gorodenkoff/iStock via Getty Images

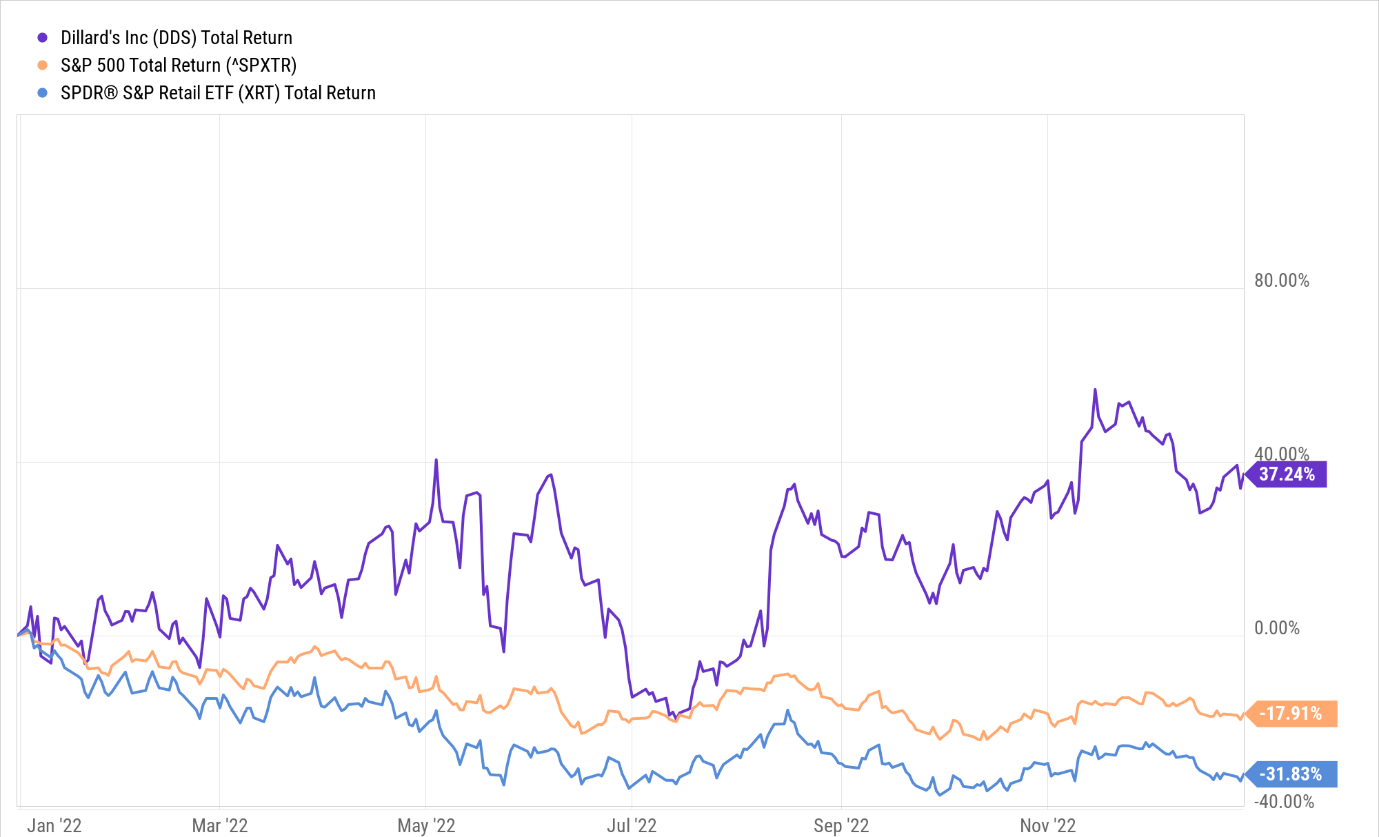

The stock of department store- Dillard’s (NYSE:DDS) has proven to be a very lucrative pick in 2022; at a time when the retail sector had collapsed by ~32%, and the benchmark index had given up ~18% of its value, DDS stood out, delivering returns of 37%!

YCharts

Whilst DDS has been a rewarding pick in 2022, I’m not sure it can carry its momentum into 2023. Here are some of my concerns.

