good CEFs do. It is impossible to select 500 ‘great’ companies. In fact, due to its market weight build, the S&P 500 is in reality highly concentrated in sub 70 names itself.

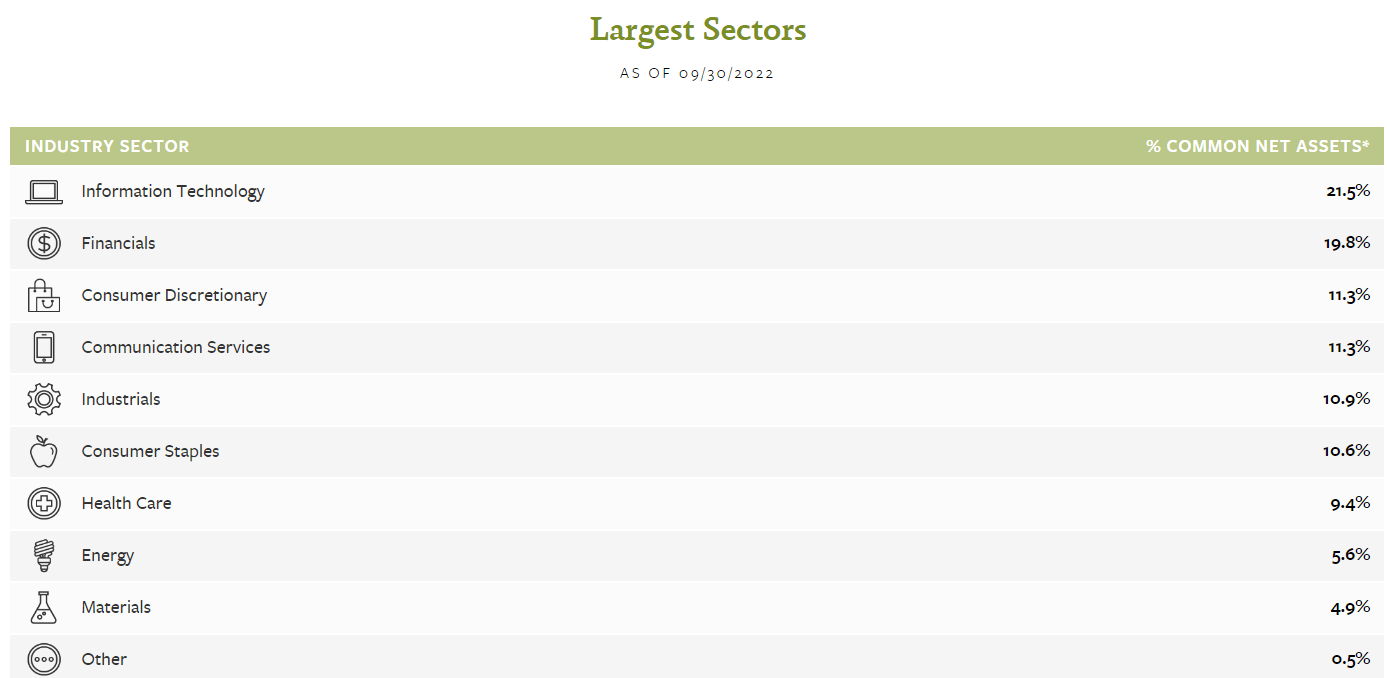

The GAM sectoral build has a growth tilt:

GAM Sectors (Fund Website)

We can see how information technology is the top sector in the portfolio currently, followed by financials.

