FangXiaNuo/E+ via Getty Images

Summary

Often described internationally as China’s Twitter equivalent, Weibo (NASDAQ:WB) is one of the leading social media platforms in China. In the US social media context, Weibo can be thought of as combining elements of many platforms including Twitter, Facebook and Medium, and having greater functionality than Twitter. China tech shares have rallied strongly from their October 2022 lows, and Weibo at $22.97, has more than doubled from its 52-week low of $10.02. However, it is still down significantly from its 52 week high of $35.16 and at a price level not seen since 2016, until last year.

The major price decline is a result of a significant decline in its financial performance in FY2022, due to weak advertising demand amidst a slower economic environment and disruptions from Covid-19 resurgence in China. However, if Weibo can rebound towards its 2021 operating performance, then Weibo looks very attractive value presently. Weibo currently has a market cap of $5.43billion and enterprise value of $4.91billion. GAAP net income attributable to shareholders was $428.3million in FYE 31 December 2021. If we exclude 2021 fair value changes in investments of negative $176.34million, adjusted net income would be $604.6million. On this basis, Weibo trades at EV to illustrative 2021 adjusted net income of 8.12x.

Besides, there is the potential for an event catalyst for Weibo. In July 2021 when Weibo was trading at around $60, it was reported that Chairman Charles Chao was exploring a privatization of the company with a state investor. This was immediately denied by Chairman Chao and Weibo. However, now that Weibo’s stock price is much lower, it looks interesting to examine the potential for a take-private by Mr. Chao. Further, a divestment by Alibaba of its 29.8% stake in the company has been an ongoing possibility. In December 2021, Alibaba was reported to be in talks with a state-owned investor to divest its stake.

Earlier this month, China’s top central bank official stated that the tech crackdown was “basically” over, per CNN. Jack Ma also relinquished control of Ant Financial this month. Alibaba’s divesting of its Weibo stake may be a final matter for closure by Alibaba, e.g. to exit out of its presence in media businesses. I view that a China state-owned investor investing in Weibo would be very positive for Weibo, whether it is in acquiring Alibaba’s stake solely or as part of a privatization of the company with Mr. Chao, which I will discuss further later.

Company overview and financial performance

Founded in 2009, Weibo (meaning microblogging in Chinese) is one of the largest social media platforms in China. Wikipedia describes that

although often described as a Chinese version of Twitter, Sina Weibo combines elements of Twitter, Facebook, and Medium, along with other social media platforms. Sina Weibo users interact more than Twitter users do, and while many topics that go viral on Weibo also originate from the platform itself, Twitter topics often come from outside news or events.”

Weibo has monthly active users of 584 million in September 2022, a net addition of approximately 11 million users on a year-over-year basis, and daily active users of 253million, a net addition of approximately 5 million users on a year-over-year basis. Whilst not directly comparable, we can note that Twitter has 450million monthly active users. Twitter was acquired by Elon Musk for $44billion, and assuming a 60.22% mark-down since then as Twitter shareholder Fidelity has done, Twitter would have a valuation of $17.50billion presently. So, Weibo is presently valued at less than a third of Twitter’s valuation.

Weibo’s largest shareholder is Sina Group owns 44.7% of shares with 70.8% of voting rights, whilst Alibaba (BABA) holds 29.8% of shares and 15.7% voting power. Sina Group is owned by Charles Chao and Sina management. Alibaba’s stake was initiated in 2013, when it acquired 18% of Sina Weibo for $586million in 2013, translating to a valuation of $3.255billion for Weibo at the time. Alibaba subsequently exercised an option to increase its stake to 30% when Weibo was listed on Nasdaq in April 2014. Alibaba is also a major customer of Weibo in terms of advertising revenue.

As at its last report, Weibo had total cash and short-term investments of $2.9603billion. It also had long-term debt of $1.540billion and current debt of $899.6million. This gives total debt of $2.4396billion. So, we have a net cash position of $520million, which looks good. Based on this, Weibo has a current enterprise value of $4.91billion.

