jetcityimage

Company overview:

Domino’s Pizza, Inc. (NYSE:DPZ) is a pizza company operating internationally. The company offers takeaway and delivery pizzas from Domino’s company-owned and franchised stores.

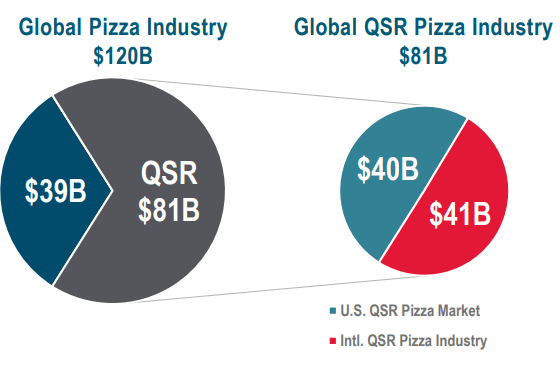

The business is arguably the largest pizza brand in the world, with an impressive slice of market share.

Domino’s market share (Q3 Investor pack)

The business operates through three segments:

- U.S. Stores – This segment is income from DPZ owned and run restaurants.

- Franchises – This segment is recurring income generated from their extensive domestic and international franchise network, in exchange for use of their IP.

- Supply Chain – This segment generates income by selling food, equipment and supplies to franchisees.

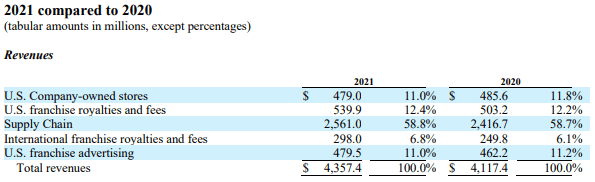

Of the three segments, most would believe they are ranked in order of size, but that would be incorrect. Domino’s Pizza, Inc. only operates 2% of the total number of Domino’s stores. In that case, is Franchises the largest? No. 58.8% of DPZ’s income is derived from Supply Chain services.

DPZ’s revenue split (FY21 Annual accounts)

The Domino’s Pizza, Inc. business is in effect a supply chain business, with a large franchise operation. This is important to identify from the start, as this creates a level of flexibility. This is not a capital-heavy business with thousands of leases / stores, etc.

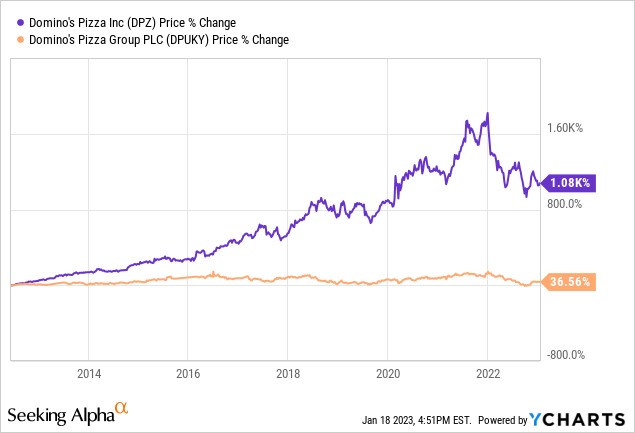

Investors are clearly a big fan of this, with DPZ performing significantly better than its Franchise counterpart, Domino’s Pizza Group plc (OTCPK:DPUKY).

In order to assess the attractiveness of DPZ, we will analyze DPZ’s current and forecast financial performance, with a relative assessment against peers. We will also consider a number of key themes and factors which drive success within the Quick Service Restaurant (QSR) industry. Finally, we will layer in our current macro view, and how this will drive future revenue.

