da-kuk

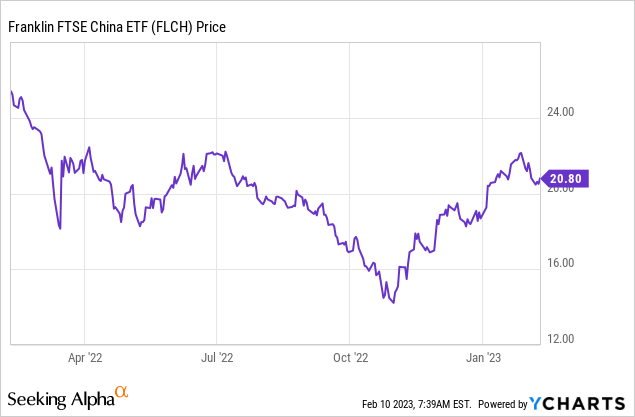

Along with the rest of the Chinese equity universe, the Franklin FTSE China ETF (NYSEARCA:FLCH) was sold off aggressively last year on concerns that the region had become ‘uninvestable’ amid regulatory crackdowns across key industries and authorities doubling down on the ‘zero-COVID’ policy. Yet, the year ended on a promising note, with the administration abruptly reopening the economy and a new He Lifeng-led economic team set to take over. In turn, investor sentiment has turned bullish on the post-COVID growth potential, leading equities higher in recent months in line with faster-than-expected reopening progress.

As I noted in my prior coverage of similar publicly-listed Chinese funds (see here), high-frequency data from the Lunar New Year have been positive as well, supporting the case for a better consumption-led economic growth outlook for 2023. With a return to growth in China likely to keep earnings up and support the RMB, FLCH investors stand to gain both ways (via valuation and FX upside).

Fund Overview – Ultra Low-Cost Consumer-Focused Chinese Exposure

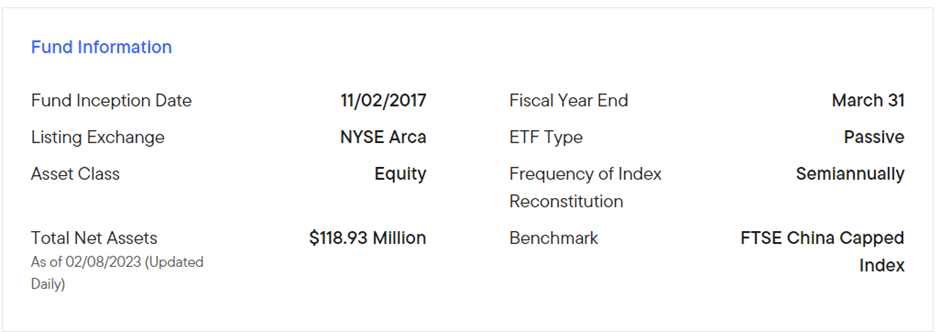

The NYSE-listed Franklin FTSE China ETF seeks to track, before fees and expenses, the performance of the FTSE China Capped Index, a market cap-weighted index comprising Chinese large and mid-cap equities. The ETF held $119m of net assets at the time of writing and charged a 0.19% expense ratio, making it one of the most cost-effective options for US investors looking to access Chinese equities. Key data on the ETF is as per the graphic below:

Franklin Templeton

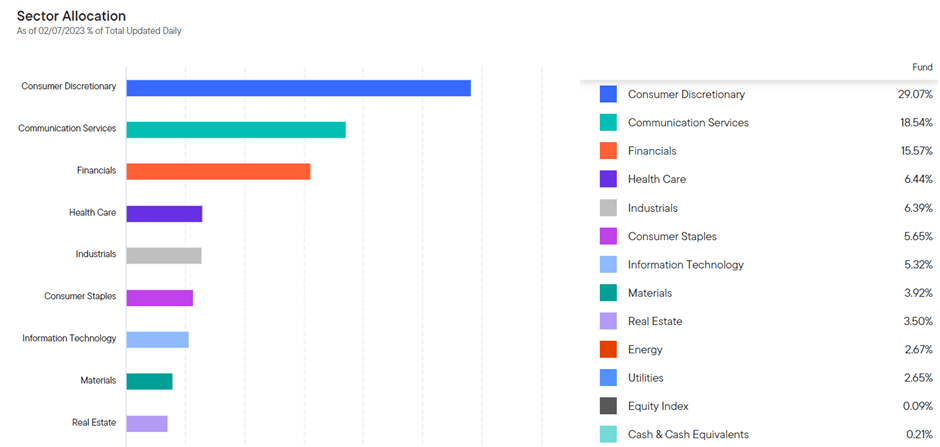

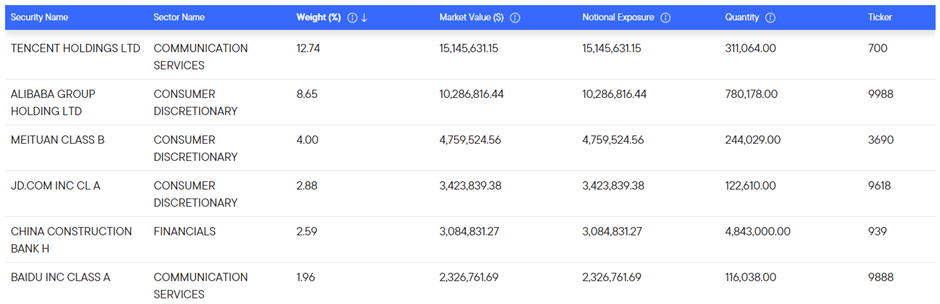

As reflected in the chart below, the fund’s sector allocation skews toward the consumer discretionary (29.1%), communication services (18.5%), and financials (15.6%) sectors, which accounted for a combined 63.2% of the total portfolio. The fund’s largest holdings are Chinese tech and entertainment giant Tencent Holdings (OTCPK:TCEHY) (12.7%), Chinese e-commerce leader Alibaba Group (BABA) (8.7%), Chinese shopping platform Meituan (OTCPK:MPNGF) (4.0%), and e-commerce giant JD.com (JD) (2.9%).

Franklin Templeton

The portfolio is composed of 971 holdings, and while the top ten holdings account for ~39% of the overall portfolio, this is still one of the more diversified Chinese ETFs in the market. Another notable difference is the inclusion of communication services players like Tencent, Baidu (BIDU), and Weibo (WB) – as these stocks have been dropped from many other indices/ETFs on ESG concerns, their inclusion in the Franklin FTSE China ETF offers ESG-agnostic investors a welcome alternative. Finally, the ETF is primarily made up of H/A shares, so investors concerned about ADR risks may prefer China exposure via FLCH.

Franklin Templeton

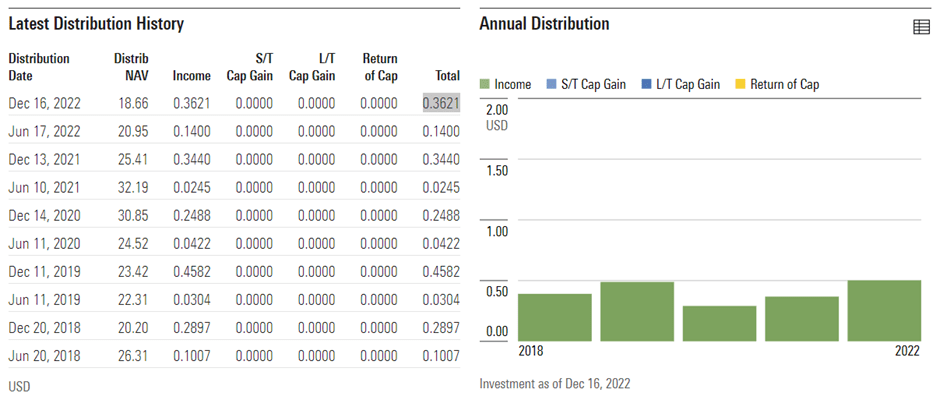

On a YTD basis, the ETF has returned 8.2% but has declined by 18.7% since its inception in 2017. Income dividends are paid out on a semi-annual basis; thus far, the fund has distributed $0.50/share for 2022 out of income, implying a ~2.4% trailing yield. This might seem low, but it’s important to bear in mind the fund’s outsized exposure to high-growth tech and consumer names, which generally reinvest excess cash (vs. paying out as dividends). Thus, FLCH is a better fit for growth-focused investors who view the relatively low yield as a bonus, in my view. Investors looking for China exposure, along with a steady income stream, might want to look at a financial-focused ETF like the Global X China Financials ETF (CHIX) instead (see my prior CHIX coverage here).

