Sky_Blue

GasLog Partners (NYSE:GLOP) is an international LNG transport company that has offices in the United States, Greece, the United Kingdom, and Singapore. The company was founded by its current chairman, Peter Livanos, who is a Greek shipping tycoon and comes from a family that has been operating in the Greek shipping industry for more than 100 years. GasLog is an LP Unit or Limited Partner, which means that a share represents a unit of ownership in a master limited partnership rather than the company itself. For shareholder purposes, there isn’t much of a difference between the two apart from taxation considerations which are outside of the scope of this article. The recent volatility in oil prices made everything that had anything to do with energy a focus for investors. This is a new sensation for master limited partnerships like GasLog. These tend to be very investor-specific and somewhat unknown. In fact, many investors will have spent their entire lives buying and selling stocks without ever owning an MLP.

Company Outlook

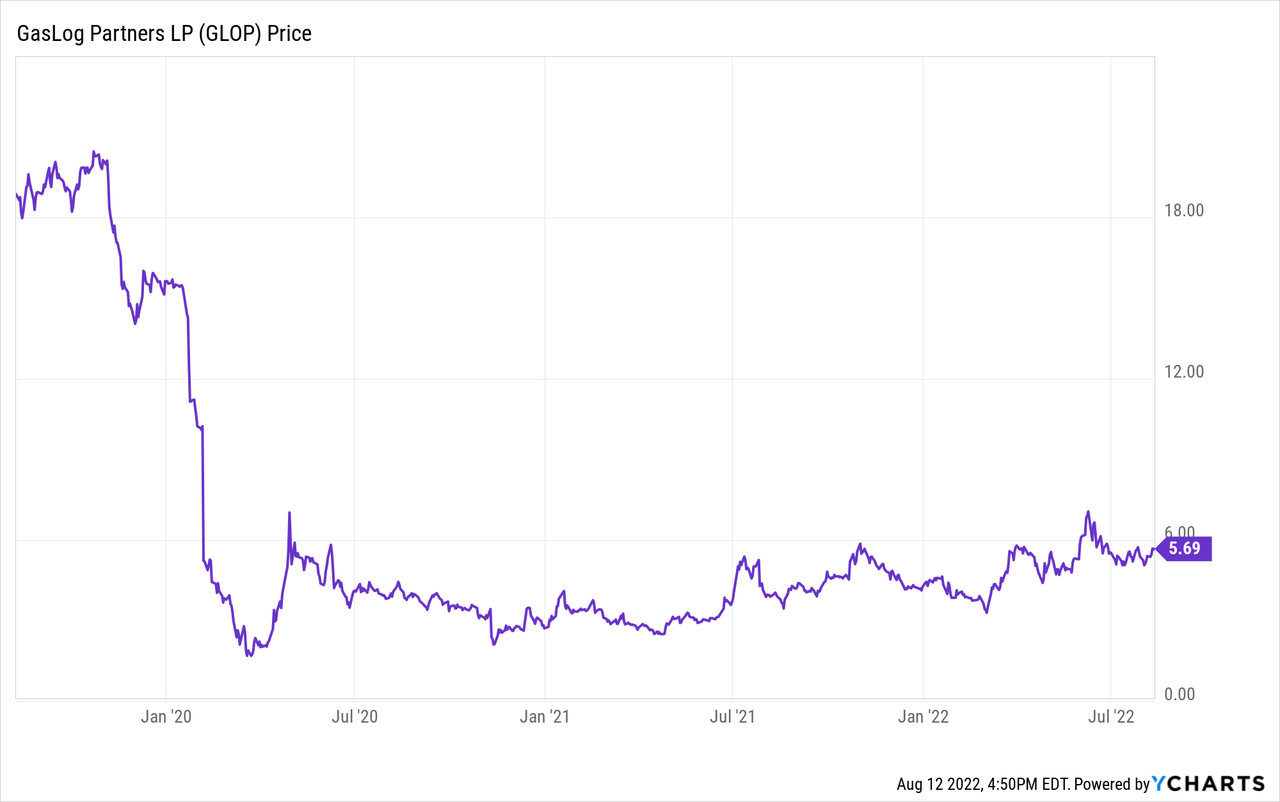

GasLog currently has a market capitalization of $290 million and pays out an annualized dividend yield of 0.71% per share. With LNG demand rising due to the economic sanctions against Russia for its invasion of Ukraine, the LNG transport industry has been one of the better performing sectors so far this year. GasLog’s stock has gained 36.6% in 2022 and over 75% during the past 52 weeks of trading.

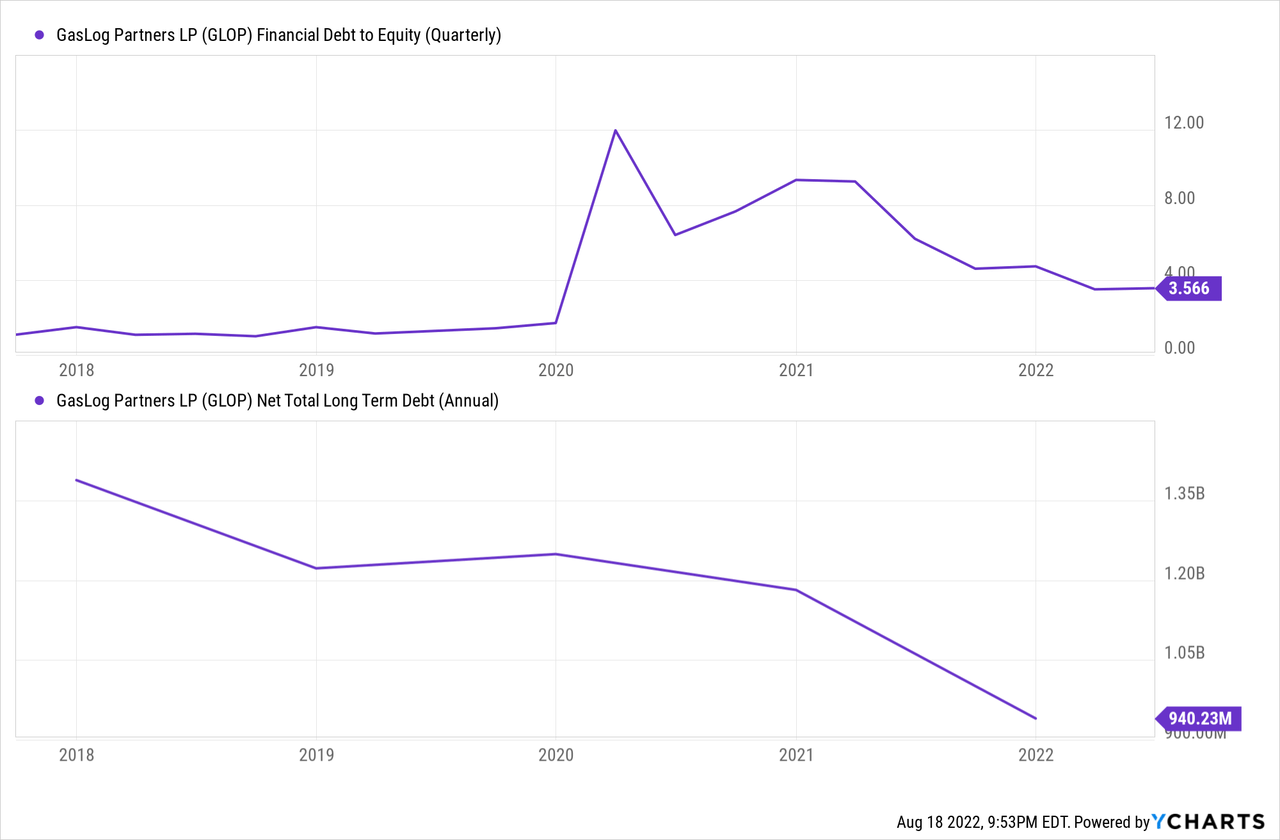

GasLog has grown its transport fleet from three to a current total of 15 vessels, having added two new ships in the last six months. The company has been savvy with its finances and has used the sudden bump in stock price and rise in business to pay down some of its debts. Over the past year, the company has retired more than $112 million in debt and lease payments, creating a stronger balance sheet.