Financials:

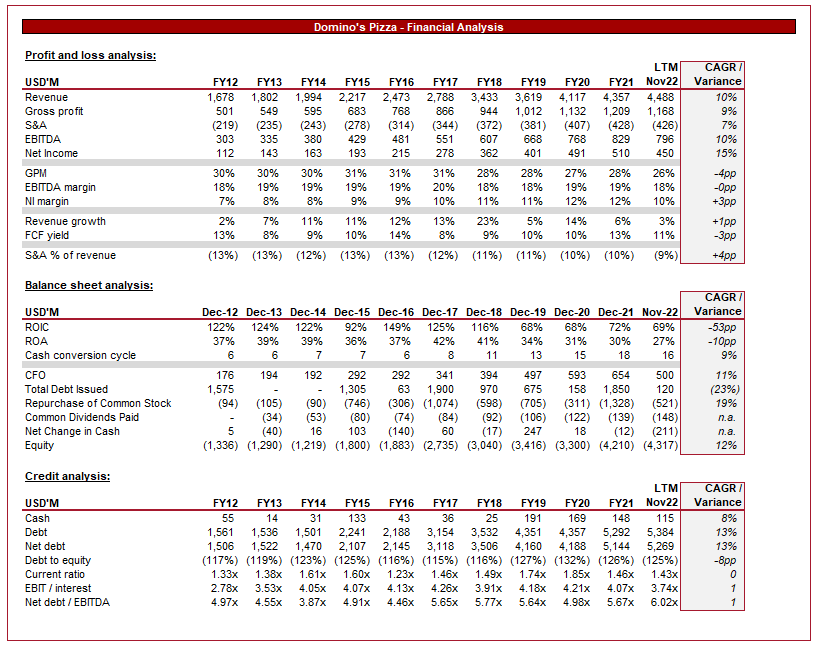

DPZ – Financials (Tikr Terminal)

Domino’s Pizza, Inc.’s financial performance over the last decade has been incredibly impressive, growing at a CAGR of 10%. This has been achieved without a parallel increase in S&A spend, suggesting Management are able to achieve efficient growth.

Gross profits had been growing in line with revenues but has dipped in the LTM period due to increasing food costs. Inflation has hit the business in 2022, with Management expecting continued margin corrosion in the near term.

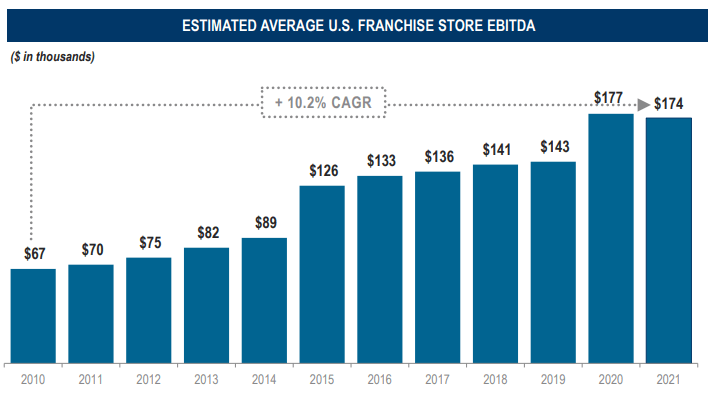

Importantly, growth is coming from current stores as well as new locations, with new stores more accretive than previous. This is a key metric to consider, as a decline can be concealed by new store openings.

US Franchise EBITDA growth (Q3 Investor Pack)

