DNY59

Earnings of Eastern Bankshares, Inc. (NASDAQ:EBC) will likely continue to surge through the end of 2023 mostly on the back of decent loan growth. Further, the margin will react positively to a rising rate environment, which will lift earnings. On the other hand, higher provisioning expenses will restrict the bottom-line growth. Overall, I’m expecting Eastern Bankshares to report earnings of $1.39 per share for 2022, up 54% year-over-year. Compared to my last report on the company, I’ve revised upwards my earnings estimate because I’ve tweaked upwards my net interest income estimate. For 2023, I’m expecting earnings to grow by a further 16% to $1.60 per share. The year-end target price is quite close to the current market price. Therefore, I’m maintaining a hold rating on Eastern Bankshares.

Loan Growth To Decelerate

After the first quarter’s disappointing performance, the loan book grew by an impressive 1.8% in the second quarter of 2022. I’m expecting loan growth to slow down in the second half of this year because of heightened interest rates.

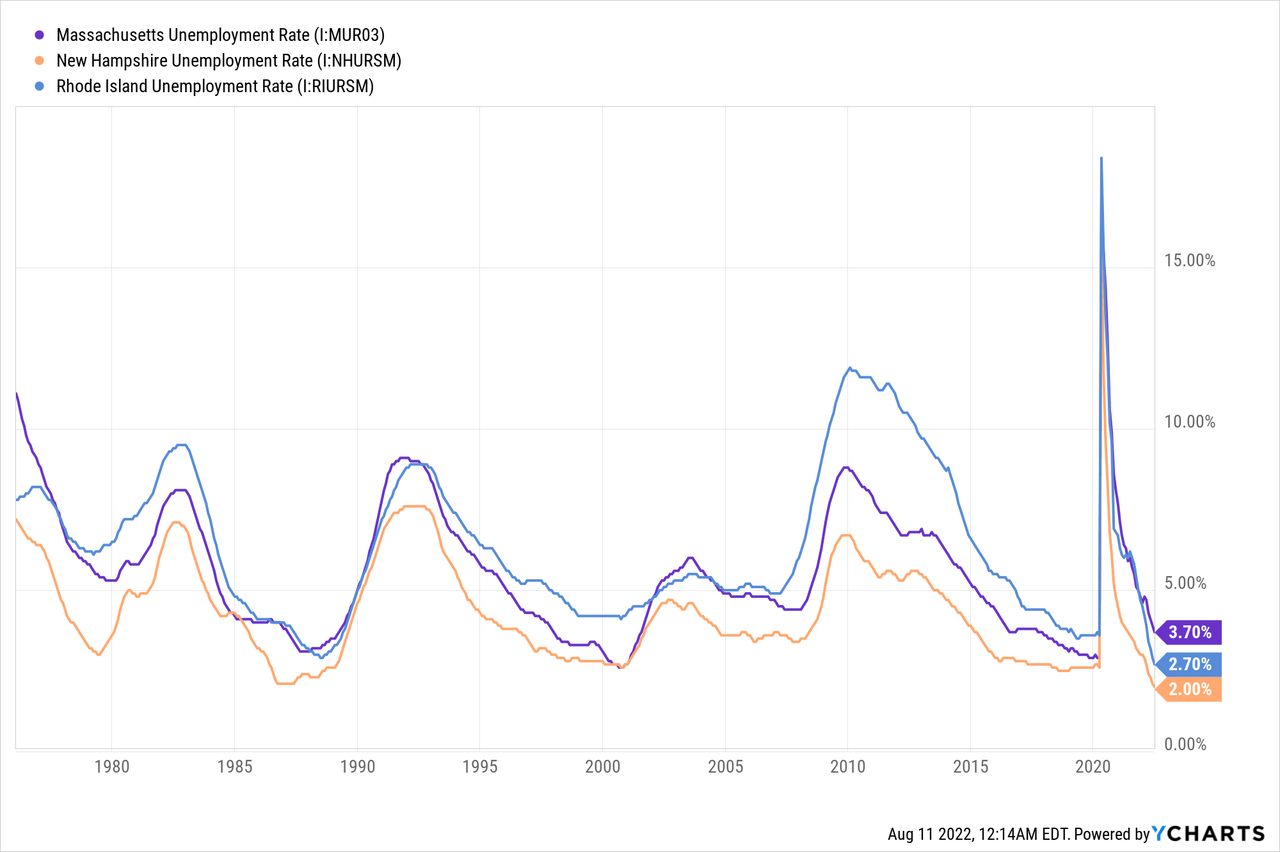

On the other hand, strong job markets will likely support loan growth in the quarters ahead. Eastern Bankshares operates in Massachusetts, Rhode Island, and New Hampshire. Both Rhode Island and New Hampshire have unemployment rates that are lower than the national average. Further, all three states have very strong job markets from a historical perspective.

