Dimitrios Kambouris/Getty Images Entertainment

Microsoft (NASDAQ:MSFT) is a stock that I held through the 2020/2021 NASDAQ rally and managed to sell before it came crashing down. I bought it after reading about the company’s success with Azure-the second fastest growing of the big tech cloud services. Alphabet’s (GOOG) Google Cloud was growing faster than Microsoft’s Azure at the time (54% vs. 42%), but Azure was profitable while Google Cloud wasn’t. So I figured that MSFT was the safer cloud bet.

When I bought MSFT, I was pretty much betting on Azure. When researching the stock, I discovered that its revenue growth in non-cloud businesses was slow, and that its valuation was expensive. Today, Microsoft only trades at 26.5 times earnings, but it was above 30 around the time I sold it. It has a sky-high 11.4 price-to-book ratio to this day.

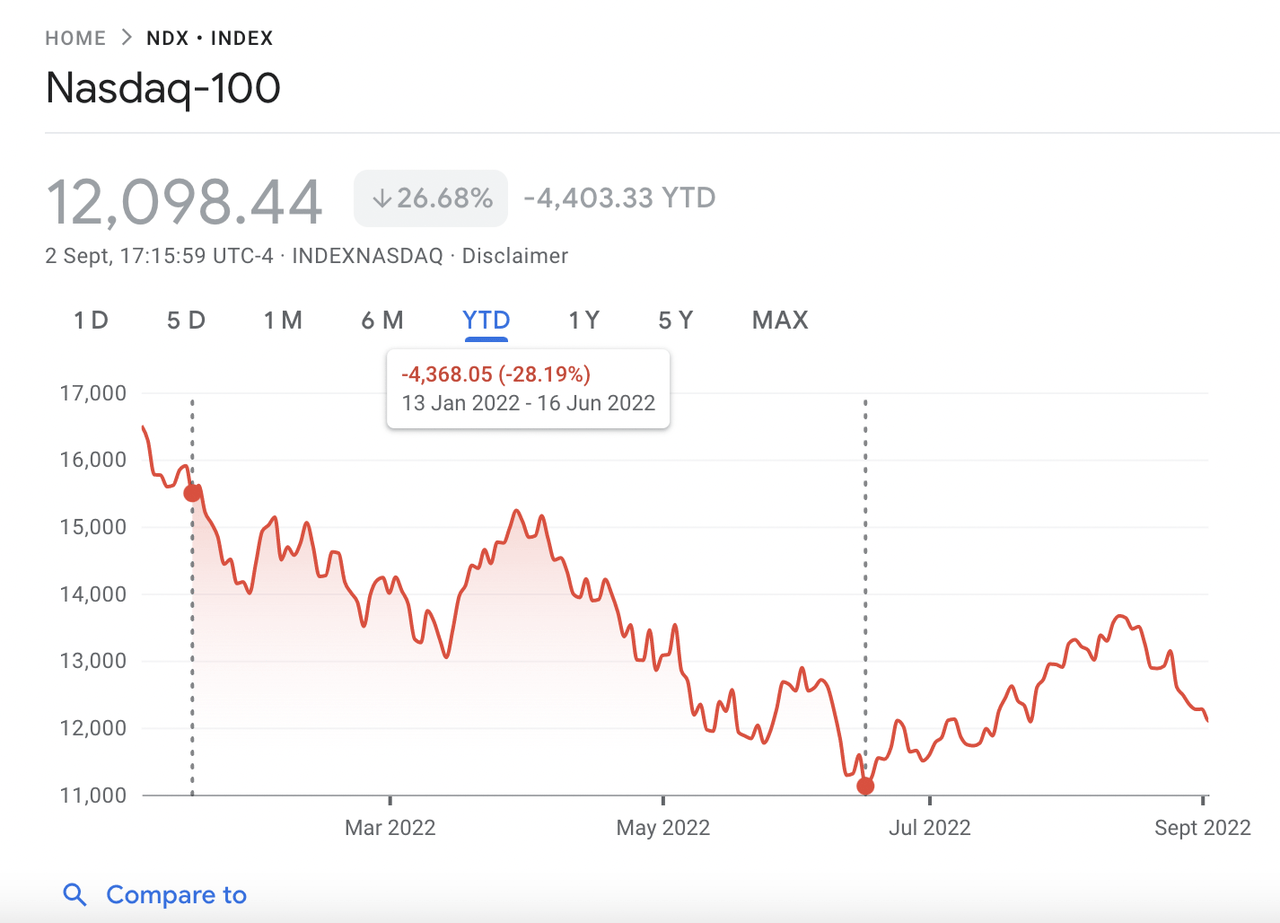

Around the end of 2021 I knew that the Federal Reserve was planning on hiking interest rates, so I sold the two most expensive stocks in my portfolio: MSFT and Adobe (ADBE). The timing on those sales was pretty good because I booked gains on both (33% on MSFT and 20% on ADBE), while limiting my exposure to the tech bear market. Shortly after these sales, I wrote the article “The Tech Stock Crash Will Likely Get Worse,” which explained my reasons for being bearish on tech stocks. After the article published, the NASDAQ-100 fell a further 28%.

NASDAQ trading after I predicted a tech crash (Google Finance)

Initially, I invested the proceeds I got from selling Microsoft into classic value plays: banks and energy stocks. I figured that rising interest rates would help banks earn more money while the economic recovery from COVID-19 would boost energy stocks. I was only half right about the first part (rising interest rates helped retail banks but not investment banks), I was 100% correct about the second part. At any rate, I booked some small profits on energy stocks and didn’t buy anything new for a while after that.

Later, though, I started thinking about getting into tech stocks again. After watching the NASDAQ-100 tumble, I noticed that valuations were getting cheap. In particular, I noticed that Google had gone all the way down to 20 times earnings, despite still having double digit revenue growth, while Apple was gaining market share in China. Apple was on the pricey side at that point, but not as much as Microsoft (it traded at around 24 times earnings). So, I added some GOOGL and AAPL-the former stock has fallen about as much as Microsoft, the latter has given me a gain.