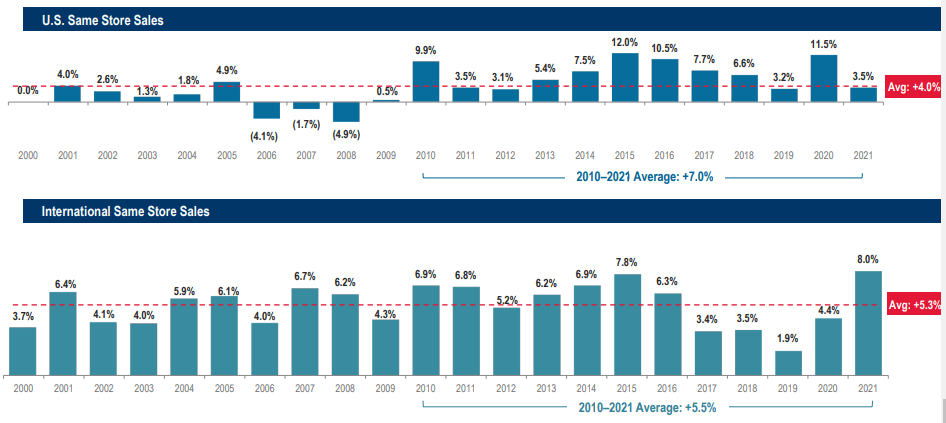

Same store sales (Tikr Terminal)

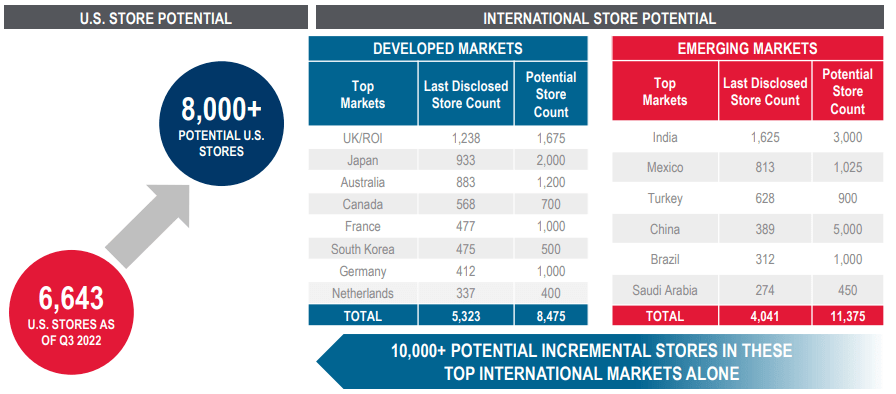

Management is of the belief that this will continue, with over 100% growth in stores possible. This is incredibly bullish and will likely take a significant amount of time. Current growth in stores is in the region of 6.6% annually. Domino’s footprint is fairly low in key regions of growth, such as China and Brazil, which provides opportunity for growth in economics alongside stores.

Store potential ( Q3 Pack)

Further, the diversification in locations ensures there is little concentration risk, which is beneficial for a business with product concentration.

The simplistic financial structure allows for much of the profits post S&A to translate straight into free cash flow, with DPZ consistently posting returns in excess of 10%.

From a credit prospective, we observe debt increasing at double digits over the historical period. We do not consider it unmanageable, although their interest coverage is poor. Management likely are unconcerned due to the relative stickiness of demand due to the sheer number of locations globally.

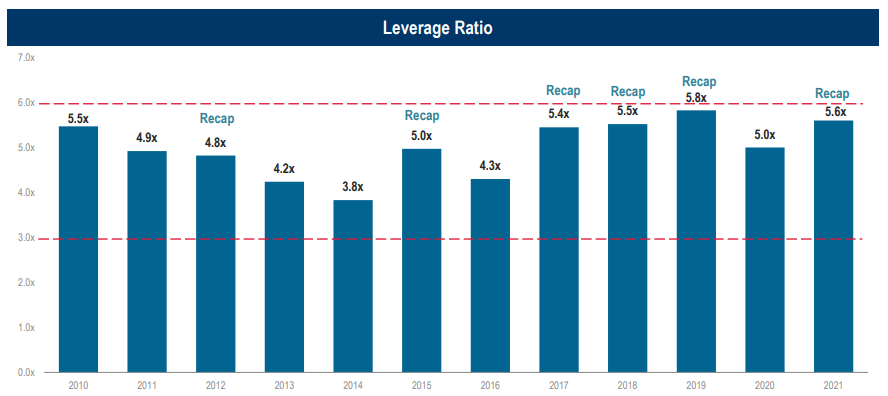

A factor which is not a deal breaker, but is unfortunate to see, is their dividend funding. Management are regularly issuing debt and occasionally net-cash-change negative due to dividend payments. Management seem to be managing the level of this, with the intention to keep their leverage ratio below 6x.

