Koichi Kamoshida/Getty Images News

Electronic Arts is a leading game publisher which has licenses to a widely popular list of iconic sporting franchises from FIFA Soccer to the NFL. The company reported a record launch of its new FIFA 23 game, and I forecast more organic sales to be driven by the excitement surrounding the World Cup, which has recently concluded. In addition, the company has beaten earnings estimates for growth, despite a tepid gaming environment overall. In this I’m going to break down its business model, financials, and valuation, let’s dive in.

Business Model

Electronic Arts (NASDAQ:EA) is an international video game company that designs and publishes a range of iconic games. Its most popular gaming franchises include NBA, Madden NFL, UFC, and FIFA in the sporting industry. Similar to owning the television rights to sports franchises, the “moat” of Electronic Arts, is its ownership/license of these sports franchises. It is pretty difficult, for competitors to create another basketball or soccer game that sells as well as the NBA games or FIFA. In addition, Electronic Arts created the iconic Sims games, Apex Legends, Need for Speed, Battlefield, and even Star Wars games. As a “recovering” gamer I was brought up playing many of these iconic games and still remember the popular slogan, “EA Sports…it’s in the game”, which is a testament to the strong brand. The popular cloud gaming distributor “Steam”, reported Apex Legends by EA was a “platinum” game in 2022. This means it was one of the best-selling games on the platform. EA has a player network of over 600 million people, which is astonishing.

EA Games (Electronic Arts)

EA develops games for all platforms including console, mobile, and PC. The company makes its revenue through a combination of game sales and “microtransactions” for in-game content and features. EA also has a popular subscription service called EA Play and EA Play Pro, which offers players a vast library of games and loyalty-based discounts. In addition, EA generates revenue from its licensing and sales of merchandise such as hats and t-shirts. EA management mentioned in its earnings call that 3 out of 4 players engage with gaming content “beyond the game itself”. This includes reading, commenting, creating content, and much more. I believe this close-knit and engaged community is another powerful part of the business.

