simpson33

The Shares Have Bottomed Up

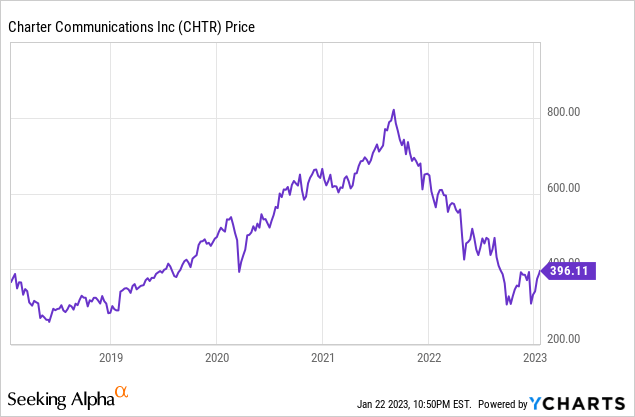

Charter Communications (NASDAQ:CHTR) stock plunged from its all-time high of more than $800 per share to $300 per share in just a year. Indeed, intense competition and rising capital expenditures concerned investors, prompting investors to dump the shares. The stock has since recovered to $396 per share on Friday. Thus, does Charter still offer an attractive buying opportunity?

Tough Competition in the Fixed Broadband Market

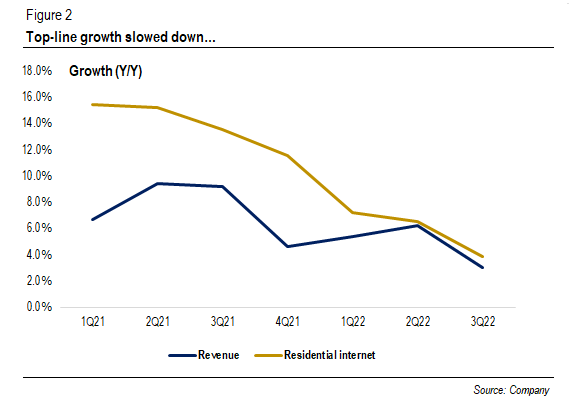

Charter saw its top-line growth decelerate from high single-digit to low single-digit in just a year, as cable operators face intense competition from fiber and fixed-wireless access (FWA). Comcast (NASDAQ:CMCSA) said that the company did not “anticipate residential broadband units to be a significant driver for now.”

Charter’s top-line growth (Company)

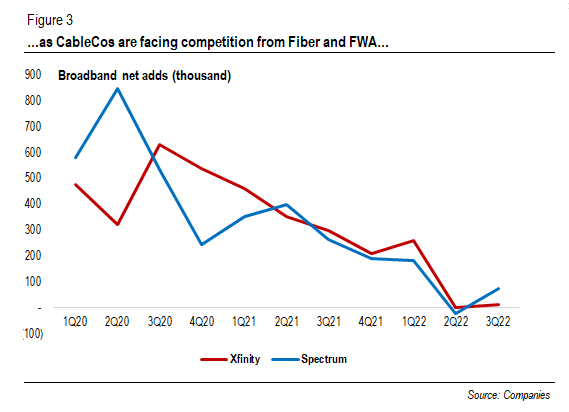

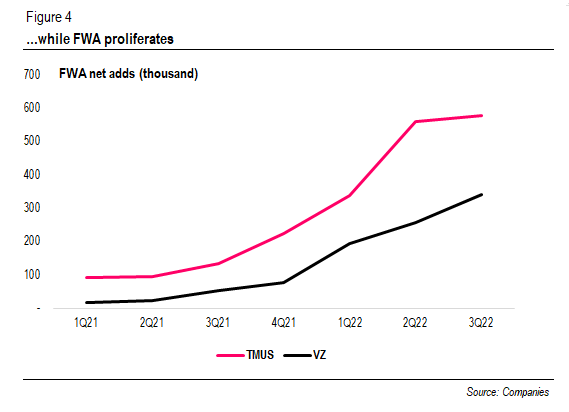

For example, cable’s broadband net adds dwindled as FWA gained traction. In a report published last year, T-Mobile (NASDAQ:TMUS) stated that more than half of its 2 million FWA customer base came from cable, citing “lower price” and “no annual contract obligation” as the reasons why customers switched. As FWA proliferates, does its growth story still intact?

