buzbuzzer

Over the last couple years, I started buying several real estate investment trusts (“REITs”) for my Roth IRA. I like the income focus of the sector, and the long term returns for investors have proven to be attractive. If you can narrow your focus to the best opportunities in REITs, returns can be even better.

I have bought positions in several different REIT sectors, from cell towers, net lease, and even cannabis REITs. As an investor with limited capital and a dislike for exchange-traded funds (“ETFs”), I had to narrow things down to what I viewed as the best options at the time. One of the REITs that I passed on is Federal Realty Investment Trust (NYSE:FRT). While the REIT is a dividend king, I found some of the alternatives to be more attractive.

Investment Thesis

Federal Realty Trust is one of the oldest REITs around, and it has earned the coveted dividend king title, with 54 years of consecutive dividend hikes. Like most the public markets, shares of FRT have struggled in 2022 and are down nearly 30% YTD. This might lead some investors to think that now is a good time to start a position or add to one, but there are a couple factors that have kept me on the sidelines.

The first is the valuation, which is cheaper now, but at 16.7x price/FFO, it still doesn’t leave a huge margin of safety. The other factor is the slowing dividend growth, which is one of the main things I look for with REITs. Shares now yield 4.4%, but I don’t think investors will see double digit returns from here without significant multiple expansion.

Overview

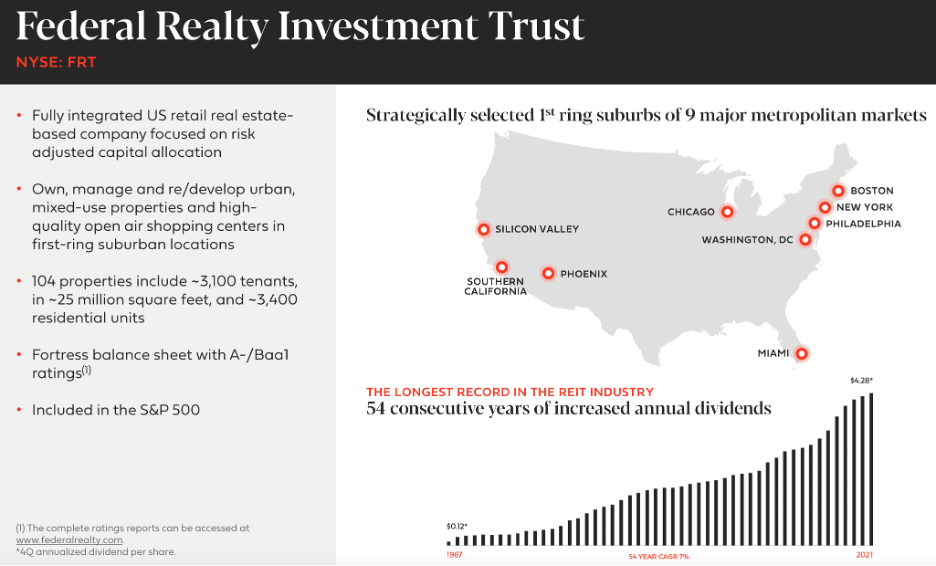

FRT is a mixed-use REIT that focuses on the suburban areas of major cities across the US. They target wealthy areas and have an interesting rent mix, including residential, office, restaurants, and other retail property types. FRT has a market cap of $7.7B and has an impressive string of dividend hikes, with 54 annual dividend increases.

FRT Overview (federalrealty.com)