Mixed Financials

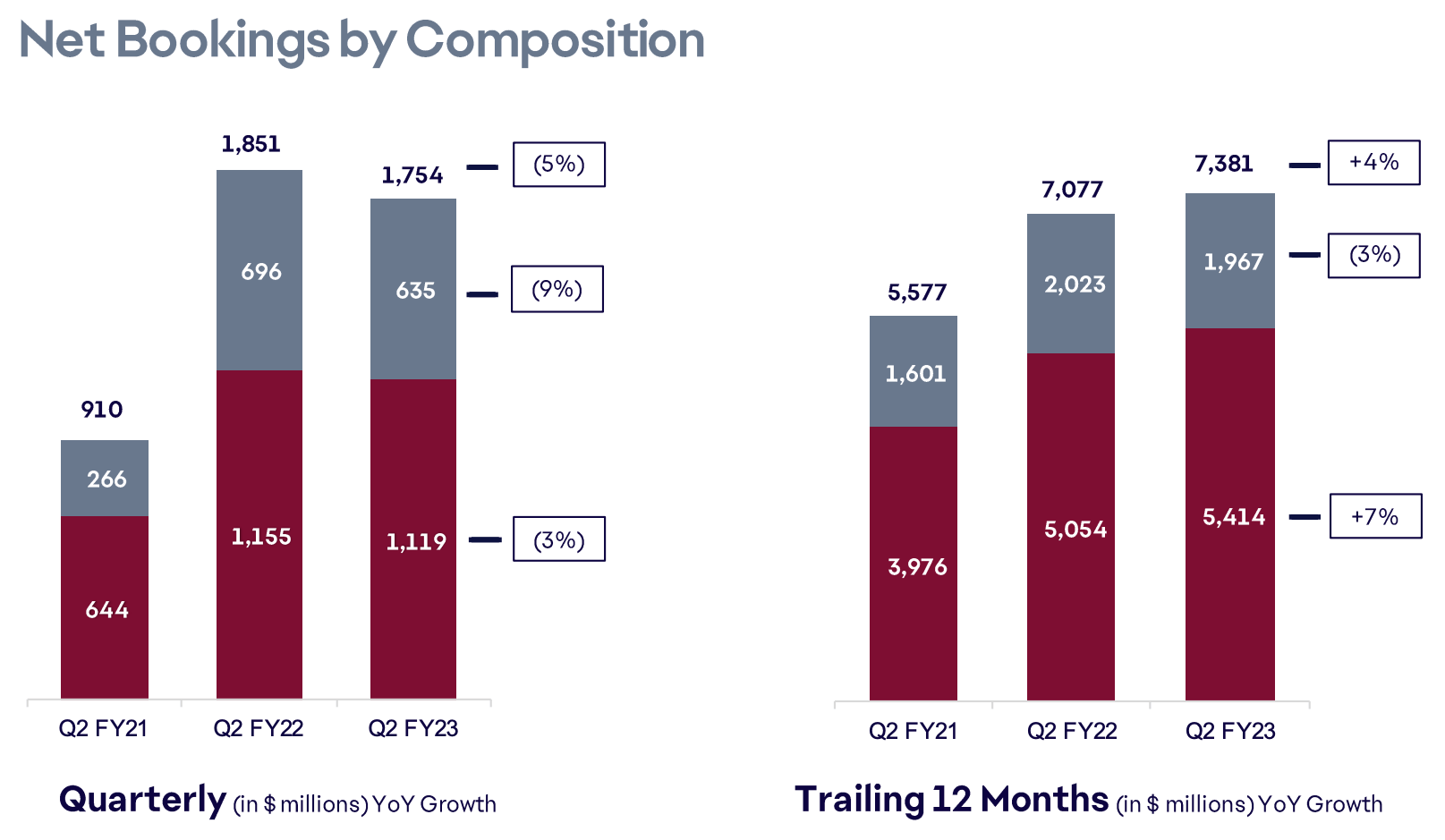

Electronic Arts reported mixed financial results for the second quarter of fiscal year 2023. The company reports using a specialist metric called “Net Bookings”. This is the “net amount” of products sold both virtually and physically. In this case, we can think of it as akin to revenue. Net Bookings were $1.75 billion, which was down 5% year over year, but up 2% on a constant currency basis. Despite the seemingly underwhelming results, management was surprisingly upbeat in their earnings call and stated these results were “in line” with their expectations. The positive is on a trailing 12-month basis Net Bookings increased by 4% year over year. The grey bar below represents “full game sales”, which decreased by 9% year over year in Q2, FY23. The red bar represents live and other services, which declined by a less amount (3%) to $1.119 billion. On a constant currency basis, this was flat year over year and again in line with management’s estimates.

Net Bookings by Composition (Electronic Arts Q2, FY23 report)

The highlight of Electronic Art’s business results was its EA Sports portfolio which showed strength. Its FIFA soccer or “football” franchise reported record results with the launch of FIFA 2023. This game generated unit sales which were up 10%, compared to the launch of FIFA 2022. The company also reported record engagement with monthly active players up 100% year over year. In addition, its free to play FIFA online service in Asia reported record results.

I believe Electronic Arts timed the launch of FIFA 23, particularly well given the World Cup started just a couple of months later in November 2022. The World Cup is one of the biggest sporting events in the world with over half the world’s population, ~3.5 billion people reportedly watching past events. As the World Cup is every four years, this makes it even more special and FIFA reported “record” TV viewing at the 2022 world cup. The result of such a huge event on sales will not show up in the second quarter FY23 results, thus I am predicting a monster third quarter, FY23 (Q4 calendar year), driven by the FIFA soccer franchise and also Christmas. Electronic Arts even updated the FIFA 23 game with special World Cup content to entice fans throughout the tournament, which further boosted engagement.

Electronic Arts is investing massively into building out its Soccer franchise with an increasing focus building community and experiences. Its EA Sports FC plans to be the “future of interactive football” and will be more independent than the FIFA franchise. This will likely offer much greater opportunities and likely higher margins than its FIFA version of the game. I suspect EA is using the momentum of the World Cup as an opportunity to launch this new game.

Back to the second quarter FY23, Madden NFL 2023, launched in August 2022 and reported “double-digit” net bookings. In addition, the company announced new partnerships with Marvel and Disney for a range of new titles such as those in the Star Wars franchise.

EA Live Games (Q2, FY23 report)