Cable’s broadband net adds (thousand) (Companies) MNOs’ FWA net adds (Companies)

Investors have been wondering whether existing network capacity is sufficient for further FWA growth since fixed broadband typically consumes 40 times higher, on average, than mobile broadband, Analysys Mason estimates. Verizon CEO Hans Vestberg indicated that capacity was not an issue, and Massive MIMO technology helps improve spectral efficiency, as noted in our article on VZ.

Nevertheless, one research suggests that “the service quality” of FWA, excluding that in the mmWave band, trailed behind that of fiber and cable broadband. We believe customers will increasingly demand more data with higher reliability, faster speed, and low latency. Research by Opensignal also suggests that while FWA offerings matched traditional fixed broadband in the “Broadband Consistent Quality” score at quiet times, they tended to dip in the afternoon and evening hours. Therefore, while we agree that the FWA growth story has not yet ended, the long-term opportunity lies in the rural areas where cable or fiber are unavailable.

We believe the competition will be tough between cable and fiber overbuilders. For example, AT&T is still pushing its fiber build, aiming for 30 million homes passed by 2025. Frontier Communications (NASDAQ:FYBR) said during the 3Q22 earnings call that it reached 3.2 million homes in fiber footprint with a ~43% penetration rate. Smaller cable companies, such as Altice USA (NYSE:ATUS)–planning to bring multi-gig speeds to two-thirds of its footprint by 2025, are jumping on the bandwagon.

Playing A Long-term Game Is The Only Way To Go

It makes little sense for cable companies like Charter and Comcast to upgrade its existing cable into all-fiber, at least for now. An estimate suggests that an all-fiber upgrade would cost $1,000 per home passed, although the figure varies among operators. Upgrading the entire footprint will require Spectrum to spend a jaw-dropping $55 billion. Instead, cable operators opted to upgrade their existing hybrid fiber-coaxial (HFC) network, believing such upgrades would cost significantly less than all-fiber.

Charter unveiled its HFC upgrade plan in three steps. First, Charter plans to expand the spectrum to 1.2 GHz and add the upstream capacity by allocating more bandwidth under a high split. As people can work from anywhere, the use of video conferencing, for example, proliferates, demanding more upstream capacity. The management claimed that more spectrum dedicated equals to 30x upstream speed increase from the current speed. In addition, the company have started this upgrade in some “mid-sized” markets.

| Split | Upstream Spectrum | Approx. Upstream Capacity |

| Sub-split | up to 42 MHz | 100 Mbps |

| EuroDOCSIS-split | up to 65 MHz | 375 Mbps |

| Mid-split | up to 85 MHz | 525 Mbps |

| High-split | up to 204 MHz | 1700 Mbps (1.7 Gbps) |

Source: Broadband Library

Second, Charter will pursue a distributed access architecture (DAA) with a remote PHY approach, which “pushes” the physical RF layer from the cable modem termination system (CMTS) to the node via remote PHY devices or RPDs. Moreover, Charter will introduce the virtualized CMTS technology.

Lastly, cable operators are poised to go through the so-called network evolution that includes DOCSIS 4.0. In general, DOCSIS 4.0 enables operators to expand the capacity of an existing cable, allowing them to offer the same 10 Gbps downstream capacity and up to 6 Gbps upstream capacity vs. the current 2 Gbps upstream of DOCSIS 3.1. Charter is pursuing the extended-spectrum DOCSIS (ESD) path–extending the spectrum ceiling to 1.8 GHz, while Comcast is lining up for Full Duplex DOCSIS (FDX).

Elad Nafshi, Comcast’s EVP and Chief Network Officer, said the costs would be under $200 per passing on a gross basis, as cited in Fierce Telecom. Meanwhile, Charter expects the upgrades will only cost $100 per home passed, although the figure does not include a new DOCSIS 4.0 CPE, which could be much more expensive than its DOCSIS 3.1 counterpart. Analysts have stated the possible reasons why upgrade costs are different between the two companies.