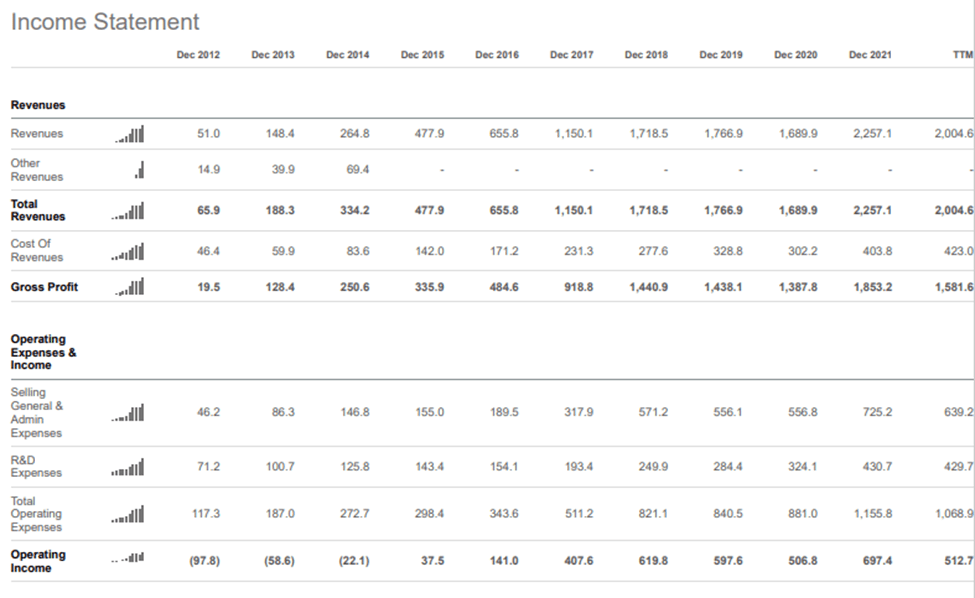

Historical financial performance of Weibo is shown below. As mentioned, based on FY2021 net income excluding negative fair value changes of investments, Weibo trades at EV/2021 net income of 8.12x presently. I prefer to look at net income of Weibo through the lens of excluding the annual fair value change of investments which are booked into GAAP net income.

For the nine months of 2022, net loss attributable to shareholders was a loss of $56.3million, which included impairment on fair value change of investments of negative $309.5million. Excluding this fair value change from net income gives a net profit of $242million for the 9 months. If we annualized this 9 month “adjusted” net income, we would have net profit of $322.6million. So, we have a hypothetical EV/2022 annualized adjusted net income multiple of 15.2x.

Seeking Alpha

Seeking Alpha

Net revenues for the third quarter 2022 were $453.6million, down 20% year-on-year on a constant currency basis. Weibo’s operating margin was 27%, compared to 35% in the previous year period. The result was “primarily due to weak advertising demand amid macro headwinds and disruptions from COVID-19 resurgence in mainland China.“

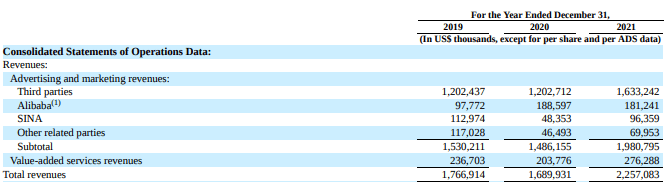

82.4% of Weibo’s advertising and marketing revenue in FY2021 was derived from third parties. Related parties Alibaba contributed 9.14%, SINA contributed 4.86% whilst other related parties contributed 3.53%.

Weibo annual report

China’s economic outlook and Weibo outlook

Weibo’s 2022 financial performance was significantly impacted by the macro headwinds in China and disruptions from Covid-19 resurgence. China’s GDP grew at only 3% in 2022.

In Weibo’s FY2022 Q3 conference call, Weibo CEO Gaofei Wang described the close relationship of Weibo’s advertising revenue and its recovery with that of the macroeconomic outlook in China, in response to Citi analyst Alicia Yap’s question:

Gaofei Wang

All right. Thank you for the question. So with regards to the Q4 and also the 2023 performance. So you can see, first of all, I’d like to talk to you about the structure of our basement. So 2/3 of the industries are actually related to consumption, for example, FMCG or 3C products as well as the e-commerce. So you can see that the recoveries is highly related to the macro.

Weibo should see a significant rebound in advertising revenue in 2023 amidst a rebound in economic growth in China. In 2023, China GDP growth is expected to rebound to 4.9%. Reuters reported that “government advisers told Reuters last month they would recommend the conference adopt 2023 growth targets ranging from 4.5% to 5.5%, while a central bank adviser said last month that China should set a target no lower than 5.” Credit growth is expected to be further expansionary and there are also expectations for a cut in rates, in contrast to the tightening seen in other global markets.

Further, the expected expansionary macro environment in China and desire to support GDP targets makes China and Hong Kong exposure a preferred choice for equities in 2023, in my view.

Potential event catalysts

In July 2021, it was reported by Reuters (and subsequently widely covered) that Weibo Chairman Charles Chao was exploring a privatization of Weibo with a state investor at an offer price of $90-$100. Weibo was trading at the $60 levels around the time of the news, which was denied by Chairman Chao and Weibo. Now, Weibo trades at barely over a third of the price then.

