CHUNYIP WONG

Douglas Emmett (NYSE:DEI) is a REIT specializing in office and multifamily properties. The company owns properties exclusively in Los Angeles, California and Honolulu, Hawaii. Earlier this month, Douglas Emmett announced that it was slashing its dividend by one third and authorized the repurchase of up to $300 million in shares. The new dividend still created a yield of around 5%, but I believe Douglas Emmett’s current stock price represents a solid opportunity for investors.

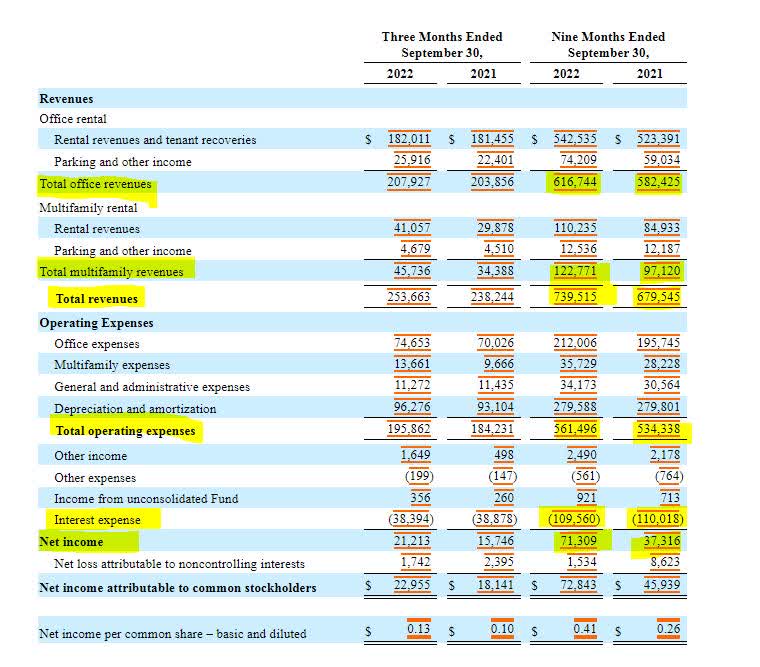

Like many office REITs, Douglas Emmett saw headwinds related to the COVID-19 pandemic and subsequent economic response. Despite the mitigations, the company was profitable in 2021 and saw revenue improvements in both its office and multifamily sectors in the first nine months of 2022. While operating expenses also increased, the income after expenses was sufficient to cover interest expenses and the company’s net income of $71 million year to date was nearly double that of the same period in 2021.

SEC 10-Q

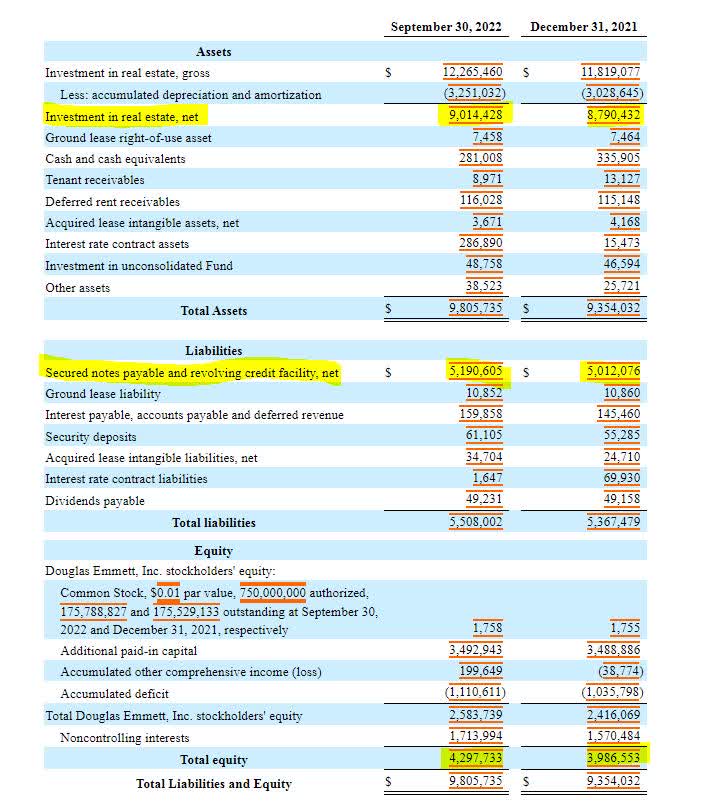

Douglas Emmett’s balance sheet is simple and straight forward. Almost all the company’s assets consist of real estate and nearly all the company’s liabilities are secured notes and a revolving credit facility, presumably collateralized by the real estate holdings. The company has managed to add over $200 million in real estate on approximately $170 in new debt. Due to the company’s holdings of interest rate contracts, shareholder equity has increased by $300 million so far in 2022. The current market cap of Douglas Emmett is $3.3 billion, just 76% of the company’s current book value.