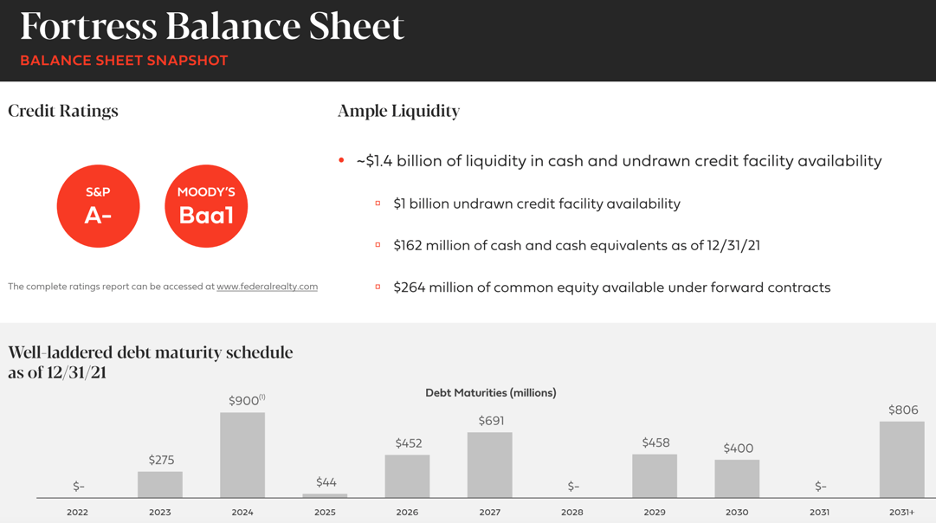

FRT also maintains a solid balance sheet with plenty of liquidity and well laddered debt maturities. The debt is a mix of mortgage notes and senior unsecured debt, most of which carries interest rates below the current rate of inflation. They have notes that are due more than two decades from now, which shows that the smart money in the bond market is willing to lend to FRT for a long time at low interest rates.

FRT Debt Ladder (federalrealty.com)

As you can see, FRT doesn’t have a bunch of debt coming due all at once, and they should be able to issue debt in the future at attractive rates. While most of the article so far is reason enough to be bullish, one of the reasons that I didn’t purchase shares of FRT is the valuation.

Valuation

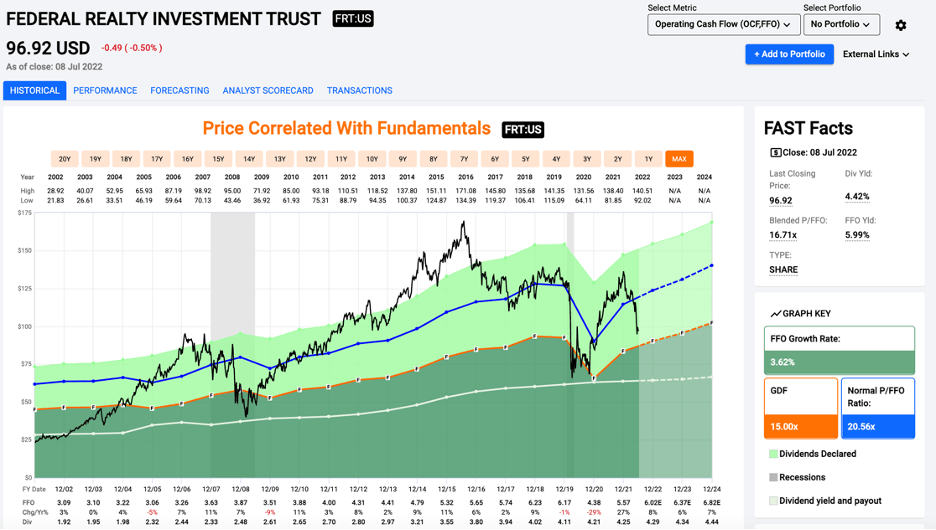

FRT has had a rough start to 2022, like most of the market outside of the energy sector. Shares are down nearly 30% YTD, which certainly offers a better entry point than the start of the year. Shares now trade at 16.7 price/FFO, which is below the average 20.6x multiple of the last two decades.

Price/FFO (fastgraphs.com)

Bullish investors might be expecting a return to a 20x multiple (or higher), which would certainly lead to attractive returns. However, I’m not willing to bet on it, which is why I currently have no position. While the valuation isn’t that compelling for new investors in my opinion, the slowing dividend growth is the other reason that I have stayed away from FRT.

Slowing Dividend Growth

FRT currently yields 4.4%, which is a solid dividend in today’s market environment. They also have a 54-year track record of dividend hikes, so it is safe to assume that the dividend raises should continue for years to come. However, the slowing dividend growth is the other primary reason that I have stayed on the sidelines. In the last 5 years, they have only raised the quarterly dividend 7 cents, from $1.00 to $1.07. The dividend hikes will likely continue, but I don’t see the dividend growth accelerating from here.

Conclusion

If your priority is safe current income with a high probability of continued increases, FRT might be an intriguing option for you. The company certainly has an impressive asset portfolio in attractive markets with high barriers to entry.

However, I don’t think the valuation is all that attractive right now at 16.7x price/FFO. Multiple expansion is possible, but I think it is unlikely with the growth profile of FRT. The other problem is the slowing dividend growth. While 54 straight dividend hikes is impressive, the recent growth hasn’t been much to get excited about, even with a 4.4% yield.

If shares continue to drop, the valuation might get to a point where the margin of safety is larger and forward returns better, but I think there are better risk/reward profiles available to REIT investors today. Shares are a hold right now in my book, but that could change in the coming months depending on what happens with the share price.

Be the first to comment