DNY59

Readers of my work know that I am a strong advocate for relative strength investing. I often use relative strength as a high level filter to identify attractive investments. However, I am skeptical of applying any process mechanically, as there are always nuances to individual stocks and securities.

Over the long run, mechanically shorting relative laggards appear to be a losing strategy, as shown by the AdvisorShares Dorsey Wright Short ETF’s (NASDAQ:DWSH) 3-year returns of -24.6% p.a., far worse than the inverse of the S&P 500’s 8.2% p.a. in the same timeframe.

Fund Overview

The AdvisorShares Dorsey Wright Short ETF gives investors a convenient way to short weak stocks. The fund has approximately $50 million in assets.

Strategy

The AdvisorShares Dorsey Wright Short ETF is an actively managed ETF that seeks capital appreciation through short selling using the Dorsey Wright Relative Strength Investing approach.

Relative Strength investing involves buying securities that have appreciated in price more than other securities until they begin to underperform. In the context of the DWSH ETF, the manager at Dorsey Wright will systematically short stocks with the weakest relative strength within the investment universe of large-cap U.S. stocks.

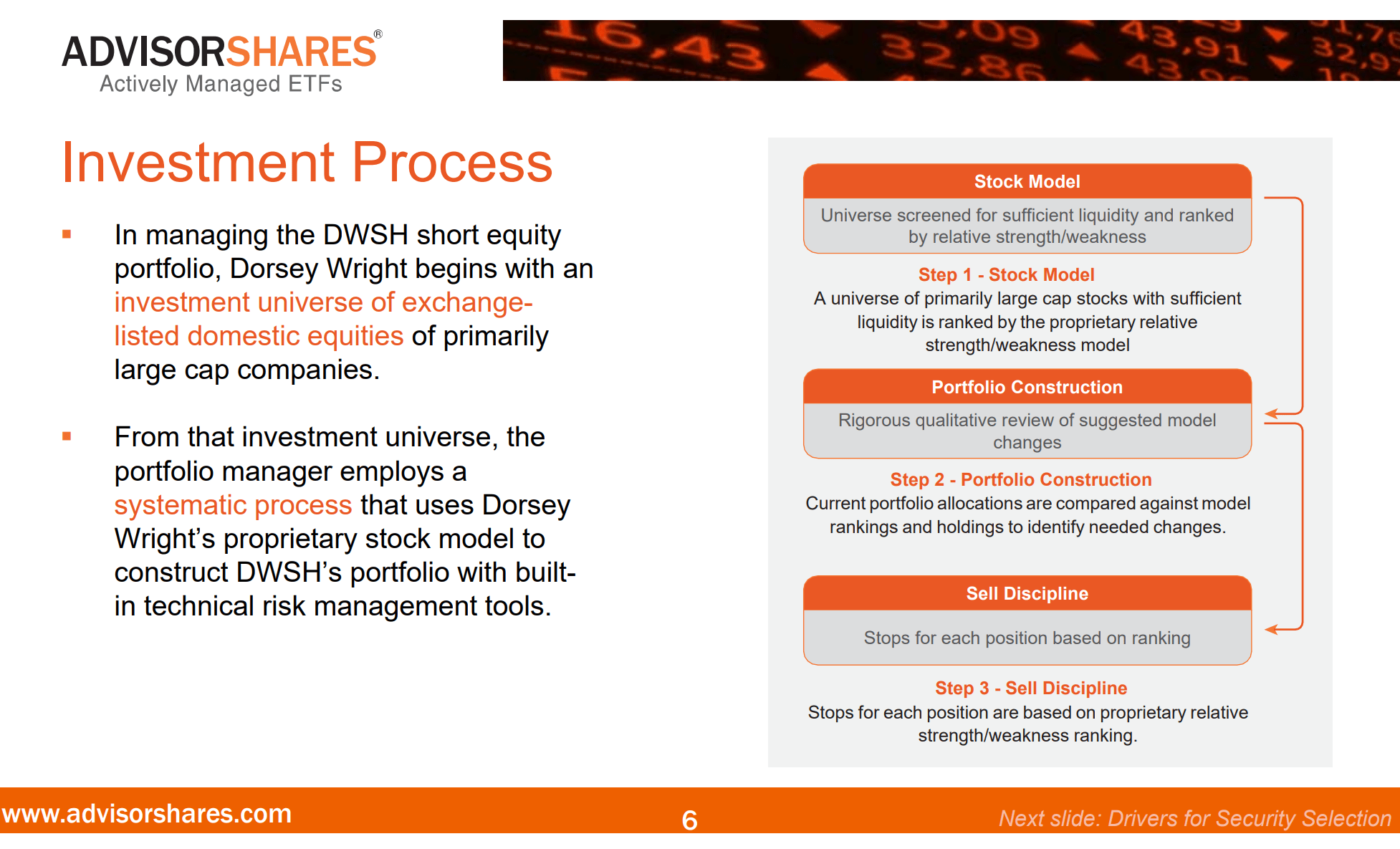

Figure 1 shows the stock selection process for the DWSH ETF.

Figure 1 – DWSH security selection process (advisorshares.com)

Portfolio Holdings

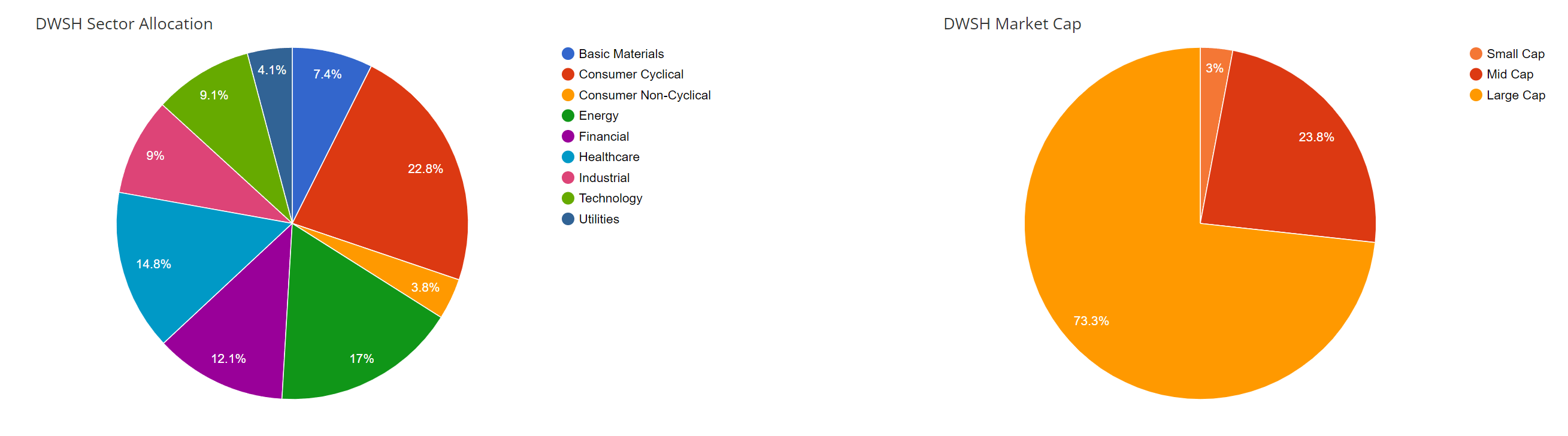

As of November 14, 2022, the DWSH short portfolio contains 101 positions diversified across various sectors (Figure 2).

Figure 2 – DWSH sector breakdown (advisorshares.com)

The fund’s top 10 positions comprise 14.8% of the portfolio and are shown in Figure 3.

Figure 3 – DWSH top 10 positions (advisorshares.com)

Returns

The DWSH ETF’s returns are shown in Figure 4. As to be expected, the DWSH has delivered positive returns in the past 12 months as the equity markets have been in the midst of a deep bear market. Interestingly, DWSH’s 1Yr returns of 26.4% to September 30, 2022, has outperformed the inverse of the S&P 500’s -15.5% return, meaning the Dorsey Wright stock selection methodology has added value.

Figure 4 – DWSH returns (advisorshares.com)

However, this short-term outperformance is tempered by the fact that the DWSH ETF has significantly underperformed on a 3Yr and since inception timeframe, returning -24.6% and -17.4% p.a. versus the S&P 500 which has gained 8.2% and 8.0% respectively.

Distribution & Yield

The DWSH ETF does not currently pay a distribution.

Fees

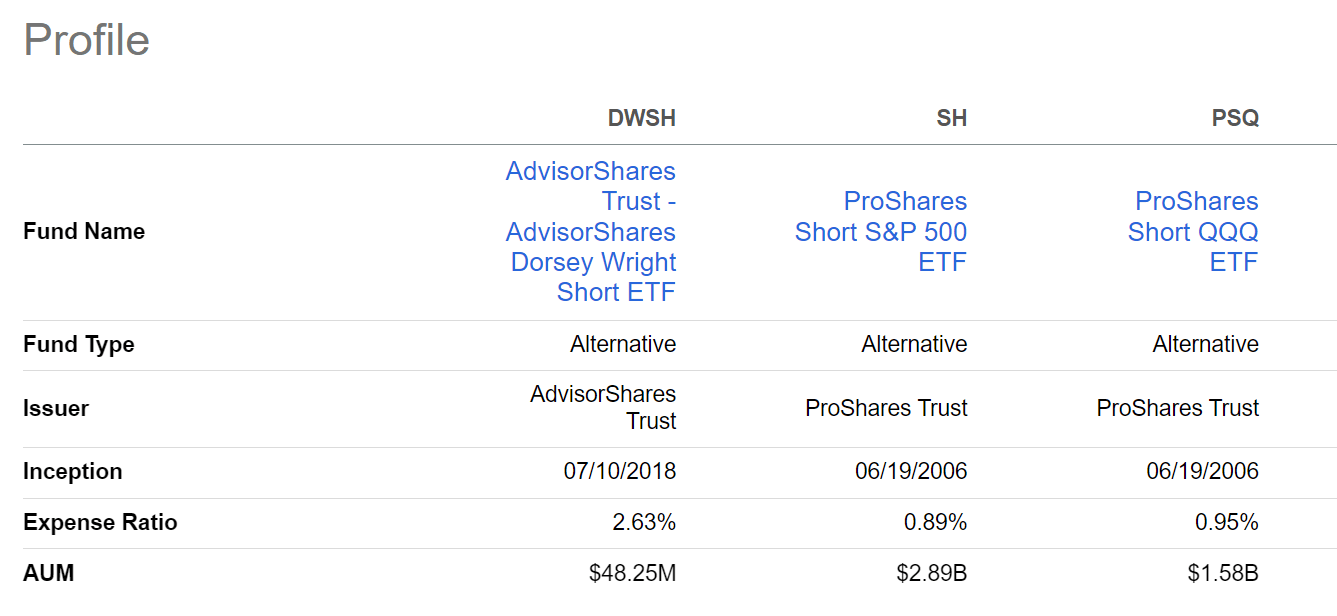

The DWSH ETF charges a high expense ratio of 2.63%. For context, ‘dumb’ bear ETFs like the ProShares Short S&P 500 ETF (SH) and ProShares Short QQQ ETF (PSQ) charges 0.89% and 0.95% respectively (Figure 5).

Figure 5 – DWSH is an expensive fund (Seeking Alpha)

Shorting Laggards Can Be A Dangerous Game

Shorting stocks with weak relative strength is a momentum strategy with the implicit assumption that the drivers causing relative weakness will persist. In theory, this strategy makes sense as the business fundamentals that drive stock prices tend to last for multiple quarters.

However, in practice, maintaining a perpetual short portfolio can be challenging, especially as short positions exhibit negative convexity (winning positions get smaller while losing positions get bigger). This is in contrast to conventional portfolio management where a few winners can carry a portfolio. In shorting, you don’t want to be carried out on a stretcher by a few losing bets.

For example, assume DWSH has identified Netflix (NFLX) as a laggard and shorts the company with a -2% weight. If the short works out, the size of the position decreases, from say -2% to -1.5%, and its impact on the portfolio is reduced. The fund will either have to ‘top up’ the position, or find another short position. On the other hand, if the short doesn’t work and the stock rallies, the position’s impact on the portfolio also increases. If losing shorts are not covered quickly, they can grow and overwhelm a portfolio.

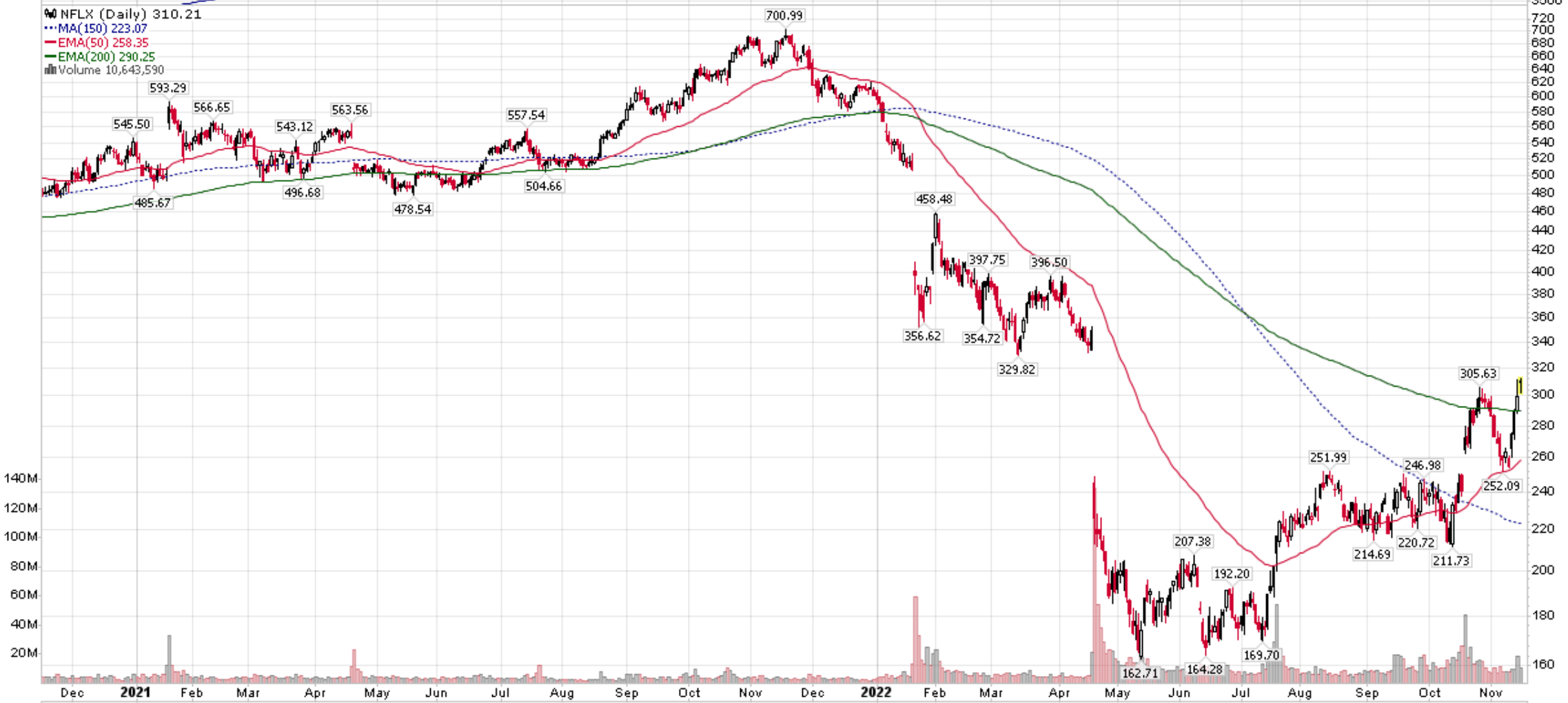

Another problem with the strategy is that weak stocks tend to have the biggest rallies during bear markets. Using the same Netflix example, we can see Netflix has been one of the biggest losers during this bear market, with its stock price declining from over $700 in November 2021 to ~$300 currently, for a loss of almost 60% (Figure 6).

Figure 6 – NFLX stock price (stockcharts.com)

However, we can also see that since the stock bottomed in May of 2020, NFLX has rallied almost 90%. So depending on the lookback period of the relative strength ranking system (say trailing 1 year relative return), NFLX could still be a top ranking short idea, but the fund could be losing money as it continuously have to cover the short back to its model weight.

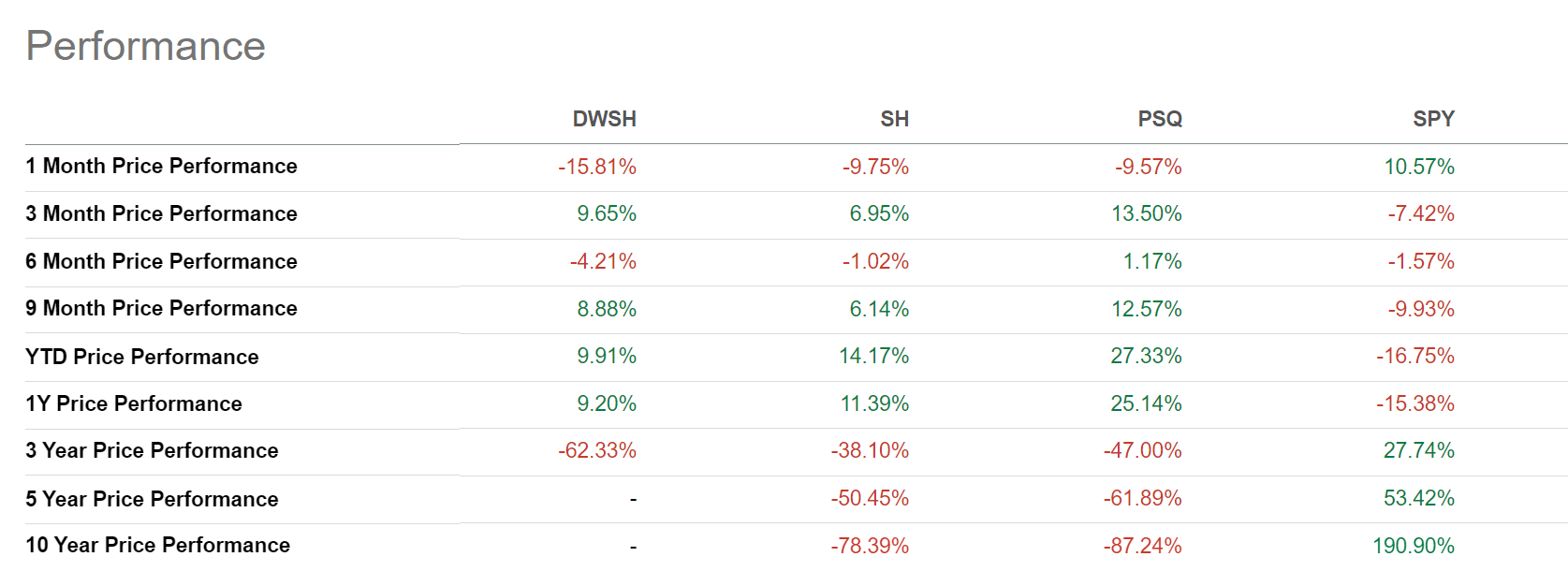

In fact, if we look at DWSH’s performance relative to peer short funds like the ProShares Short S&P 500 ETF (SH) and the ProShares Short QQQ ETF (PSQ), we can see since the markets bottomed in early October, DWSH has underperformed by losing 15.8% (to November 15, 2022) on a 1 month basis vs SH at -9.8%, PSQ at -9.6%, and the SPDR S&P 500 Trust ETF (SPY) with a 10.6% gain.

Just one bad stretch has reversed the short-term 1Yr outperformance we saw in Figure 4 above, with DWSH returning only 9.2% on a 1Yr basis to November 15, 2022 vs. the SPY ETF losing 15.4% (Figure 7).

Figure 7 – DWSH vs. peer funds (Seeking Alpha)

Conclusion

I am a strong advocate of relative strength investing – if you read my work, I often use relative strength as a high level filter to identify attractive investments. However, I am skeptical of applying any process mechanically, as there are always nuances to individual stocks and securities.

A good example is Netflix, which is a top weight in the DWSH ETF. While Netflix may have been a good short earlier in the year when it began to relatively underperform the market, since May, the stock has rallied close to 90% and would have required constant covering for anyone caught short.

Over the long run, mechanically shorting relative laggards appear to be a losing strategy, as shown by DWSH’s 3Yr returns of -24.6% p.a., far worse than the inverse of the S&P 500’s 8.2% p.a. returns in the same timeframe.

Be the first to comment