None of this is to say that I’m actively bearish on Microsoft. I still hold the Invesco QQQ Trust (QQQ), which has a high level of MSFT exposure. However, factoring in price, competitive dynamics, and growth, I find Google and Apple to be better bets. In the ensuing paragraphs, I’ll explain why I think that way.

Competitive Landscape

One area where Google and Apple both have an edge over Microsoft is competitive dynamics. Google and Apple both have wide moats, Microsoft’s position relative to competitors is less robust.

First, we can look at Google’s moat. It’s the #1 online ad platform in the world, with 26.4% of the market. In second place after Google is Meta Platforms (META), which has gained at Google’s expense over the last decade, but is experiencing issues this year due to Apple’s privacy changes and competition from TikTok. We can expect Google’s moat to persist, because it benefitted from the very same Apple policy changes that hurt Meta, proving it has a resilient model competitors can’t touch.

Next, we can look at Apple’s moat. This stems from its brand (the most valuable in the world), which helps it retain customers, and its interconnected ecosystem, which encourages customers to buy multiple products. Apple has a huge fan community on YouTube, which helps it sell products without extra ad spend. As a result, Apple is #1 or #2 across multiple product categories, including:

So we can see that Google and Apple both have high market share. Additionally, they have factors that can lead us to infer continued high market share-brand loyalty in Apple’s case, a resilient ad platform in Google’s case.

As for Microsoft?

It has some of the advantages that Apple and Google have, but not to the same extent. It controls Windows, the most popular computer operating system, but that product category has plateaued. It no longer has a meaningful presence in smartphones, as it failed in that market. In cloud services, it is #2 after Amazon. Finally, in gaming, it’s second in hardware sales to Sony’s (SONY) PlayStation 5, and owns the popular Minecraft IP. Microsoft has a pretty good competitive position, but it is not the #1 player in any growth sectors the way Apple and Google are.