The management also appeared optimistic about loan growth during the latest conference call. The management expects commercial loan growth to be in the mid-to-high-single digit range. Considering these factors, I’m expecting the loan book to grow by 3.0% in the second half of 2022, leading to full-year loan growth of 3.8% from the end of December 2021 to the end of 2022. However, the average loan balance for 2022 would be much higher than 2021 because of the acquisition of Century Bancorp in November 2021.

In my last report on Eastern Bankshares, I estimated loan growth of 2.0% for 2022. I’ve revised upwards my loan growth estimate mostly because of the second quarter’s surprising performance.

Higher Rates To Erode Equity Book Value

The growth of other balance sheet items will most probably lag loan growth this year. Due to a large balance of available-for-sale debt securities, the equity book value stands to take a hit from the rising-rate environment. An increase in interest rates will lower the value of the investment securities portfolio. This loss will flow directly into equity bypassing the income statement.

The book value per share has already declined from $18.28 at the end of December 2021 to $15.17 at the end of June 2022. The book value per share will likely dip even further because I’m expecting the Federal Reserve to hike the fed funds rate by another 75 basis points this year before reducing rates in mid-2023.

The following table shows my balance sheet estimates.

| FY19 | FY20 | FY21 | FY22E | FY23E | ||||

| Financial Position | ||||||||

| Net Loans | 8,899 | 9,594 | 12,157 | 12,622 | 13,135 | |||

| Growth of Net Loans | NA | 7.8% | 26.7% | 3.8% | 4.1% | |||

| Other Earning Assets | 1,736 | 5,122 | 9,600 | 8,295 | 8,632 | |||

| Deposits | 9,551 | 12,156 | 19,628 | 19,452 | 20,242 | |||

| Borrowings and Sub-Debt | 235 | 28 | 34 | 43 | 45 | |||

| Common equity | 1,600 | 3,428 | 3,406 | 2,813 | 3,039 | |||

| Book Value Per Share ($) | NA | 18.4 | 18.2 | 15.1 | 16.3 | |||

| Tangible BVPS ($) | NA | 16.3 | 14.8 | 11.6 | 12.8 | |||

| Source: SEC Filings, Author’s Estimates | ||||||||

| (In USD million, unless otherwise specified) | ||||||||

Deposit Mix, Securities Portfolio To Limit The Margin’s Rate-Sensitivity

The loan book is quite rate-sensitive as it is concentrated in floating-rate loans. As mentioned in the second quarter’s earnings presentation, around 39% of the loan book will re-price within only 30 days of a rate hike. The deposit book is also quite rate-sensitive as it is heavy on interest-bearing, savings, and money-market accounts. These rate-sensitive deposits made up 63% of total deposits at the end of June 2022. However, the magnitude of the loan book sensitivity is higher than the sensitivity of the deposit book. This is because the bank has greater pricing power when it comes to deposits due to the excess liquidity of depositors. However, as depositors shift more and more of their deposits into treasury securities to get good yields, this pricing power may diminish.

The large balance of available-for-sale debt securities will limit interest income growth amid a rising-rate environment. Securities made up a hefty 34% of total assets at the end of June 2022. Further, this portfolio has a long duration of 4.9 years, as mentioned in the presentation. Therefore, only a small part of the portfolio can be expected to mature and roll over into higher-yielding assets this year.

The results of the management’s interest-rate sensitivity analysis given in the 10-Q filing show that the net interest income’s rate sensitivity has considerably declined in the first half of 2022. At the end of 2021, a 200-basis points hike in interest rates could boost the net interest income by a hefty 15.1%, as mentioned. However, the latest simulation results show that the 200-basis points hike in interest rates can now boost the net interest income by only 4.7%. Nevertheless, the balance sheet is still asset-sensitive and the net interest income stands to benefit from rising rates, albeit to a lower degree than before.

Considering these factors, I’m expecting the margin to grow by 25 basis points in the second half of 2022 before stabilizing in 2023. Compared to my last report on Eastern Bankshares, I’ve revised upwards my margin estimate because my outlook on interest rates is more hawkish than before.

Higher Than Pre-Pandemic Provisioning Likely

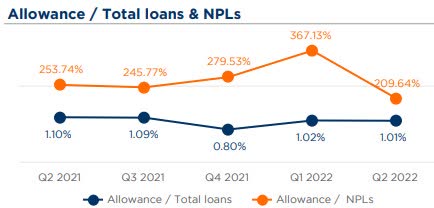

Eastern Bankshares’ allowances dipped to 209.64% of nonperforming loans by the end of June 2022, which is the lowest ratio in the past twelve months.

2Q 2022 Earnings Presentation

I’m expecting the provisioning to be slightly above normal in the second half of 2022 because of the following factors.

- Lowest allowances-to-nonperforming loans ratio in the last twelve months.