Unappealing outlook

While Dillard’s has exposure to quite a few product categories, apparel is the dominant category accounting for ~53% of the company’s business over the last nine months. With a recession around the corner and the personal savings rate of 2.4% well below even pre-pandemic levels, customers are likely to be even more discerning with their discretionary spending. In an uncertain economic environment such as this, it’s difficult to go gung-ho over apparel purchases.

Apparel inventory is largely sourced from external shores, and recent data already shows that US apparel imports have begun to slow substantially. Separately, note that in-store clothing sales in the US have begun a declining trend after months of growth.

YCharts

With Dillard’s per se, there are signs that it is losing some momentum. For instance, Black Friday, footfall sales showed that the company faced the steepest decline (relative to the pre-pandemic level) amongst all its peers (down by 36%, whilst the likes of Macy’s, Kohl’s, and Nordstrom saw declines in the range of 26-29%). I also think investors should ponder if Dillard’s can deliver ample comp growth when it’s due to come up against a very high base effect in the January and April quarters (In the Jan-22 quarter, comparable retail sales had grown by 37%, and in the April-22 quarter it had grown by 23%).

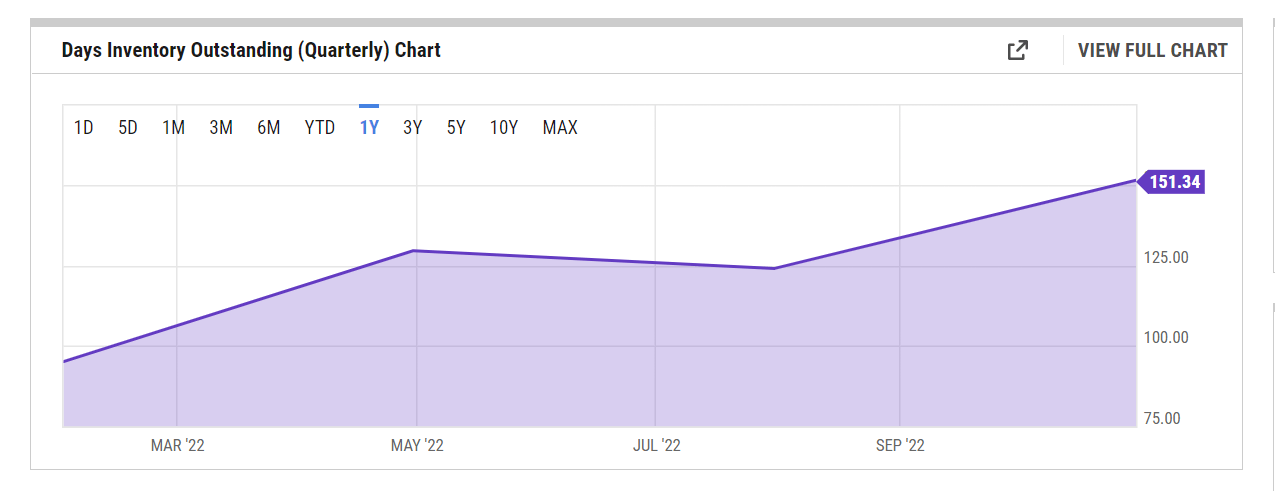

Mckinsey believes that cost pressures that were seen in the second half of ’22 across the fashion industry will likely persist through 2023. According to a survey carried out by the institute, 97% of the respondents stated that COGS and SG&A would continue to rise in 2023. Dillard’s has already been seeing some gross margin declines on an annual basis; in Q2-22 retail gross margins were down by 20bps, and in Q3-22, they fell by a greater margin of 100bps! Looking ahead, I believe gross margin pressures could continue to linger, as the company still has a lot of inventory on its balance sheet that will need to be unwound at promotional rates. Note that the inventory days continue to trend up and are currently at their highest point since Q3-20.