We believe those upgrades, including DOCSIS 4.0, will allow cable operators to compete better with fiber overbuilders. Recent tests by Charter show that a DOCSIS 4.0 demo with six 1.8GHz amplifiers (or N+6) generated 8.3 Gbps downstream and 5.3 Gbps to 5.5 Gbps upstream. Because speed is no longer an issue, further competition could be down to price, at least in the foreseeable future, in our view.

For now, Charter has been aggressive, offering a bundled package of internet, advanced Wi-Fi, and a single mobile line under Spectrum One for $49.99/month for 12 months.

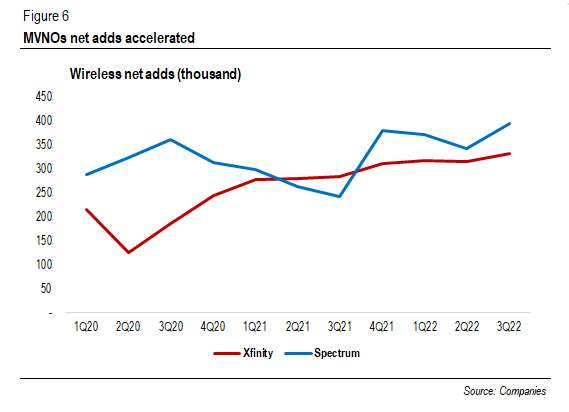

Mobile As A Source Of Growth

On the contrary, though MVNO deals, cable operators saw their wireless net adds accelerated. Comcast and Charter posted 333,000 and 396,000 net adds in 3Q22, respectively. We believe that MVNOs raked more subscribers as people looked for cheaper options. Cable operators typically offer two plans: Unlimited and by-the-Gig plans, and their mobile services are limited to their internet subscribers. Xfinity Mobile charges $45 per month for single line and $30 each per month for two lines. By-the-Gig plan starts from $15 per month for 1 GB. Again, Charter took a more aggressive approach by offering a $29.99 unlimited plan for one line.

MNVOs’ net adds (thousand) (Companies)

While cable operators can better compete with MNOs thanks to its competitive pricing, it does pose a serious question: is the business profitable? While Xfinity Mobile has reached a breakeven point, Spectrum Mobile has been in the red at the EBITDA level. In order to transform mobile business into a profitable one, Charter is taking a few initiatives.

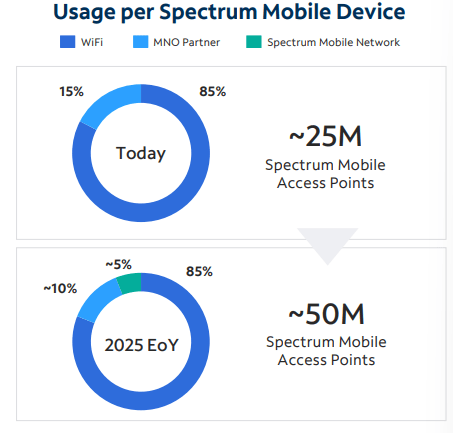

First, Charter plans to build its small-scale 5G network in the CBRS spectrum, which can help offload some traffic from Verizon’s network and offset MVNO wholesale costs. The company expects its network to bear 5% of traffic by 2025.

Spectrum’s target of traffic usage (Company)

Second, Spectrum One is competitive in terms of price. In our view, such a competitive offering will attract more internet and mobile customers and allow the company to retain its customers. Once the promotional period ends, which possibly lasts for 12 months, Charter might work on mobile’s profitability.

