PonyWang

Investment overview

Since 1990 until 2020, global semiconductor market grew approximately 7.5% CAGR and outgrew global GDP by 2.5% per year. Since Taiwan Semiconductor Manufacturing (NYSE:TSM) IPO in 1994, the company has grown its market value by over 18% p.a. excluding reinvestments of dividends. Even though, the global semiconductor market is estimated to decline in 2023 by 4.1%, I expect that dominance of TSM is going to continue in the future and occasional cyclical downturns are an opportunity to increase its exposure in the stock. There is a tendency the strongest companies are starting to grow during bear markets among first. A similar pattern is visible in TSM stock. In last six months, the company has been steadily outperforming its competitors, mainly Intel (INTC) and Samsung Electronics (OTCPK:SSNLF).

Seeking Alpha

Ability to gain upper hand in difficult markets

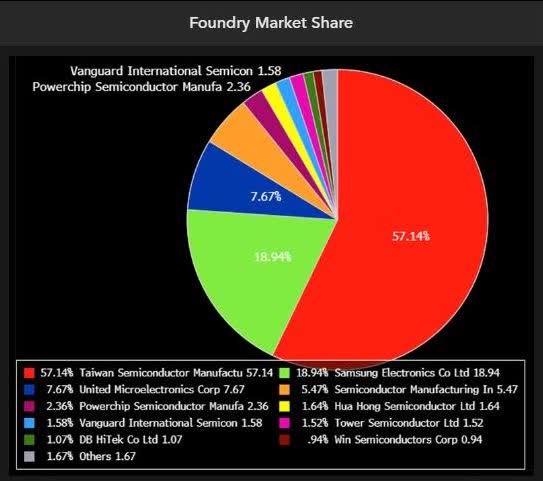

To succeed in semiconductor foundry business, the company needs enough scale to spread over exorbitant investments needed to build manufacturing facilities. Semiconductor Industry Association estimated that initial investment in building foundry manufacturing facility exceeds US20 billion. Only a handful of companies in the world can afford to spend such amounts. TSM was the first semiconductor producer which adopted low-cost pricing strategy to develop necessary scale. The business model was based on the premise of giving price concession to customers as foundries make productivity improvements and cost synergies. As the customers were motivated to sign longer-term production agreements with TSM, the company was able to spread its investments and invest in more sophisticated nodes. According to Bloomberg Intelligence data, TSM has over 57% market share, which is two times higher than its closest competitor, Samsung Electronics. There is a big debate whether Chinese competitors, such as UMC or SMIC can close the gap in foundry manufacturing. If market share predicts future profitability, then it looks highly unrealistic that Chinese companies can compete at the same level.

Bloomberg Intelligence

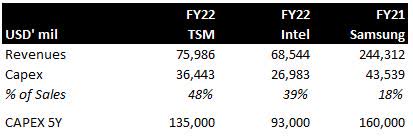

In 2019, the semiconductor industry’s CAPEX as proportion of sales was 26%. Semiconductor manufacturing is the most capital intensive in the semiconductor’s supply chain. Comparison of capital investments among TSM, Intel and Samsung show a visible pattern. TSM is investing the highest proportion of its sales and it is outspending its competitors, both Intel and Samsung. For Samsung, the foundry business is proportionately smaller to its memory business or electronics business and still their total CAPEX in absolute numbers is similar in size to TSM’s. All in all, investments in R&D and CAPEX are part of a virtuous cycle in which new investments create more scale, which creates more sophisticated nodes, which create higher profits for new investments.

Annual Reports, Bloomberg, own work

Dominance in the most sophisticated chips

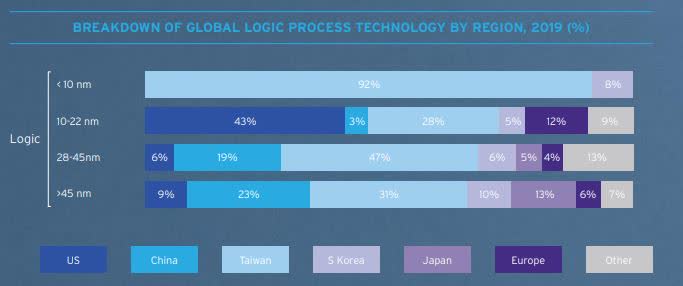

In semiconductor manufacturing, there is a strong correlation between each new technology node and level of investments necessary to achieve this node. Most sophisticated chips, those under 10-nanometers are proportionately more capital intensive than slightly higher nodes. 7-nanometer and 5-nanometers node chips account for 50% of TSM’s FY2021 revenues. Currently TSM is in the development phase for 3-nanometer and even 2-nanometers nodes. It is true that some chips, such as DAO (discrete, analog, others) do not always require the smallest nodes, but for logic chips it is usually the case that smaller equals better. To see the dominance of TSM in the most sophisticated chips, let’s see the breakdown of logic chips by different nodes.

SIA: State of the U.S. semiconductor industry 2021

In the table above, Taiwan is the proxy for TSM. As can be seen, TSM is manufacturing approximately 92% of all semiconductors under 10-nanometers. With the introduction of 3 and 2-nanometer nodes, this dominance will only strengthen.

What are the possible risks?

Geopolitical risks persist as the most significant risk to this investment thesis. Taiwan is in the middle of a fight between two economic powers, the US and China. Both countries are realizing the importance of semiconductors which are necessary for technological dominance in the defense industry. TSM is aware of these risks and tries to diversify its production capacity away from Taiwan. The new production facility in Arizona should start commercial production in 2024, but TSM’s production and its stock would be negatively impacted in case of any conflict.

Conclusion

The semiconductor industry is currently in the downturn, measured by a decline in revenues and lower wafer shipments. Historically, it has been a winning strategy to bet on the strongest companies in the cyclical downturn as those are the companies that start to grow first and outperform their peers. Foundry IC business is characterized by three factors. Scale, level of investments and technical sophistication of chip nodes. TSM is dominating on all these characteristics, and it is increasing its moat in each new business cycle. TSM is trading at undemanding valuation of 12x FY2024 earnings, which I believe is not fully reflecting TSM’s intrinsic value.

Be the first to comment