YCharts

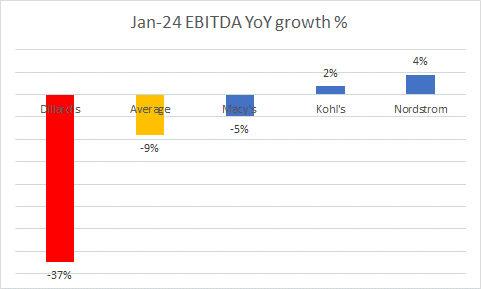

All in all the operating backdrop of Dillard’s doesn’t look too appealing. According to YCharts consensus estimates, Dillard’s offers the weakest EBITDA growth runway over the next year; whilst other department peers will likely witness 9% YoY attrition (on average), in their January 2024 EBITDA values, DDS will fare a lot worse with an expected annual decline of -37% (FY24 EBITDA of $782.4m). Meanwhile, the likes of Kohl’s (KSS) and Nordstrom (JWN) will see positive EBITDA growth of low to mid-single digits.

YCharts

Pricey valuations and limited yield

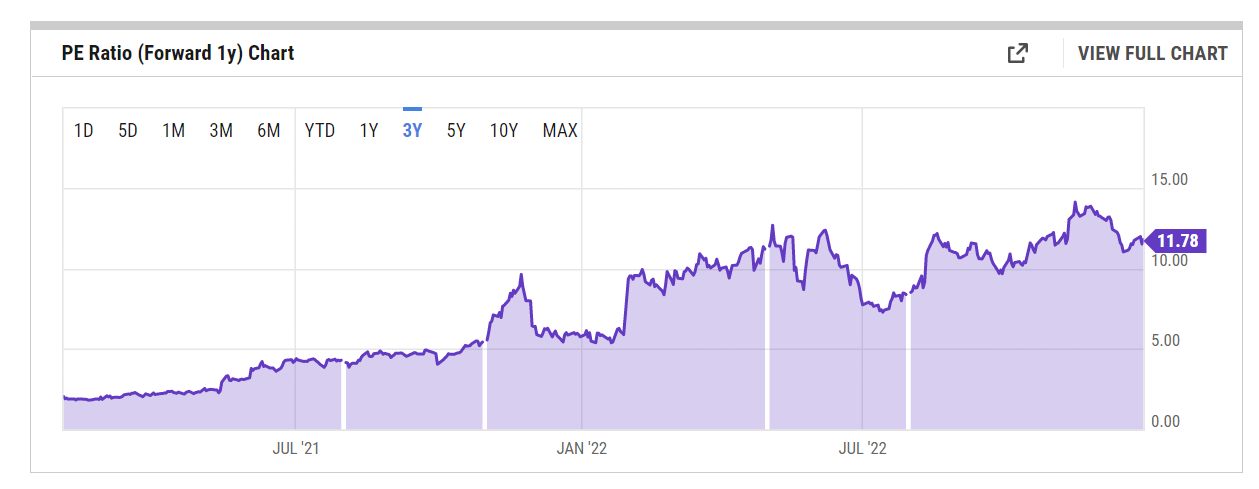

Long-standing owners of the Dillard’s stock will note that management has a history of engaging in buybacks to make the valuation picture more palatable; for instance, as of 9M-22, shares outstanding have decreased by 16% in just one year. Yet, despite a sizeable attrition of the share count, current forward P/E valuations of Dillard’s look quite exorbitant. Relative to its 5-year forward P/E average of 7.26x, the stock currently trades at a ~62% premium.

YCharts

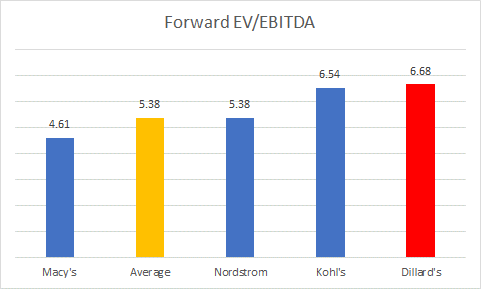

If you want to play down the EPS effect on account of the diminishing share count and switch to the EV/EBITDA metric which negates this effect, things don’t get any better.

I previously touched upon Dillard’s adverse EBITDA outlook for the year ending January 2024, and this weighs on Dillard’s EV/EBTIDA valuations making it the priciest amongst its department peers, with a forward EV/EBITDA multiple that is 25% higher than the peer set average.