Leverage ratio (Q3 pack)

Digital business:

One of the ways DPZ has managed to grow at the rate it has, especially relative to its competitors, is due to the development of their app. The app is far superior to their competitors and is the most developed, allowing for orders and deliveries.

This was incredibly valuable during COVID-19, with the relative adjustment required being minimal. It is difficult to compare Domino’s to its competitors regarding online sales due to its focus on take-away but regularly boasts market leading online sales.

Deliveries:

Providing delivery services is an incredibly shrewd decision by DPZ. This allows for control over the delivery process and thus quality control. The most important factor is that it ensures obstacles between customers are removed. As mentioned, Domino’s focus on take-away and so requires customers to come to them. If they can eliminate that barrier, consumers have one less reason to not order.

This is an area that is coming under threat, however. With the rapid rise of e-commerce delivery businesses, Domino’s is no longer one of the few QSR’s with a reliable delivery service. Now you can get most of them at a relatively affordable price and time. Given how high these stocks are trading, it is clear that deliveries are of material importance to consumers. This means a big competitive advantage is likely dwindled and will continue to do so as delivery services expand to more rural areas.

Supply chain:

DPZ’s ownership of the supply chain process is a great compounding component. As sales grow, the number of franchises will increase due to the attractiveness of the brand, but it also means more food will be needed. This is natural way to increase the monetization of each location.

Further, similar to deliveries, this allows DPZ to control a larger segment of the total process. This means ingredients can be sourced to their desired quality, kept uniform across geographical locations, and allows franchises to focus on management. For these reason, supply chain control is both financially beneficial and good for their product quality.

We are now seeing the downside of operating the supply chain. Food costs are rising and in many pockets we are seeing labor shortages (impacting stores also). These costs have yet to be passed on, resulting in margins contracting. It is likely that we will see some changes to the pricing structure going forward.

Fall of QSR:

With greater media attention and education, many are looking to eat more healthy and move away from QSRs. We have seen strong growth in healthy-alternatives and a move towards cooking at home. The financials suggest this has yet to impact Domino’s but remains a sustained and unwavering risk. This is partially the issue with being reliant on one product; if Pizza were to fall out of favor, it will likely be because of its relative unhealthiness. Should this occur, it would systematically damage Domino’s Pizza, Inc. Although this is unlikely, slowing growth is certainly possible.

Macroeconomic conditions:

Economic conditions are an important factor to consider as it is a determinant of demand within an economy. Although QSR’s are not a luxury necessarily, they have many cheaper alternatives and competitors.

The reason for slowing market conditions in 2022 into 2023 is inflation. Inflation is currently 6.45% in the US and 9.2% in the Eurozone, remaining at an unsustainable level for most of 2022. The cause of inflation is many factors, including the Russian Invasion of Ukraine. Central bankers have responded by raising rates, in order to calm demand. This is likely working, but is very gradual. For this reason, it is likely inflation and interest rates will remain heightened for much of 2023. This has led to a living crisis for many households, who face rising prices and increased borrowing costs. With consumers tightening their wallets, less expenditure has been available for discretionary spending. For many, QSR is the cheapest option for food and will continue to consume. However, for many, QSR’s are a regular luxury. For those individuals, they may choose against consuming at the rate they are, driving demand down. With revenue down in the Q3 period for DPZ, this is likely a contributing factor.