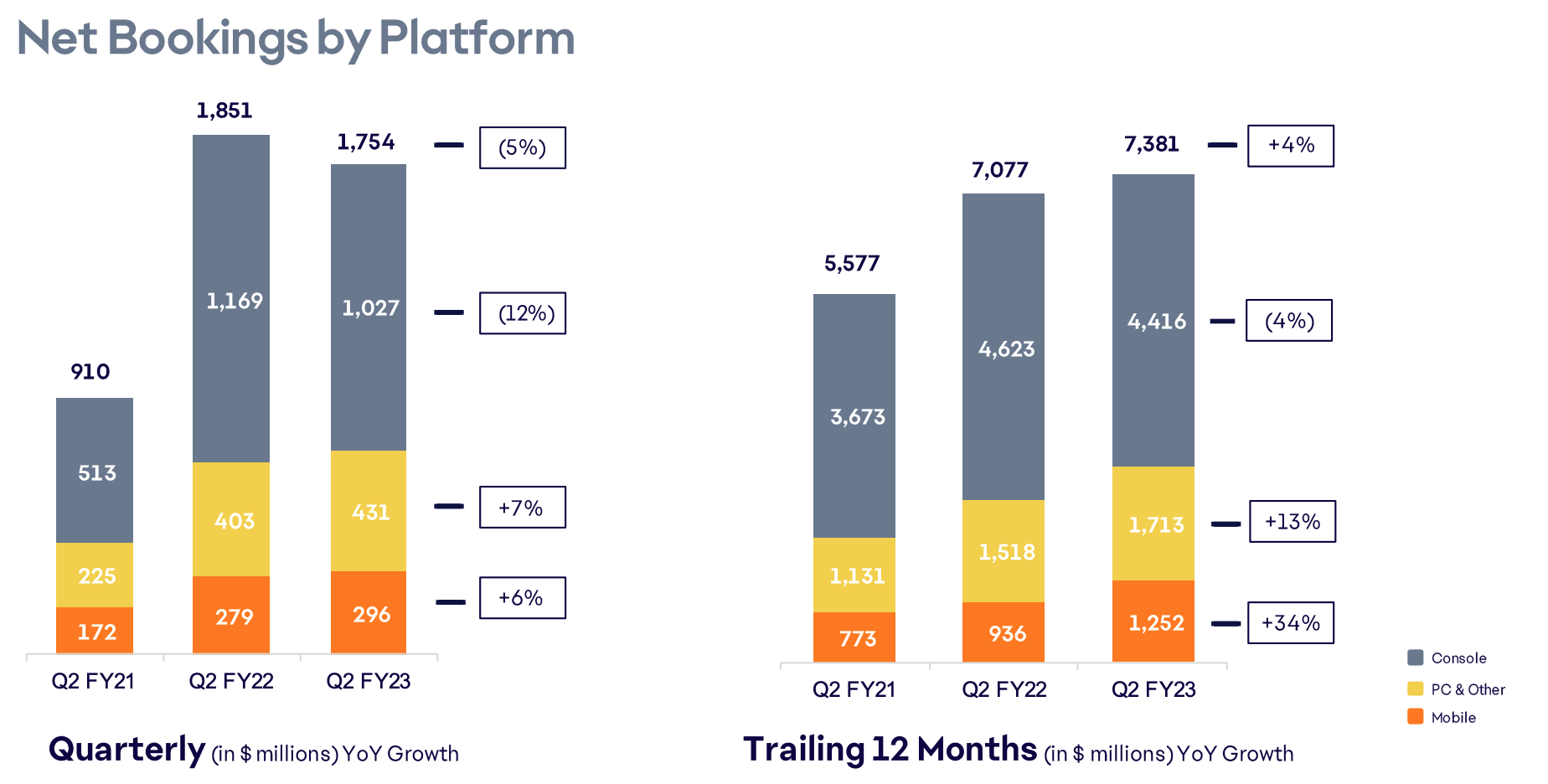

Breaking Bookings down by platform, the company reported strong growth in the PC market, which increased revenue by 7% year over year to $431 million. In addition, the mobile market increased by a 6% year over year to $296 million. Console game bookings did report a 12% decline but this was expected given the cyclical decline in the gaming market.

Bookings by Platform (Q2,FY23)

Electronic Arts reported that Gen Z and Gen Alpha are increasingly turning to gaming as a form of social connection. This was a trend that was heightened during the lockdown of 2022, and I expect this to continue.

Profitability and Cash Flow

Electronic Arts reported earnings per share [EPS] of $1.07, which beat analyst estimates by $0.07 and increased by 4.26% year over year. Operating expenses only rose by 2% year over year, which was a positive given the high inflation environment. EA reported operating cash flow of negative $112 million, this was worse than the $64 million reported in the same quarter last year. However, it should be noted this included a substantial $378 million in buybacks and dividends. EA has a strong balance sheet with $1.874 billion in cash and short-term investments. The company does have fairly high debt of $2.2 billion, but the vast majority of this $1.879 billion is long-term debt.

Cash Flow (Q2,FY23)

Moving forward management has forecast full-year net bookings of between $7.65 billion to $7.85 billion, up 2% to 4% year over year or 6% to 9% on a constant currency basis. The company is expecting a $200 million headwind from foreign exchange rates as over half of its revenue is derived from outside of the U.S. A positive is the company raised its GAAP earnings per share guidance to between $3.11 to $3.34.