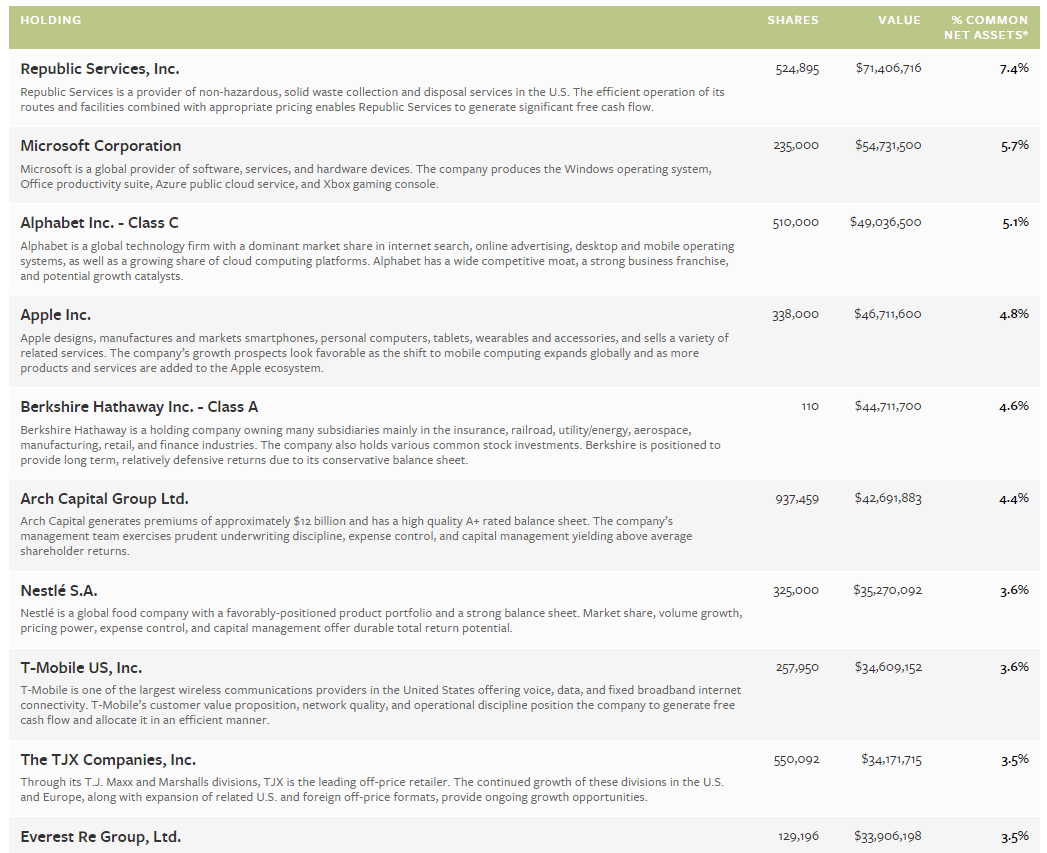

The top-10 names in the portfolio currently are:

Top 10 Holdings (Fund Website)

A number of ‘FAANG’ components are present, as well as other international large cap names.

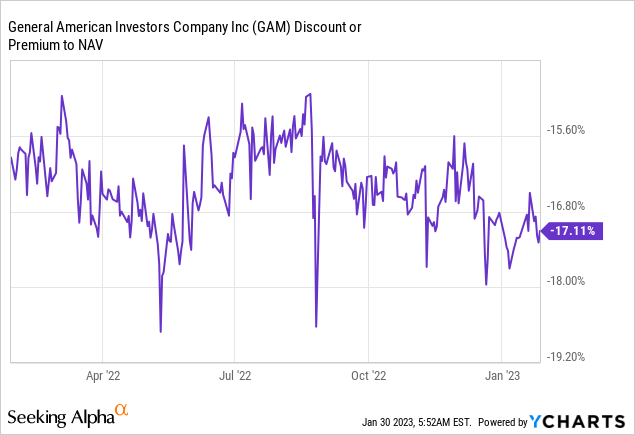

Premium/Discount

The fund’s discount to NAV has been fairly stable in the past year:

We can observe a tight -15% to -18% range here, with a low standard deviation. This CEF is ‘tried and tested’ given its extremely long tenure, thus the discount to NAV does not fluctuate that much.

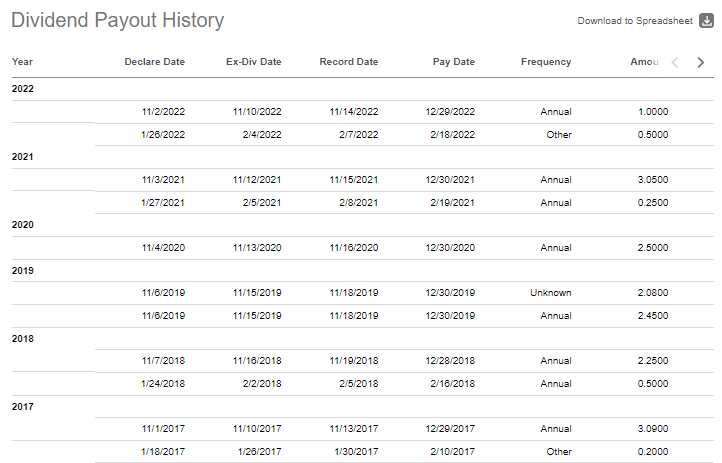

Distribution

The CEF is pretty straight forward from where it sources its dividends:

The Company’s dividend and distribution policy is to distribute to stockholders before year-end substantially all ordinary income estimated for the full year and capital gains realized during the ten-month period ended October 31 of that year. If any additional capital gains are realized and available or ordinary income is earned during the last two months of the year, a “spill-over” distribution of these amounts may be paid. Dividends and distributions on shares of Preferred Stock are paid quarterly.

The stocks in the portfolio pay interest income and can also produce capital gains if they appreciate during the period they are held. If there is no appreciation in the underlying portfolio then the dividends are limited. GAM therefore is more akin to an ETF from this perspective, because it does not have a managed distribution and only pays interest semi-annually:

Dividends (Seeking Alpha)

If this year is also poor in terms of equity returns, expect another low semi-annual distribution. This CEF does not like to use ROC.

Conclusion

GAM is an equity closed-end fund. The vehicle aims to replicate the S&P 500 total return, but with a much smaller portfolio. The CEF currently sports a very low leverage of 14%, achieved via preferred shares. The fund’s total return has matched the index in the past year, with a slight outperformance in 2023 as technology rallied (the vehicle has a growth tilt through its portfolio). GAM only distributes what it makes via semi-annual distributions. If equities do not perform, expect low dividends from GAM. This is not a fund that will offer unsupported eye popping dividend yields. GAM is a tried an tested CEF, and although it currently sports a -17% discount only expect this to narrow to -15% when the markets rally. In our minds GAM is a viable alternative for those investors who do not want to sit on substantial capital gains by outright investments in the index.

Be the first to comment