Valuation

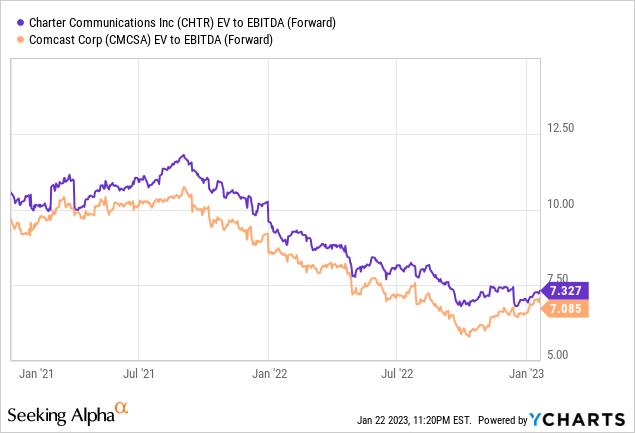

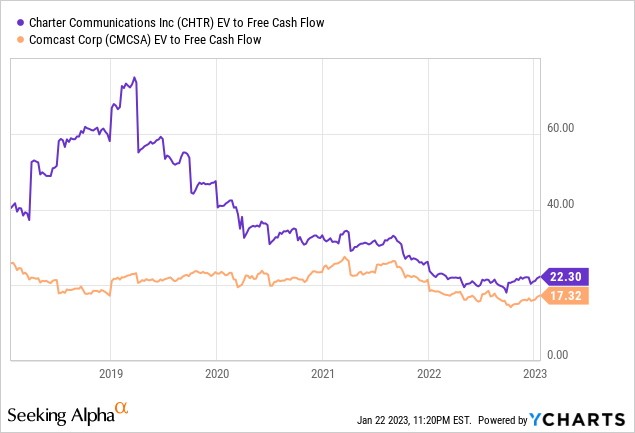

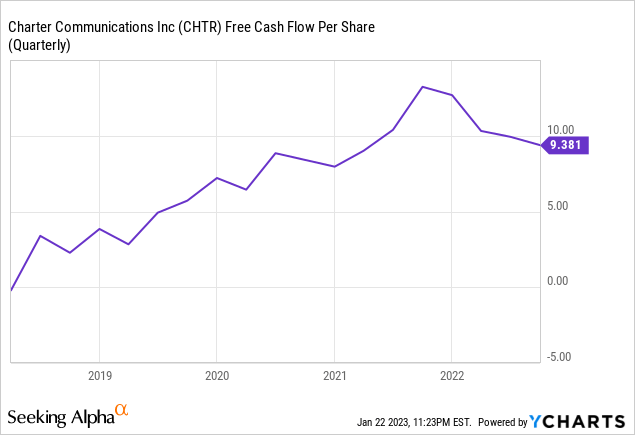

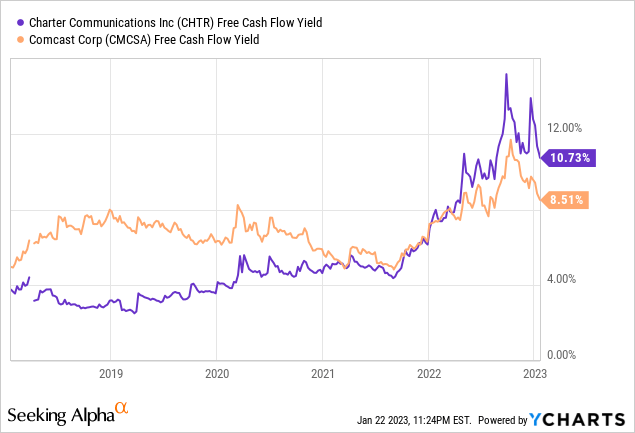

Charter is trading at around 7x of its forward EBITDA, lower than its 5-year average of 10x per Morningstar data. Though the price has recovered to ~$400 per share, is there any buying opportunity left for investors? We should ask whether Charter’s business is better or worse than before, and we believe that one way is to look at the company’s FCF/share.

We like Charter’s FCF/share expansion, as it grew more than 25% annually, on average, in the last five years. However, Charter’s FCFs will likely dip a few years ahead due to the network evolution initiative and rural build.

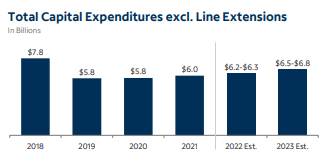

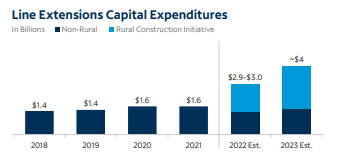

Rising capital expenditures spooked investors, as the company plans to spend $6.5 billion-$6.8 billion, a rise from the usual ~$6 billion, including the so-called network evolution estimated to require $5.5 billion–spread until 2025. For line extensions CapEx, Charter will allocate $4 billion, a significant portion of which stems from the rural build commitment totaling $5.9 billion. Charter expects to spend more than $10 billion in CapEx this year.