Advanced Valuation

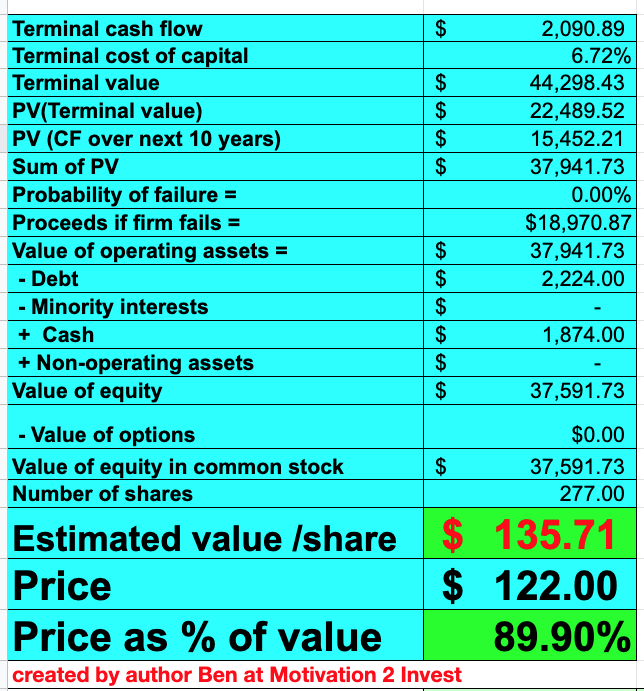

I have plugged the latest financial data into my discounted cash flow model to value, Electronic Arts. In this case, I have forecast 7% revenue growth for “next year”, which includes the next couple of quarters in the valuation model. I forecast this to be driven by a combination of FIFA world cup tailwinds, but with a headwind from unfavorable foreign exchange rates. In years 2 to 5, I have forecast a faster growth rate of 9%, driven by an overall improvement in the cyclical gaming market, especially console games.

Electronic Arts stock valuation 1 (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation, I have capitalized R&D expenses, which has lifted the operating margin substantially. I have forecast a further 3% growth in operating margin over the next 8 years, driven by the increased community, engagement, and return on gaming investments.

Electronic Arts stock valuation 2 (Created by author)

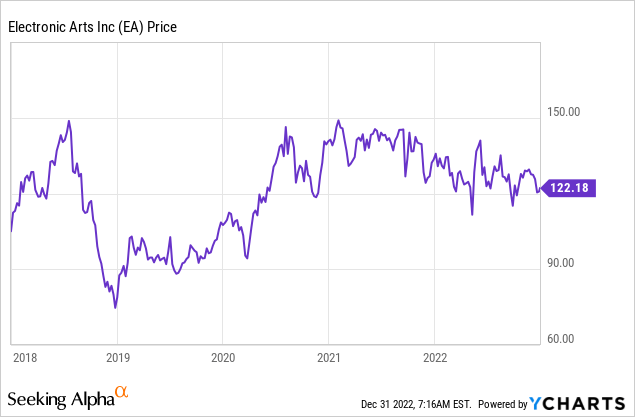

Given these factors I get a fair value of $135.71 per share, the stock is trading at $122 per share at the time of writing and is thus over 10% undervalued.

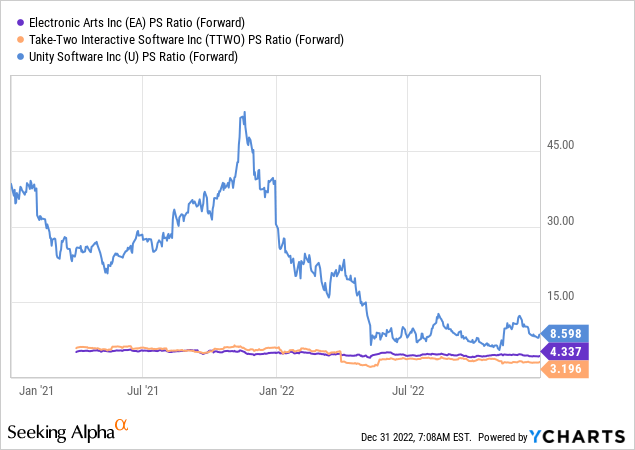

As an extra datapoint, Electronic Arts trades at a Price to Sales ratio = 4.71, which is 25% cheaper than its 5-year average. Relative to other gaming companies (shown below) Electronic Arts is trading at a mid-range valuation.

Risks

Recession/Cyclical Gaming demand

Many analysts have forecast a recession, which will likely reduce the number of overall game sales and in-game purchases. In addition, the gaming market is currently going through a lower engagement period. The positive is both the economy and the gaming market tend to be cyclical.

Final Thoughts

Electronic Arts is a fantastic gaming company that has a range of iconic franchises. Its sporting brands are particularly strong and its exclusive partnerships with sports teams give the company a strong moat. I forecast Electronic Arts to benefit from World Cup tailwinds, which will likely drive higher FIFA game sales. In addition, its stock is undervalued intrinsically and relative to history, thus it looks to be a great long-term investment.

Be the first to comment