In 2021, Charles Chao completed the privatization of Sina, Weibo’s largest shareholder, which owns other tech businesses. Some of the possible motivations for the privatization was the undervalue of Sina on the US market and the potential for a significantly higher valuation in a future re-listing on a China exchange. Shanghai’s Composite Index has rallied from its October year low, to presently trade at the higher end of its 5 year historical range. Buoyant capital markets in China may prompt renewed speculation of privatizations of China tech companies in the US and re-listings in China. Significant economic growth in China in 2023 can also be expected to provide further tailwinds to China’s financial centers and stock exchanges.

Further, there lies the question of what Alibaba may do with its 29.8% Weibo stake. Divestment by Alibaba seems like a probable outcome; to exit out of its media-related businesses. This year and in recent years, China’s government has taken 1% golden shares stakes in several China tech companies. Per CNN, golden shares “give the government decisive voting rights or veto power over certain business decisions or – in the case of internet companies – content.”

Various commentators quoted in the CNN article expressed negative views on the golden share stakes. On the contrary, China’s government shareholding in China tech companies is a major positive, in my view. Across the globe, tightening regulation and scrutiny of the big tech companies by governments globally will inevitably continue, as we have seen for US big tech. The past “move fast and break things” approach of many “disruptive” US tech upstarts that disregarded regulators in US and other Western markets, is evolving by necessity into a more collaborative approach between tech companies and governments globally. Therefore, wherever it is that one invests in tech companies, regulatory risk is likely always going to be a potential risk factor for investors in global large tech companies. Now consider the opportunity in China if the government is a major investor in a tech company, and thus assists in supporting the growth of the company and in ensuring its appropriate navigation of pertinent issues, such as content. This outcome would be a major positive and should make China a top pick for global tech investors.

There was a positive market reaction to the news of the Chinese government taking 1% golden share stakes in Alibaba and Tencent earlier this month. Alibaba’s potential sale of its 29.8% Weibo stake to a state-owned investor would be an even bigger positive, if it occurs. Weibo would become possibly the first of the major Chinese tech companies with China’s government as a top major shareholder. I envisage that this could be highly collaborative in many ways, such as 1) the state-owned investor’s ensuring Weibo’s appropriate navigation of issues such as content, thus mitigating regulatory risk; 2) lower debt financing costs from having the state as a major shareholder; 3) advertising revenue from the government’s state-owned and state-controlled enterprises; 4) general support for the growth and expansion of the company.

Potential added margin of safety

Weibo has an existing $500million share repurchase program announced in March 2022. As of 30 September 2022, the company had purchased approximately 3.1 million ADSs under this program for a total cost of $57.7 million, translating to an average cost of $18.61. Since Weibo’s share price hit a low of in October, there may have been further shares repurchased since September. There is presumably still a very large amount available of the share repurchase program that can be deployed going forward.

Potential Risk Factors

I am very bullish on Weibo due to the reasons previously described. At the same time, we should consider the potential risk factors. The main risk factors relate to the flip-side scenarios of the bullish reasons described.

Weibo has seen its advertising revenue significantly affected by the 2022 slow-down in China. Weibo’s current stock valuation looks very attractive assuming a rebound in financial performance to or near its 2021 performance. Based on the previously described 2022 trailing numbers, it does not necessarily look cheap though. If the economic rebound is below expectations in 2023, Weibo’s 2023 financial performance may be below expectations.

Alibaba’s divestment of its Weibo stake may result in a reduction in revenue from Alibaba as a customer. There is a meaningful (9.14% in 2021) amount of advertising revenue that is derived from Alibaba.

Although I view that regulatory risks going forward would be mitigated by having the government as a shareholder (via golden shares or if a state investor buys out Alibaba’s stake), it is to be seen if this will be the case.

Conclusion

Weibo looks poised to see significant upside from its current price levels, based on an expected rebound in financial performance in 2023. I view that at least a 15x multiple of net income excluding fair value changes of investments is appropriate for Weibo, as a leading social media platform and prized tech asset in China. FY2020 net income excluding fair value changes was $488.1million, and assuming a 15x multiple on this gives a $7.321billion valuation, or $30.94 per share representing about 35% upside. I also view price support at the low $20 levels in the near term, therefore non-significant short-term downside, and that any dips are good buying opportunities. Besides, there are the potential event catalysts that could arise from a potential privatization offer and/or a divestment by Alibaba of its 29.8% stake. There are multiple paths for significant upside in 2023 from the current stock price levels, in my view.

Be the first to comment