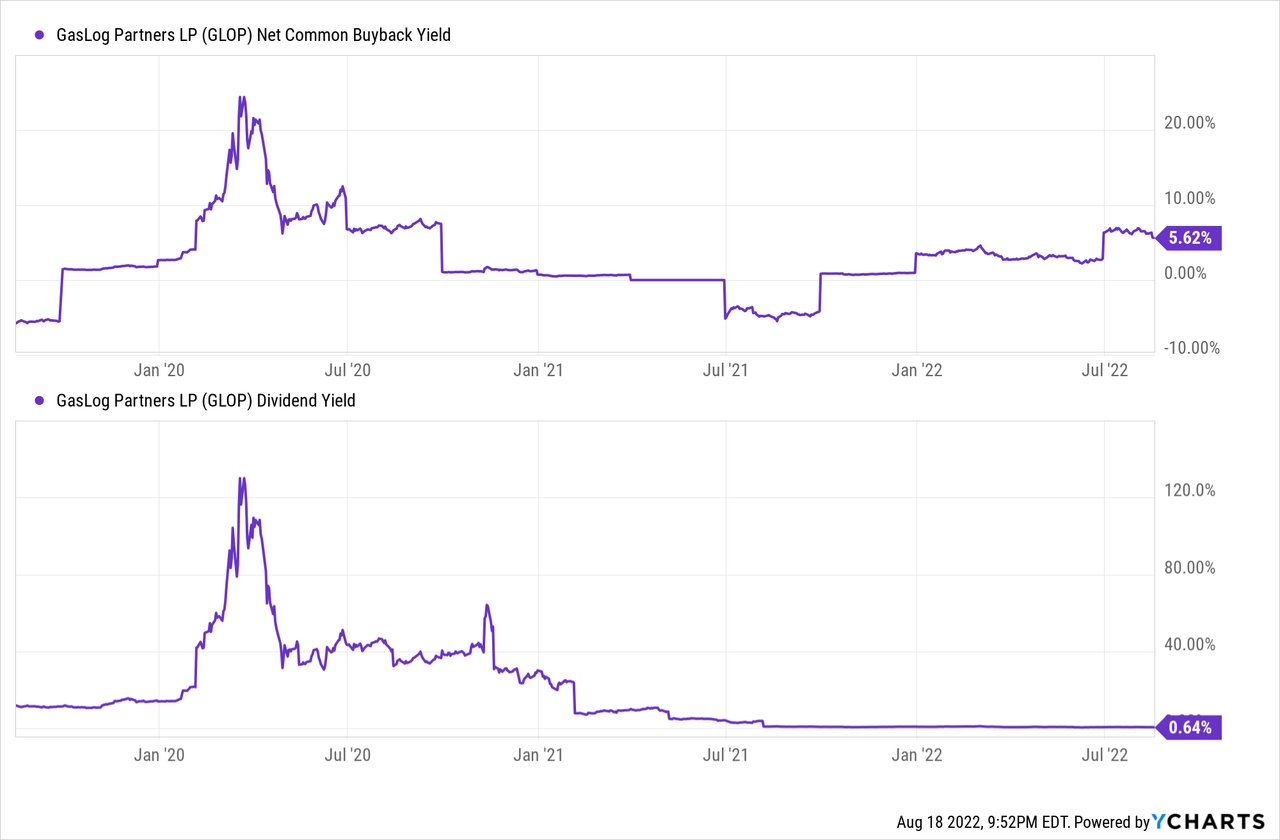

It has also used that influx of cash to strengthen shareholder equity by buying back $10 million in units with a plan for a total of $28 million in unit buybacks. The dividend is somewhat paltry, but investors are still seeing some return, and there is the potential to hike the dividends in the future should the stock rise to elevated levels, making buybacks less attractive. But in the end, there’s really not much to be excited about here.

