FabrikaCr/iStock via Getty Images

Freeport-McMoRan Inc. (NYSE:FCX) is one of the largest copper producers in the world, although due to the nature of copper mines it also has substantial gold production (with some moderate molybdenum). Due to the inelastic nature of supply here (once a mine is producing, operating costs are low), the industry remains susceptible to fluctuations in demand (making it a very cyclical industry).

The company’s stock has declined more than 40% from its 52-week highs, as the once high-flying company has been impacted by potential economic weakness. However, as we’ll see throughout this article, the company’s unique positioning and long-term demand for its assets make it a valuable investment.

Freeport-McMoran Financial Results

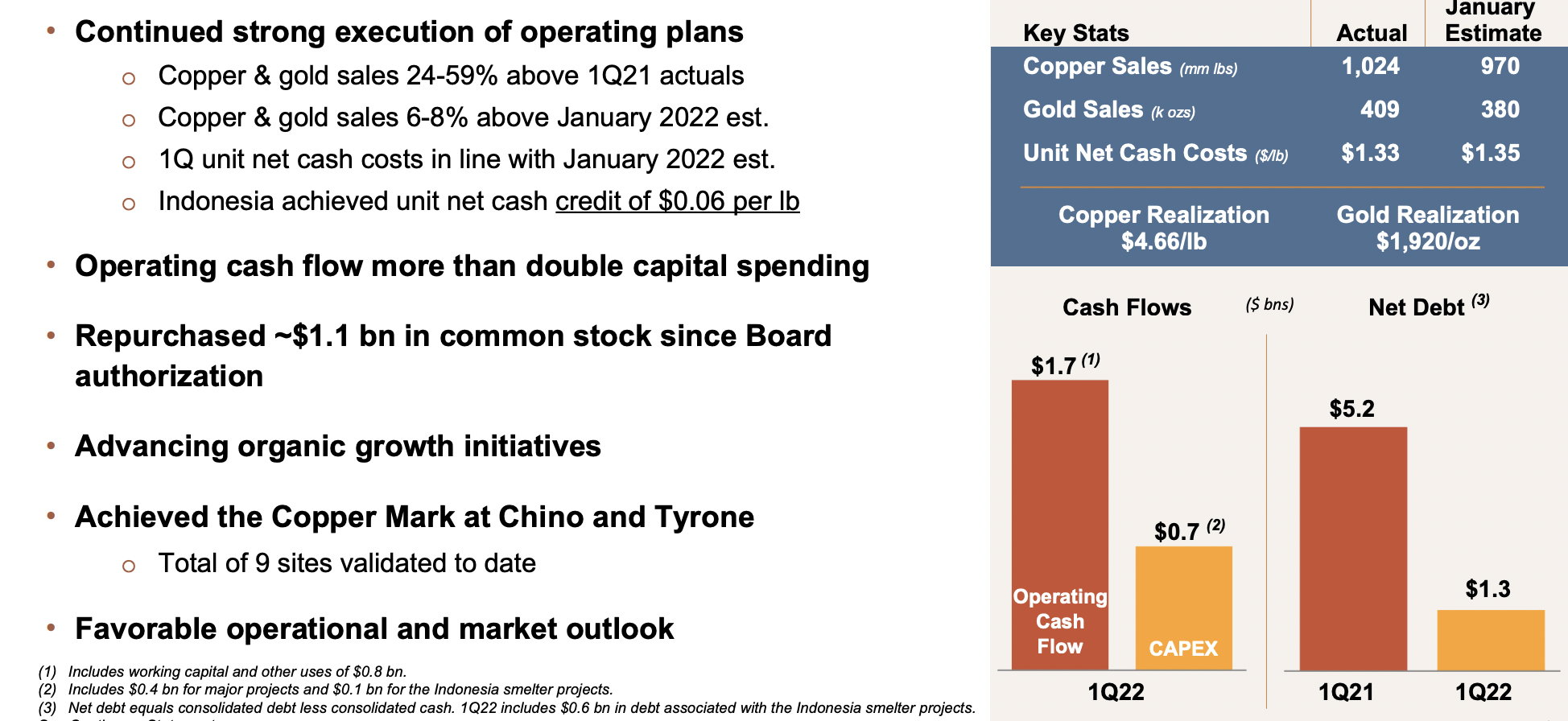

Financially, Freeport-McMoRan had a strong quarter, highlighting the company’s financial position.

Freeport-McMoRan Financials – Freeport-McMoRan Investor Presentation.

The company saw strong YoY sales increases with mid-to-high single digit outperformance versus the company’s initial investments. The company saw operating cash flow at more than double capital spending, leaving $1 billion in FCF for the quarter and giving the company a FCF yield of roughly 9% for shareholders.

The company has continued to focus on shareholder returns. It’s continuing to chase growth projects, with a very manageable $1.3 billion in net debt. We’re also excited to see the company’s share repurchases, which highlight its commitment to long-term returns. While copper prices have fallen significantly, gold prices have remained stronger, meaning cash credits should remain high.

Freeport-McMoRan and a Recession

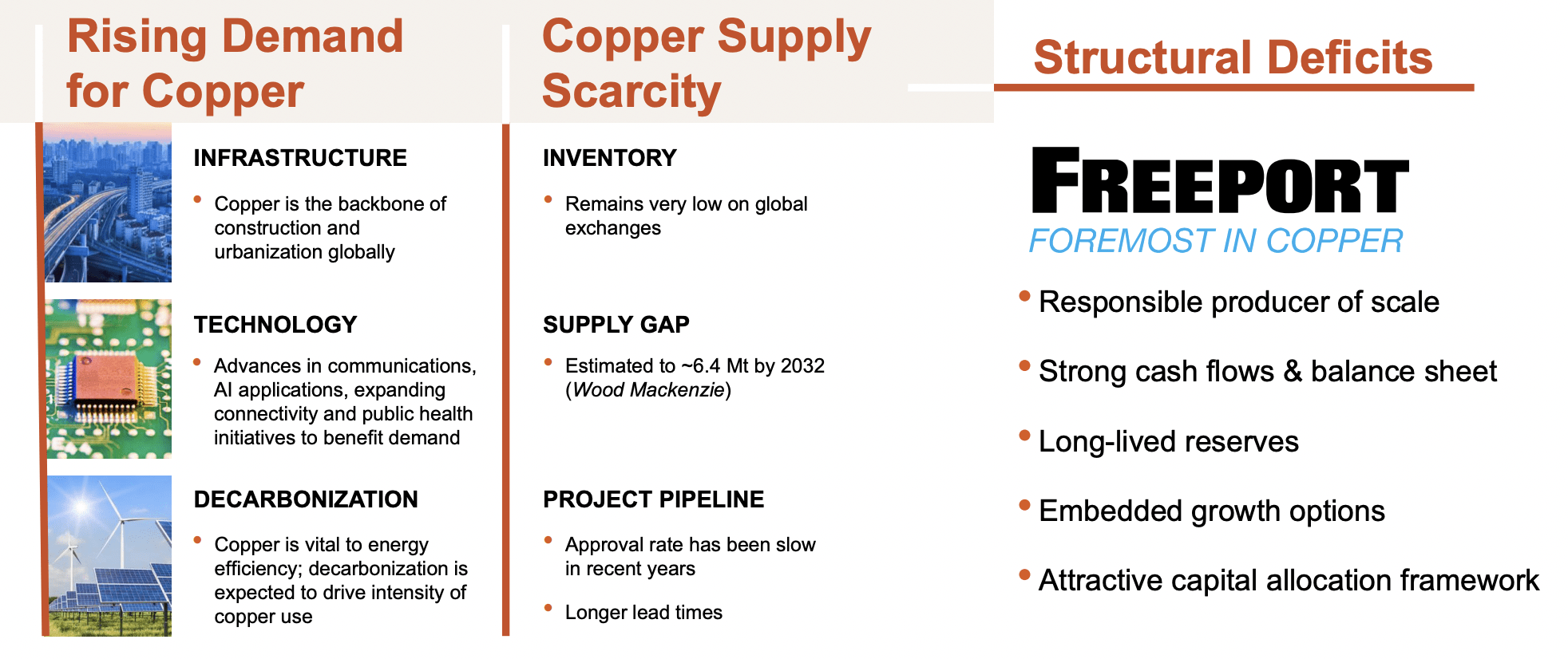

Freeport-McMoRan operates in a clearly cyclical market, although with strong long-term potential.

Freeport-McMoRan Positioning – Freeport-McMoRan Investor Presentation.

In the short-term, copper prices are roughly 20% below their peaks. That’s because copper demand is heavily infrastructure and technology based, and capital spending tends to dramatically slow down in a recession. With high interest rates, and a concerned market, along with global conflict, fears over global economic strength are pressuring copper prices.

Long-term, though, we see a $4+ / pound price range as a new normal. Inventory remains low, and finding and developing large copper deposits remains difficult. The majority of copper production comes from several companies with several “mega-deposits” such as the Grasberg mine in Indonesia.

The takeaway here for investors is, expect short-term weakness, but also expect long-term strength in prices.

Freeport-McMoRan Operations and Growth

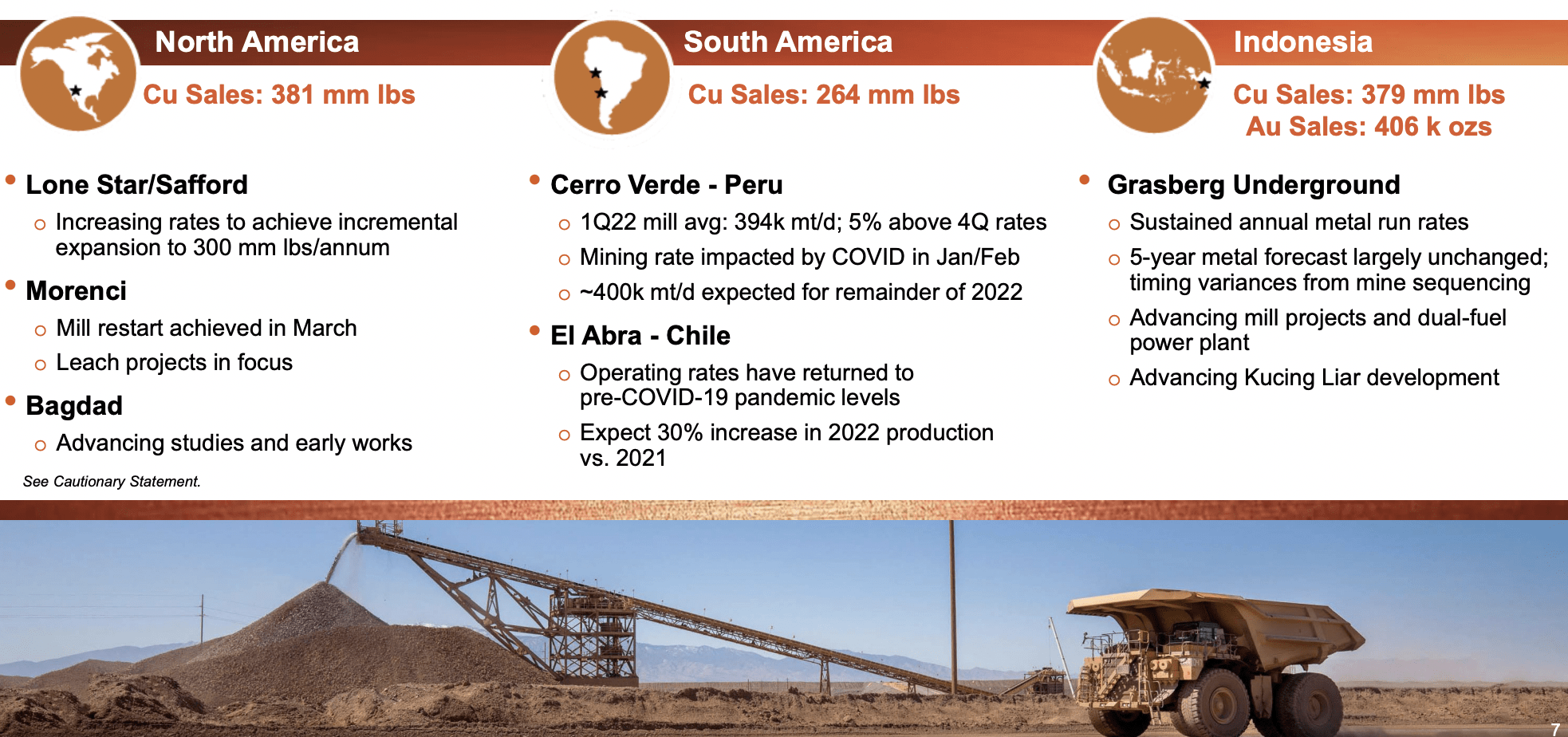

For those looking at Freeport-McMoRan’s FCF (free cash flow) yield in an up-cycle and shaking their heads, it’s worth noting the company’s capital is continuing to support growth.

Freeport-McMoRan Operations and Growth – Freeport-McMoRan Investor Presentation.

Freeport-McMoRan has three major centers of copper production: North America, South America, and Indonesia. In North America, the company is expanding its Lone Star / Stafford projects substantially, while also looking for room to expand other projects, in what is a stable operating environment for the company.

In South America, the company had strong COVID-19 impacts, but has since recovered, and expects that recovery to continue. El Abra is a classic example of this, where 2022 production is expected to be 30% greater than 2021 production. Lastly in Indonesia, the company has continued to revamp the mine and move onto new assets.

In Indonesia, concluded negotiations with the government have provided the company with a much more stable runway.

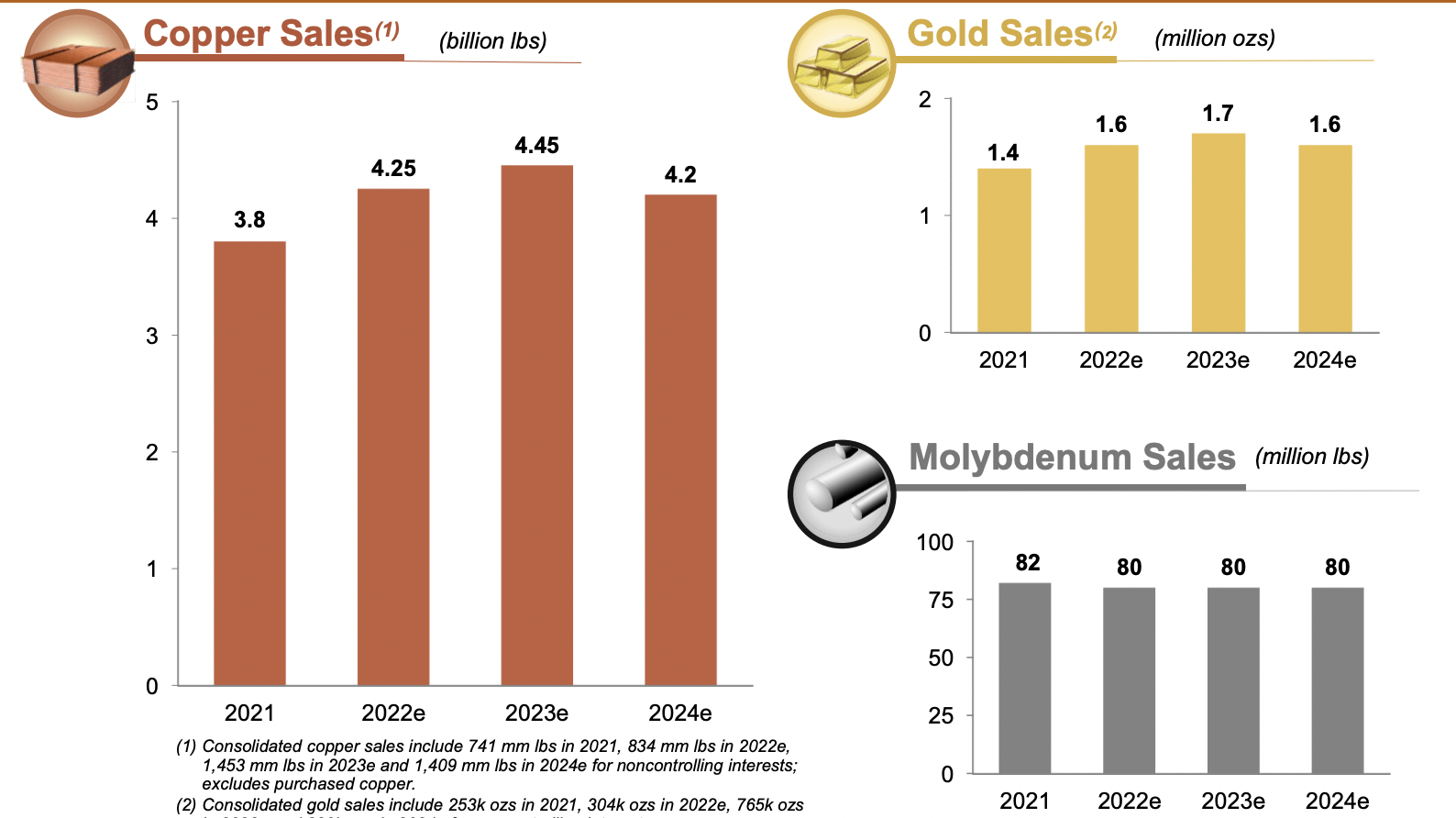

Freeport-McMoRan Sales Forecast – Freeport-McMoRan Investor Presentation.

The company’s $3.2 billion in planned 2022 capital spending represents a peak, with that spending expected to fall almost 10% in 2023 and continue to decrease from that point. The company’s production is expected to remain constant for the next several years at current spending rates, although 2023e will see roughly 5% higher production.

As a result, in a price agnostic environment, we view the company’s FCF for 2022 as a trough versus the next several years.

Freeport-McMoRan Shareholder Returns

From the company’s asset portfolio, Freeport-McMoRan has the ability to drive substantial shareholder rewards.

Freeport-McMoRan Shareholder Rewards – Freeport-McMoRan Investor Presentation.

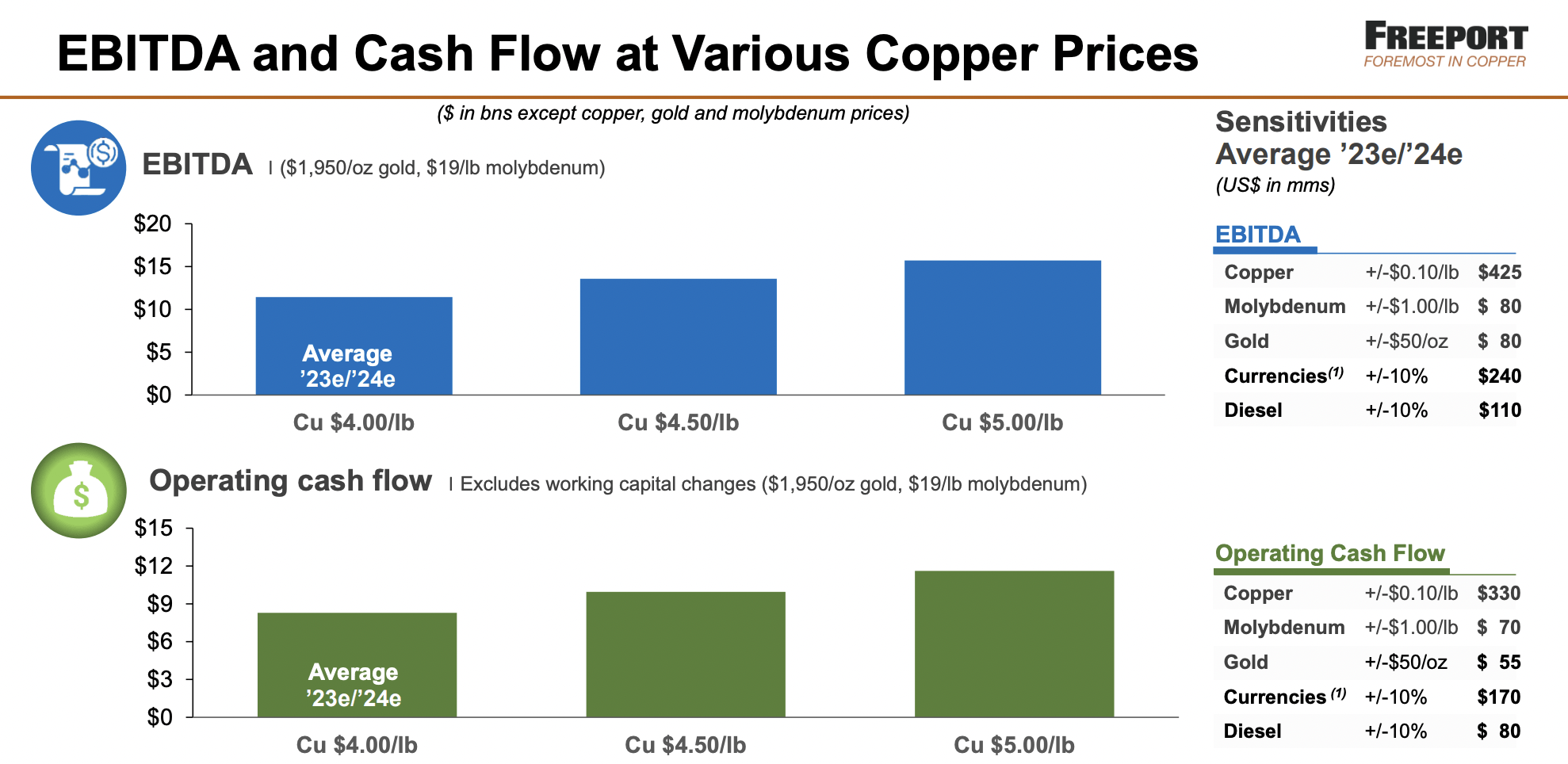

Freeport-McMoRan has the ability to generate $9-10 billion in operating cash flow for the 2023-2024 period (assuming copper prices are in the $4-4.5 range). The company’s capital spending over this time period will be around $5 billion implying roughly $13-15 billion in FCF (~30% cash flow yield for the overall two-year period or a ~15% annualized FCF yield for the company throughout this period).

The company has repurchased roughly 2% of its float since the start of its share repurchase program, and, at current prices can repurchase ~4% of its float. The company can do those repurchases with 2022’s FCF alone without increasing its debt, and purchased $600+ million in the 1Q 2022 alone, implying an annualized rate of ~$2.5 billion.

Going forward, regardless of how the company uses the cash, we expect it to generate substantial shareholder returns.

Thesis Risk

The largest risk to our thesis is volatility in the global markets. Copper prices (along with other industrial precious metals) tend to see very volatile demand in a volatile market. Large scale capital projects are among the first cut in a recession. Similarly, new technologies that increasingly use copper are placed on the back-burner.

This effect is evident in copper’s price performance over the past few months. Should copper prices continue to decline, Freeport-McMoRan’s ability to generate strong profits will suffer.

Conclusion

We recommend Freeport-McMoRan as a buy. Freeport-McMoRan has a unique and impressive portfolio of assets. The company is continuing to invest capital to slowly ramp up production, with 2023-2024 production expected to be noticeably higher than the 2021-2022 period. At the same time, the company is seeing increased reliable and strong performance across its entire asset portfolio.

Despite concerns about the global economy, the company generates strong cash flow at $4+ / barrel copper. We expect the company to be able to utilize that cash flow to generate substantial shareholder rewards, making the company a valuable investment for investors. The current dip will enable the company to accelerate its share repurchase program while generating other forms of returns.

Be the first to comment