Total CapEx excluding line extensions (Company) Line extensions CapEx (Company)

But is such a decline in free cash flows structural or a temporary one? Such spending is required to expand the company’s footprint and stay competitive with fiber overbuilders. Furthermore, the company’s network expansion bore fruit, as the company achieved 40% of penetration for its rural extensions and 50% for state grants after six months. As CapEx is estimated to peak in 2025, it will return to the business-as-usual (BAU) level. The $42.5 billion BEAD program will require the company to spend, should it participate, but it will not start until at least 2024–probably much later, during which the CapEx level should have peaked.

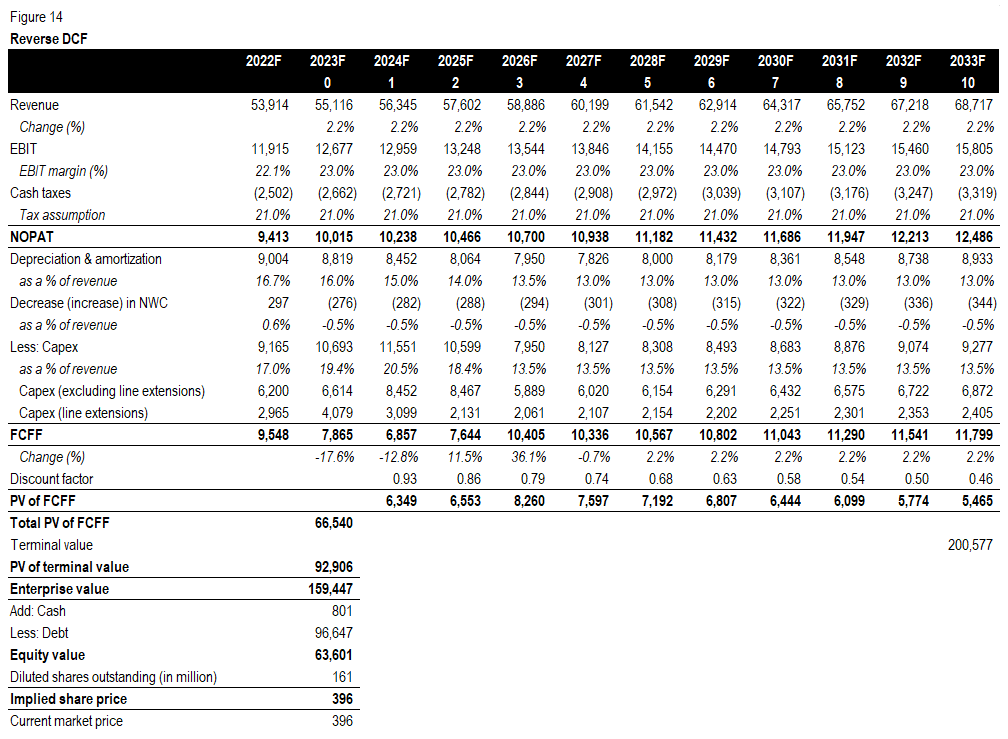

Further, we did a 10-year reverse DCF, assuming 8% WACC and 2% FCF growth in perpetuity. We found that the market is expecting a long-term revenue growth of ~2.2%, lower than Charter’s 5-year revenue CAGR of 5.3% and our 2022F estimate of 4.3% (Y/Y).

Charter 10-year reverse DCF (Vektor Research)

While we believe that the competition among fiber, fixed wireless, and cable will intensify in the coming years, growing, say, 3% a year in the next ten years seems achievable. A 3% of long-term revenue growth implies $466 per share, an 18% upside. Still, we believe the stock does not provide a comfortable margin of safety at the current price ($396 per share).

Conclusion

Intense competition and rising capital expenditures did concern investors. However, we think that playing a long-term game is a must for Charter to compete with fiber and fixed wireless. Deteriorating cash flows will be temporary and should be back to normal after the company finishes its network upgrades.

Further, while the Spectrum Mobile is still in the red, scaling up remains the main theme of the business. And the company could work on profitability once the promotional period ends, as a converged bundle with aggressive pricing (Spectrum One) could help acquire and retain its customers. However, our reverse DCF model suggests that the stock price does not provide a comfortable margin of safety. Therefore, we assign a HOLD rating for Charter.

Be the first to comment