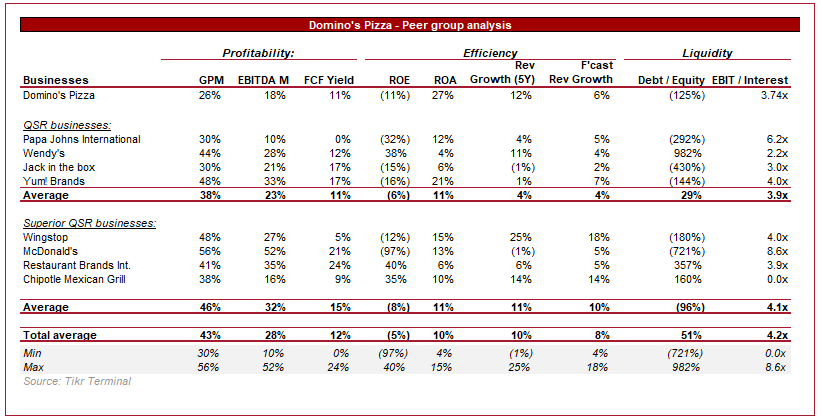

Peer comparison:

Peer group comparison (TIkr Terminal)

When assessing the QSR market, we have a mix of operating models. For this reason, it is not necessarily a like-for-like comparison, but on a wholistic basis, profitability is comparable.

What we see is that there are some clearly superior businesses, either due to growth or profitability. Profitability is noticeably high in the market and so superiority comes with greater growth or very large margins.

Although DPZ has achieved market leading growth (v. average) in the historical period, it is forecast to grow at a far more mediocre rate. Further, margins are attractive on a nominal basis but relative to competitors, they fall flat.

Our view is that DPZ is a middle-of-the-road business, which through intelligent management has posted strong results. That said, this is not unique to the market and investors have a lot of choice.

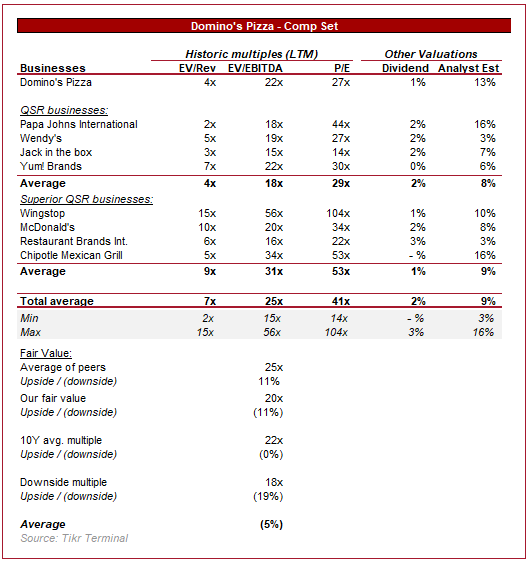

Valuation:

Peer group valuation (Tikr Terminal)

Domino’s Pizza, Inc. is valued slightly below its peer group in every metric. The reason for this is likely a combination of its relative performance and commercial factors, such as the fact it is reliant on one type of food.

Our view is that this is warranted, with DPZ’s valuation likely sitting between the first and second cohort, on the lower end.

Our valuation reflects 4 separate scenarios, a standard average of its peers, its 10Y historical average multiple, a downside contraction to 2014 levels and our deemed fair value. This is based on discounting superior multiples and factoring in comparable peers.

Given margin for safety and general market volatility we are experiencing currently, our view would be that Domino’s Pizza, Inc. is valued correctly.

Conclusion

Domino’s Pizza, Inc. is a tremendous business with healthy sustained growth. The business has a wide moat and has scope for continued growth through emerging markets. There are several themes in the market which have both positive impacted the business (own delivery) and negatively impacted them (supply chain problems). Overall we think Domino’s Pizza has navigated these factors well.

This all said, we are entering fragile market conditions. Business trading will be more difficult and markets will be less forgiving. It is possible that Domino’s Pizza, Inc. store growth will slow with greater borrowing costs, demand will slow with lower discretionary income and costs will continue to rise. When this is factored in, the Domino’s Pizza, Inc. valuation must reflect adequate upside for investors, and we do not see it.

For this reason, we rate Domino’s Pizza, Inc. stock a hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment