Mario Tama/Getty Images News

Dollar Tree, Inc. (NASDAQ:DLTR) is a leading operator of retail discount stores, with over 16K stores under operation. At present, they operate in two reportable segments: Dollar Tree and Family Dollar.

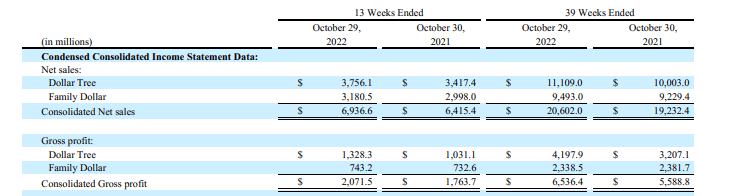

While net sales are fairly proportional between the two segments, Dollar Tree drives consolidated margins. This is due primarily to product mix. Their recent strategic increase in their minimum price point from $1.00 to $1.25/unit also figures into the margin strength.

Q3FY22 Form 10-Q – Consolidated Net Sales And Gross Profit By Segment

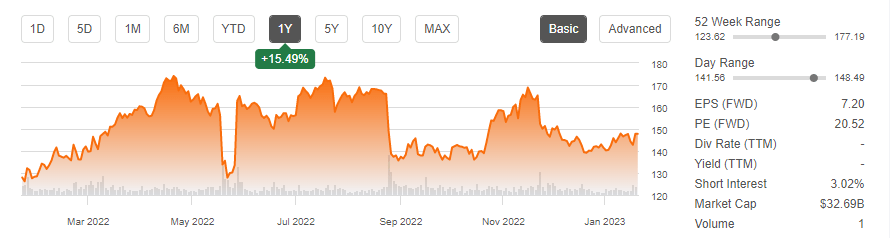

Over the past year, the stock has outperformed the broader index, with a gain of over 15% during this period. This performance also exceeds the 6.5% gains logged by close peer, Dollar General (DG), over the same period.

Seeking Alpha – Basic Trading Data Of DLTR

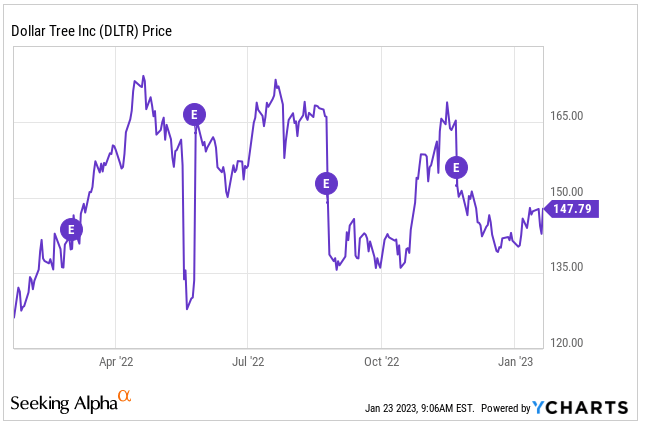

The stock, however, did take a hit following their Q3FY22 results, dropping about 9% immediately following the release. And the stock has yet to make a full recovery.

YCharts – Share Price Performance Of DLTR Following Recent Earnings Results

Though topline results surpassed expectations, poor store traffic levels in relation to other big-box retailers likely contributed to the investor disappointment. In future periods, a greater share of consumable sales is also likely to weigh on earnings due to the lower-margin nature of the product mix.

It wouldn’t be surprising, however, for the company to report greater store traffic levels, especially as consumers increasingly trade-down on goods and groceries. Any increase in store traffic will likely be viewed favorably and will serve as one key catalyst for a share price rebound. With shares still lagging from Q3 trading levels, investors have an attractive opening in advance of their Q4 release.

Recent Performance

In Q3FY22, DLTR reported total quarterly net sales of +$6.94B. This was up 8.1% YOY and +$100M better than expected.

Within the same-store population, comparable enterprise net sales was up 6.5% on both a constant currently basis and when including the impact of Canadian currency fluctuations, due primarily to a 10% increase in average prices, offset by a 3.2% decrease in customer traffic.

Driving same-stores was their Dollar Tree unit, which was up 8.6% on a double-digit increase in average prices. Family Dollar was also up but to a lesser extent of 4.1%, due to a combination of both increased tickets and traffic.

Overall gross profit was up 17.5% during the quarter, led by Dollar Tree, whose segment margin improved 520bps. Margins at Family Dollar, on the other hand, were down 100bps due to both product mix and cost inflation.

Overall, DLTR was in an improved cost position, one marked with lower merchandise costs, including freight, as well as lower occupancy and distribution costs.

This, however, was partially offset by higher costs associated with a greater share of sales attributable to consumable products, which is inherently lower-margin, in addition to higher overall inflationary cost pressures and shrink costs.

The overall improved cost position also translated to a 240 basis point (“bps”) improvement in gross margin. This pushed operating income higher by 22.8% during the period to +$381M. This represents 5.5% of total revenue, a 70bps improvement over the prior period.