- Heightened interest rates. These will make debt servicing more difficult on variable-rate loans.

- Possibility of a recession.

Considering these factors, I’m expecting the provision expense to make up around 0.08% of total loans (on an annualized basis) in the second half of 2022. Further, I’m expecting the provision expense to make up 0.05% of total loans in 2023. In comparison, the provision expense made up 0.07% of total loans in 2019, before the pandemic. Compared to my last report on Eastern Bankshares, I’ve revised upward my provision estimate because I’ve tweaked upwards my loan growth estimate. Further, my outlook on rates and economic growth has changed.

Expecting Earnings To Grow By 54%

The anticipated loan additions and margin expansion will likely drive earnings growth this year. On the other hand, higher than normal provision expenses will likely drag the bottom line. Overall, I’m expecting Eastern Bankshares to report earnings of $1.39 per share for 2022, up 54% year-over-year. For 2023, I’m expecting earnings to grow by a further 16% to $1.60 per share. The following table shows my income statement estimates.

| FY19 | FY20 | FY21 | FY22E | FY23E | ||||

| Income Statement | ||||||||

| Net interest income | 411 | 401 | 430 | 568 | 622 | |||

| Provision for loan losses | 6 | 39 | (10) | 5 | 7 | |||

| Non-interest income | 182 | 178 | 193 | 181 | 188 | |||

| Non-interest expense | 413 | 505 | 444 | 447 | 461 | |||

| Net income – Common Sh. | 135 | 23 | 155 | 231 | 267 | |||

| EPS – Diluted ($) | NA | 0.13 | 0.90 | 1.39 | 1.60 | |||

| Source: SEC Filings, Earnings Releases, Author’s Estimates | ||||||||

| (In USD million, unless otherwise specified) | ||||||||

In my last report on Eastern Bankshares, I estimated earnings of $1.39 per share for 2022. I’ve revised upwards my earnings estimate because I’ve tweaked upwards both my loan and margin estimates.

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

Current Market Price Near The Year-End Target Price

Eastern Bankshares is offering a dividend yield of 2.1% at the current quarterly dividend rate of $0.10 per share. The earnings and dividend estimates suggest a payout ratio of 25% for 2022, which is a sustainable level. As the IPO of Eastern Bankshares was completed in 2020, there isn’t enough data to determine what is a comfortable payout rate for the management. Therefore, I haven’t incorporated any change in the dividend level for this investment thesis.

I’m using the peer average price-to-book (“P/B”) and price-to-earnings (“P/E”) multiples to value Eastern Bankshares. The following table shows the peer multiples obtained from Seeking Alpha.

| Peer Comparison | ||||||

| ABCB | BOH | PACW | FHB | PPBI | Peer Average | |

| P/E GAAP (fwd) | 9.2x | 14.5x | 6.7x | 13.0x | 11.3x | 10.92x |

| P/E GAAP (ttm) | 9.9x | 14.1x | 6.5x | 14.2x | 10.3x | 10.98x |

| Price to Book (ttm) | 1.1x | 2.8x | 0.8x | 1.5x | 1.2x | 1.47x |

| Source: Seeking Alpha | ||||||

| Data extracted after the market closed on August 10, 2022 | ||||||

Multiplying the average P/B multiple with the forecast book value per share of $15.1 gives a target price of $22.2 for the end of 2022. This price target implies a 14.2% upside from the August 10 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/B Multiple | 1.27x | 1.37x | 1.47x | 1.57x | 1.67x |

| BVPS – Dec 2022 ($) | 15.1 | 15.1 | 15.1 | 15.1 | 15.1 |

| Target Price ($) | 19.1 | 20.6 | 22.2 | 23.7 | 25.2 |

| Market Price ($) | 19.4 | 19.4 | 19.4 | 19.4 | 19.4 |

| Upside/(Downside) | (1.4)% | 6.4% | 14.2% | 21.9% | 29.7% |

| Source: Author’s Estimates |

Multiplying the average P/E multiple with the forecast earnings per share of $1.39 gives a target price of $15.2 for the end of 2022. This price target implies a 21.6% downside from the August 10 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 9.0x | 10.0x | 11.0x | 12.0x | 13.0x |

| EPS – 2022 ($) | 1.39 | 1.39 | 1.39 | 1.39 | 1.39 |

| Target Price ($) | 12.4 | 13.8 | 15.2 | 16.6 | 18.0 |

| Market Price ($) | 19.4 | 19.4 | 19.4 | 19.4 | 19.4 |

| Upside/(Downside) | (35.9)% | (28.8)% | (21.6)% | (14.5)% | (7.3)% |

| Source: Author’s Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $18.7, which implies a 3.7% downside from the current market price. Adding the forward dividend yield gives a total expected return of negative 1.7%. Hence, I’m maintaining a hold rating on Eastern Bankshares.

Be the first to comment