SEC 10-Q

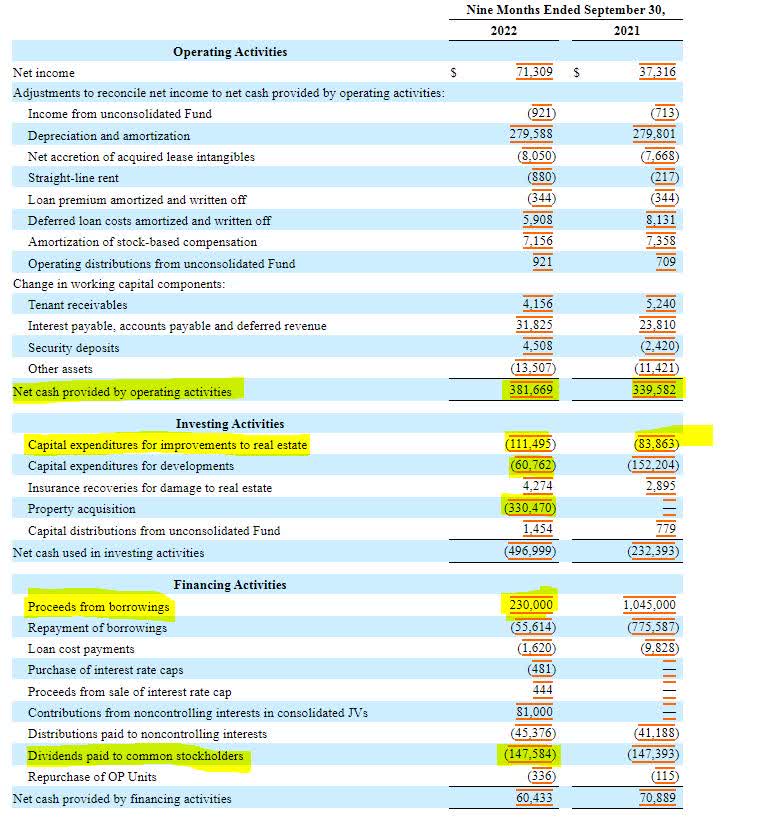

Douglas Emmett’s cash flow statement further highlights the company’s stable financial position. Douglas Emmett’s operating cash flow increased comparatively to net income year over year. At $381 million, the company was able to cover all capital expenditures (both maintenance and development), and still have nearly enough to cover the dividends. It was only because of the $330 million in acquisitions that the company needed to borrow additional funds ($175 million). The dividend cut does help preserve cash flow, but if the company is switching to buying back stock, doing so at below book value may be beneficial in the future.

SEC 10-Q

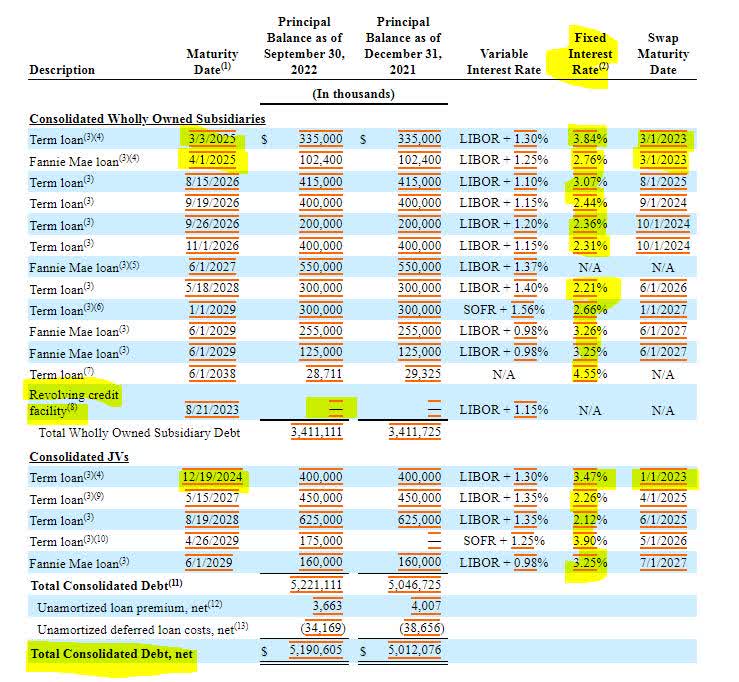

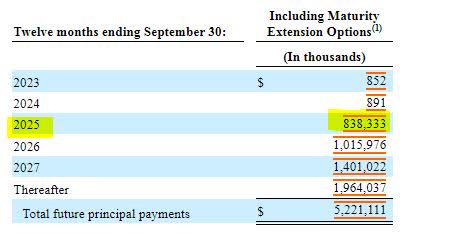

When it comes to debt, Douglas Emmett utilizes interest rate swaps to mitigate interest expenses. Only $28 million of the company’s $5 billion in debt has an interest rate greater than 4%. Additionally, the company has $400 million in debt coming due in 2024 and a similar amount in 2025. Douglas Emmett also has a rested revolving credit facility it could utilize should it need to.