Partially negating their higher profit margins was an increase in selling, general, and administrative (“SG&A”) costs. As a percentage of revenue, SG&A came in at 24.4% during the quarter. This is up 170bps from the prior period.

At period end, the company had total cash and equivalents of +$439M. This is down from +$701M due to repurchasing activity and increased inventory purchases and spending on capital expenditures.

Looking ahead, management increased their sales outlook for the year, though they do expect full-year earnings to come in at the lower half of their previous guidance, due to higher costs and product mix.

Current Valuation And Risks To Consider

DLTR currently trades at a forward multiple of 20.5x earnings. While this is in-line with the multiple commanded by DG, it is a premium to the approximately 18x multiple of the broader S&P 500 (SPY).

In addition, the stock does trade above their five-year averages, which historically has been around 17.8x. The elevated multiple exposes the stock to a further comedown in the event of weaker than expected performance.

Furthermore, the increasing shift into the consumables segment is likely to further pressure margins in future periods, as these products naturally are sold at low margins. Increasing competition from larger retailers could also constrain the company from driving foot traffic levels.

Despite the higher multiple, there is still upside embedded within the shares. Assuming a five-year compound earnings growth rate of 12%, which is not unreasonable considering diluted earnings is up about 21% YOY, shares would be reasonably valued at about $175, presuming a CAPM-derived cost of equity of 8.4%.

This is slightly above consensus Wall Street estimates of $163/share, but not significantly so. At any rate, considered together, DLTR could be fairly priced at about $170/share. This would imply upside of over 10% at current pricing levels.

Main Takeaways

DLTR handily beat expectations for same-store growth in both their business units. Overall, net income also came in slightly above estimates. Part of the success is clearly attributable to their improved pricing structure and a broader offering of higher priced products. The combination of the two, for example, contributed to an over 500bps improvement in margins in their Dollar Tree segment.

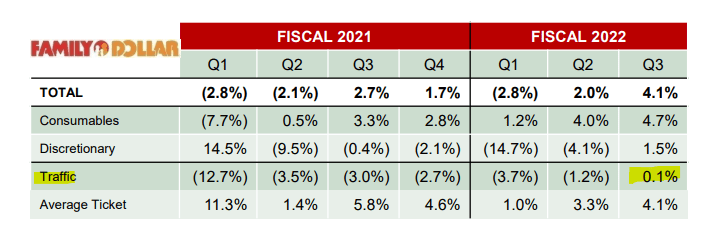

In addition, quarterly traffic at Family Dollar’s same-stores was up for the first time in three years. This was attributable to more competitive pricing in relation to both pure-play competitors and grocery and drugstores. The pricing is particularly important since this unit more closely caters to consumers on the lower end of the income spectrum.

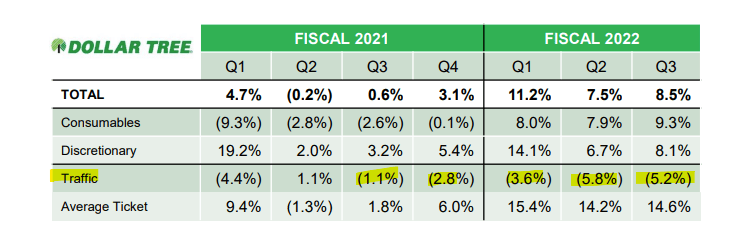

While more competitive pricing has lured more consumers to Family Dollar, the opposite rings true at Dollar Tree, which has now experienced five consecutive quarters of declining traffic, no doubt in part to the higher minimum price points.

Q3FY22 Investor Supplement – Table Highlighting Store Traffic Levels At Dollar Tree Segment

The lower traffic levels at Dollar Tree is perhaps one reason investors weren’t impressed with quarterly results, especially since their big-box competitors, such as Walmart (WMT), have reported traffic gains in recent quarters. And despite the traffic gains at Family Dollar, it’s worth noting the increase was just 0.1%.

Q3FY22 Investor Supplement – Table Highlighting Store Traffic Levels At Family Dollar Segment

Looking ahead, however, it wouldn’t be surprising to see greater traffic gains in both business units. According a recent study published in the American Journal of Public Health, dollar stores were the fastest-growing food retailers by household expenditure share, with notable growth reported in rural areas.

And while dollar stores still represent just about 2.1% of household food purchases, they are increasingly factoring more into consumer food purchases, especially in the current inflationary environment.

Furthermore, another report released by Coresight Research highlighted the growing threat of dollar stores to more traditional grocery stores. Since the beginning of October, for example, more than 20% of consumers have consistently visited dollar stores to buy groceries.

In Q4, if DLTR does report greater traffic gains, that could be one catalyst for further share gains. While a greater share of sales attributable to consumables will weigh on earnings, the traffic volumes will be viewed favorably, especially since it would mark a notable pivot from consistent declines in their Dollar Tree segment over the past several quarters.

For investors seeking a new addition to their long-term portfolios, DLTR appears attractive ahead of their final release for fiscal 2022.

Be the first to comment