Forward-Looking Commentary

In the longer term, it is important to remember that the European Union has shifted its focus to using LNG as a primary energy source, which has further limited global reserves of LNG. The general expectation is that the global push towards renewables, along with elevated oil prices, will provide tailwinds for LNG pricing at least through winter 2022. Cold winters greatly increase energy demand, and while I am certainly not a meteorologist, I would expect global energy prices to remain elevated at least until early 2023.

While LNG is becoming more and more mainstream, oil prices are still the most important variable to consider. With oil coming off of historic highs, there are a number of possible headwinds to consider. The economic sanctions against Russia will play a role, but over time it’s likely that Russian oil will find its way to the market in one form or another. There is also the fact that elevated energy prices will continue to be an untenable political position for global leaders in developed countries.

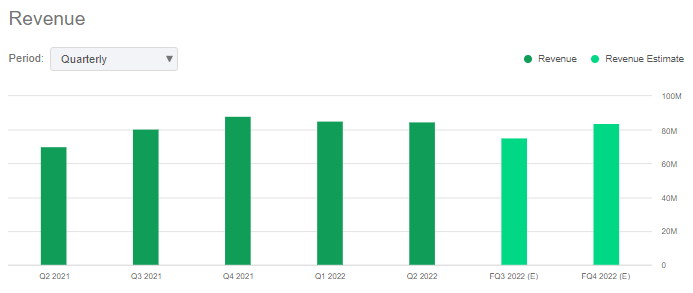

When we look at revenue trends, we can see that the current perfect storm has produced less than stellar results for the company and that it would be imprudent to expect a sensational improvement over the next few quarters.

Seeking Alpha

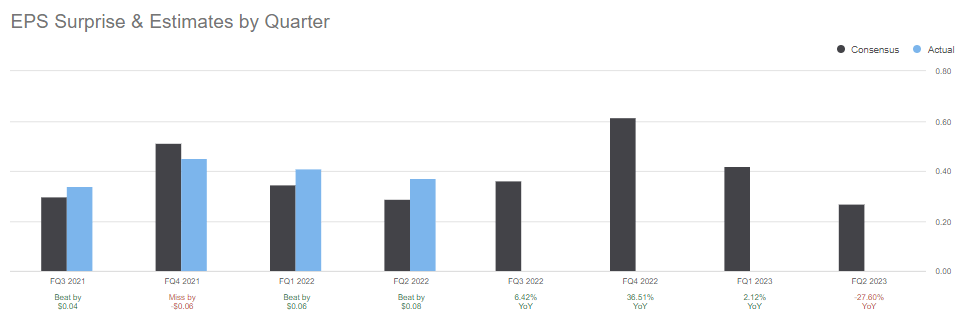

The firm also does a fairly good job of delivering on its earnings expectations. The company has managed to beat on three of the last four quarters, with no bombastic misses.

Seeking Alpha

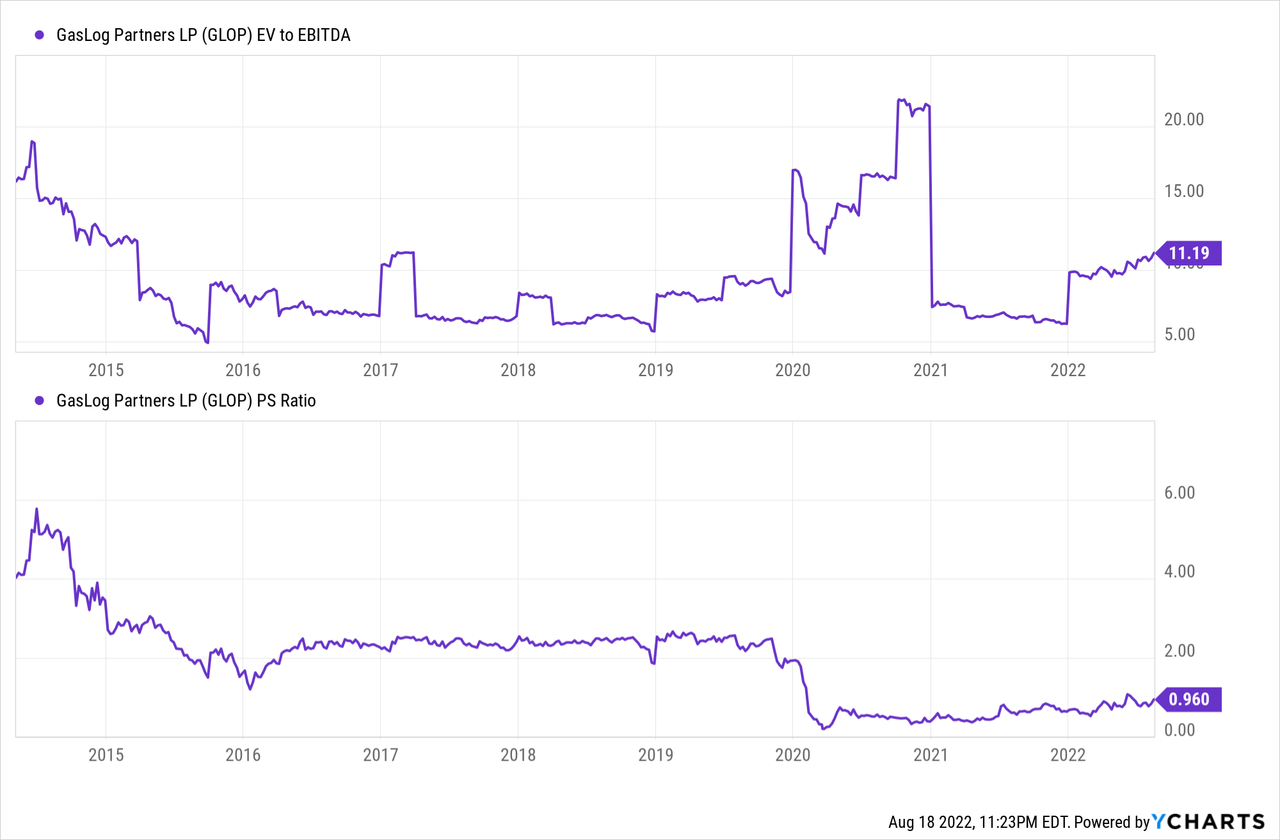

Despite this, value investors might have seen the ship sail on buying GasLog at a discount. After some lofty gains over the past year of trading, savvy investors may want to sit on the side lines until the price of the stock stabilizes. Despite its efforts, the company still has a massive debt load of over $1 billion, mostly due to leasing vessels and other fixed costs. One might look at the low price to sales multiple of 0.96 and argue that the stock is trading at depressed levels, but it is important to note that MLPs on a whole seem to have lost mainstream attention and, for the most part, don’t trade at the extreme multiples that we are used to in other segments.

So it would be prudent to manage expectations here, we aren’t talking about a high-flying technology stock, and even though GasLog is having one of the best moments of its existence, investors shouldn’t expect another sensational move going forward.

The Takeaway

Investors who bought into the stock following the 2020 meltdown will likely be feeling pretty good about their position here. They should be taking a victory lap and possibly be thinking about taking some profits here. The chart has been a slow but steady mover, the company is in an amazing moment, but the easy money has likely been made. Winter will likely bring more elevated energy prices, but one does get the feeling that we are a bit late in the game for energy stocks right now. There isn’t a pressing need to sell, but there are also no greatly compelling reasons to buy right now. I rate the stock as a hold.

Be the first to comment