SEC 10-Q SEC 10-Q

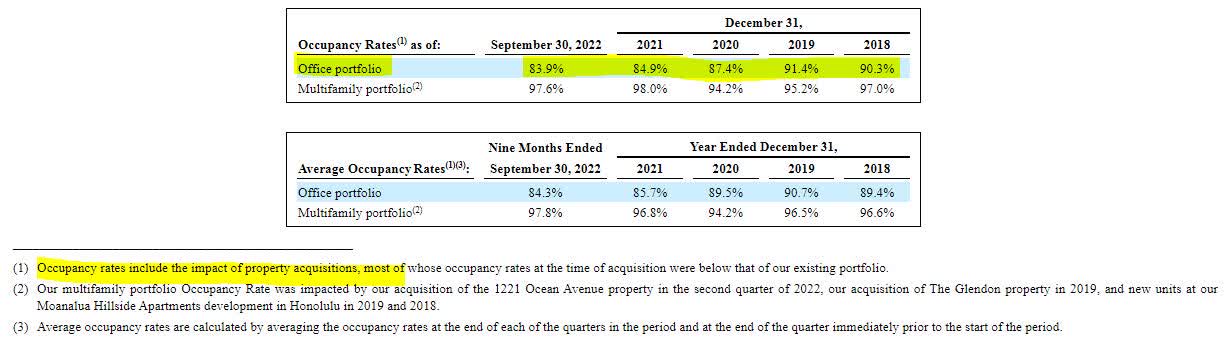

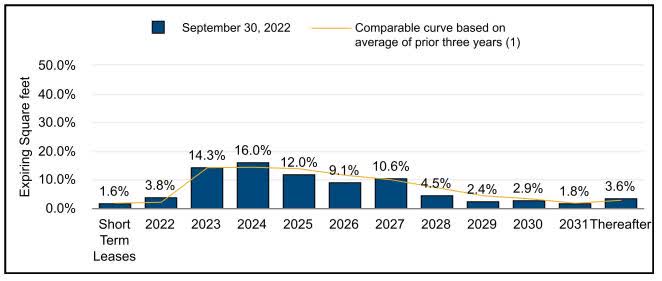

One risk to Douglas Emmett is the ability to retain office tenants. Office occupancy at the end of the third quarter was lower than in 2021 or 2020, suggesting that a bottom in the office real estate space has not happened yet. Additionally, over 33% of the leased square footage is expiring by the end of 2024.

SEC 10-Q SEC 10-Q

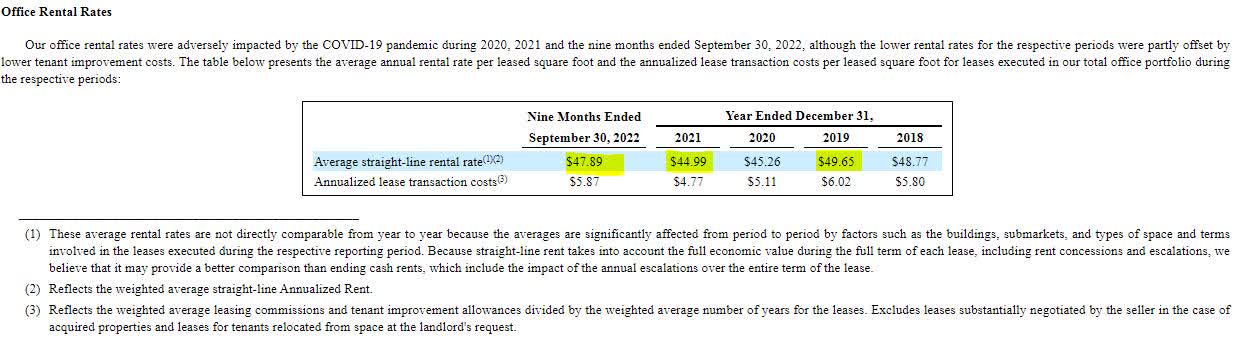

There are a couple of things that Douglas Emmett has going for it to assist with the leasing challenges. First, the company’s office rental rates have partially recovered in 2022, more than halfway back from their COVID related dip. Secondly, Douglas Emmett has only $69 million in contractual commitments across two projects, one of which is an office to multifamily conversion. The company can utilize future cash flows towards making capital improvements in exchange for a long-term lease or to convert more office space into multifamily properties.

SEC 10-Q SEC 10-Q

Overall, I think the market is discounting Douglas Emmett’s share price because of the space it occupies. The company has managed to maintain reasonable leverage with the use of interest rate swaps to lower interest expense, and it has the cash flow to invest in tenant retention or to pivot away from office space into multifamily with its existing properties. Once the office real estate space shows recovery, shareholders should see positive gains.

Be the first to comment