Comparative Valuation

Having looked at Microsoft’s competitive position, we can now turn to its valuation. MSFT remains a pretty expensive stock well into the 2022 bear market, and it may continue to be expensive for a while. To illustrate this fact, we can compare Microsoft’s earnings multiples with those of Apple and Google.

|

MSFT |

AAPL |

GOOG |

|

|

Price/earnings |

26.5 |

25.5 |

20 |

|

Price/sales |

9.7 |

6.57 |

5.13 |

|

Price/book |

8.18 |

43 |

5.5 |

|

Price/cash flow |

21.45 |

21 |

14 |

As you can see, Apple is pretty similar to Microsoft, while Google is far cheaper. Valuation favors Google, it does not favor Apple, but recall the previous section on the competitive landscape: Apple’s high brand loyalty makes it a very reliable company. It is not under any threat of margin compression due to new competitors entering the market, Microsoft arguably is.

As for Microsoft’s valuation in a discounted cash flow model: it’s hard to forecast the cash flows of a company with as many moving pieces as MSFT. However, if we start with the last 12 months’ $8.69 in free cash flow per share, and assume that it grows at the 10-year CAGR rate of 7.7%, we get to $12.59 in FCF per share after five years. Using a 3.25% discount rate (the current treasury yield), and assuming that growth falls to zero after five years, we get a present value of $379. That’s a significant amount of upside, but remember that DCF models are very sensitive to inputs. Change the discount rate to 8% and suddenly the fair value falls to $150, which is severe downside. If you run this same model swapping out Microsoft’s free cash flow for Google’s, you get a fair value of $215, which implies 2X upside. Google also ends up worth less than today’s price if you raise the discount rate to 8%, but the amount of downside (about 20%) is less.

Microsoft’s Earnings

As I showed above, Microsoft has a steeper valuation than other tech companies you can compare it to. However, it has some advantages that other tech companies don’t have. For example, it’s still growing. In its most recent quarter, MSFT managed to achieve positive top and bottom line growth, posting the following results:

-

Revenue: $51.9 billion, up 12%.

-

Operating income: $20.5 billion, up 14%.

-

Net income: $16.7 billion, up 2%.

-

Diluted EPS: $2.23, up 3%.

Like many companies in the same period, Microsoft achieved solid revenue growth in Q2; however, unlike those other companies, it also had positive earnings growth. For a tech company to still be growing in 2022 after the Fed’s many rate hikes and Apple’s privacy changes is impressive. However, note that:

-

Google’s Q2 top line growth was higher than Microsoft’s, at 13%.

-

Apple is doing a major product launch today that could boost its sales.

Certainly, Microsoft is a good company. But when you look at Google’s wider moat and Apple’s potential catalyst, both of these stocks look like better opportunities.

Risks and Challenges

As I’ve shown in this article, Microsoft is a good stock, but perhaps not the best in the tech sector. I personally think Apple and Google are more appealing. However, there are risks and challenges facing any investor who chooses to overweight Google and Apple at the expense of Microsoft, including:

-

Concentration risk. All investors are exposed to two types of risk: market risk and specific risk. Market risk is the risk inherent in the whole market, specific risk is the risk in any one stock. The more you diversify, the less your specific risk. A broadly diversified portfolio with thousands of stocks reduces your specific risk to near zero. When you increase your specific risk by holding a lower number of stocks, your total portfolio is said to have ‘concentration risk.’ If you’re considering investing in just tech stocks, a full ‘FAANG’ portfolio that includes MSFT, AAPL, GOOGL and the rest of the NASDAQ-100 will have less concentration risk than a pure Apple/Google portfolio. It would still be exposed to market risk, but its overall risk would be lower than holding just Apple and Google.

-

A slowdown in consumer spending. Despite the current economic contraction, consumer spending is still rising modestly. In this environment, there are plenty of people buying Apple products, and patronizing companies that advertise on Google. If we enter a full fledged recession, though, that will likely change. As economic activity dips, people start to worry about being laid off-they often cut their spending as a result. Should something like that happen, an enterprise-focused company like MSFT might fare better than Google and Apple, which are heavily invested in the consumer.

The risks above are worth keeping in mind. If they concern you, then Invesco’s QQQ ETF might suit you better than a concentrated Apple/Google bet. Nevertheless, it’s hard not to notice that Google and Apple enjoy competitive advantages over Microsoft. That reason alone is enough for me to weight the former two stocks higher than the latter.

Be the first to comment