Morningstar

Levered to the Chinese Consumer Recovery

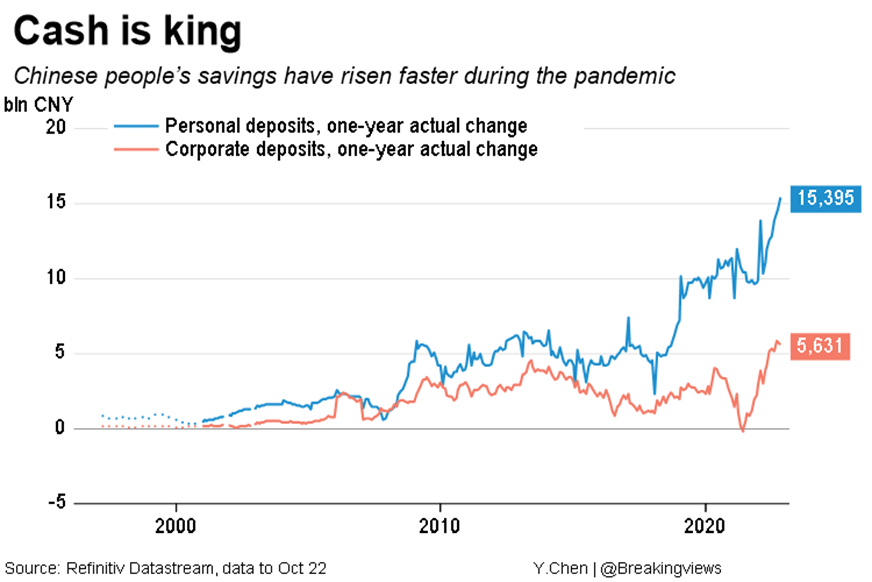

Having lagged in the COVID-impacted years, consumption is finally poised for a rebound, with a gradual return to pre-COVID levels possibly on the cards as soon as 2023. The key question is how the ‘revenge spending’ theme plays out – high-frequency data coming out of the Lunar New Year indicates pent-up demand for activities previously most impacted by restrictions (e.g., travel) should lead the consumer spending snap back, along with the broader services sector. Also, worth monitoring is the pace at which households draw down the excess savings accrued through the ‘zero-COVID’ years.

Reuters

Beyond the near term, a consumption-driven economic recovery should have substantial second-order effects via higher employment and income levels, in turn driving a positive feedback loop around income and consumption. Going forward, expect retail sales to grow in the double-digits % YoY and consumption to return as a key headline GDP growth driver this year before normalizing well above the levels seen during the COVID-impacted years. Given FLCH’s outsized exposure to this theme (note four of its top-five holdings are consumer/consumer-related businesses) and the significant discount Chinese consumer names like BABA still trade relative to pre-COVID levels, expect higher earnings revisions to extend the YTD rally.

Return of the Policy Put Paves the Way for More Upside

In conjunction with the ‘zero-COVID’ policy pivot in late 2022, Chinese policymakers have followed up with a series of measures aimed at stabilizing the economy. These include support for the troubled property sector, for instance, via relaxed funding restrictions for developers, along with a looser policy for buyers (e.g., easing of purchase restrictions) to shore up the demand side as well. In effect, the return of a policy ‘put’ caps further downside risk to the Chinese property/housing market as the economy reopens.

A stabilized property sector is key – only after minimizing systemic risks will Beijing have a clear path to introducing major fiscal stimulus measures (potentially infrastructure and manufacturing investments), building on the PBoC’s ongoing monetary easing. Commentary from recent policy meetings, including the Politburo meeting and Central Economic Work Conference (CEWC), also leaned toward a pro-growth stance for 2023. And with the new economic team set to take over in March, expect accelerated policy momentum as they look to start off strongly.

An Ultra-Low-Cost Vehicle to Play the China Recovery

Within the US-listed China ETF universe, FLCH should be right at the top of investor shortlists. The fund comes with an ultra-low expense ratio at ~0.2% and a decent >2% distribution yield, while the outsized exposure to the Chinese consumer (via discretionary, staples, and communication services) leaves the fund well-positioned to ride a consumption-led recovery.

Market sentiment has shifted, as reflected in the YTD appreciation in FLCH and similar Chinese ETFs, but with the reopening progressing well ahead of expectations (as evidenced by the busy Lunar New Year travel season), the rally still has legs, in my view. Plus, the Chinese policy ‘put’ offers additional support, now leaning more toward economic growth and stabilization (e.g., the ongoing balance sheet repair in property). And with a new economic team coming into office next month, expect more positive catalysts on the horizon.

Net, China equities stand to benefit from a unique combination of tailwinds that should keep earnings and the RMB up for the year; consumer-focused Chinese funds like FLCH and CHIQ are compelling areas to allocate capital, in my view.

Be the first to comment