YCharts

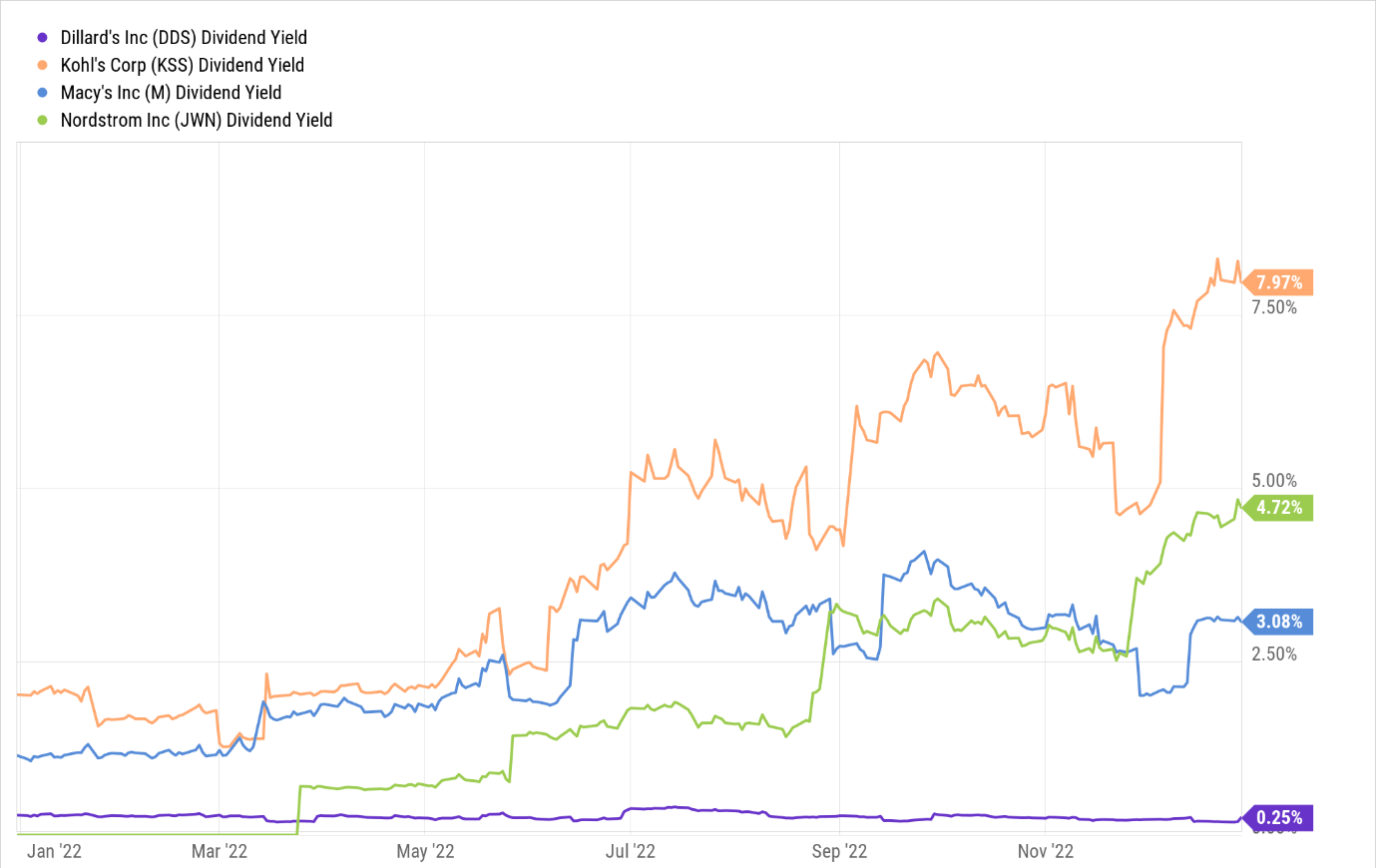

Finally, at the current share price, you also have to consider the yield, which is quite a pittance, particularly when you consider that other peers offer yields within the range of 3-8%.

YCharts

Poor risk-reward on the charts

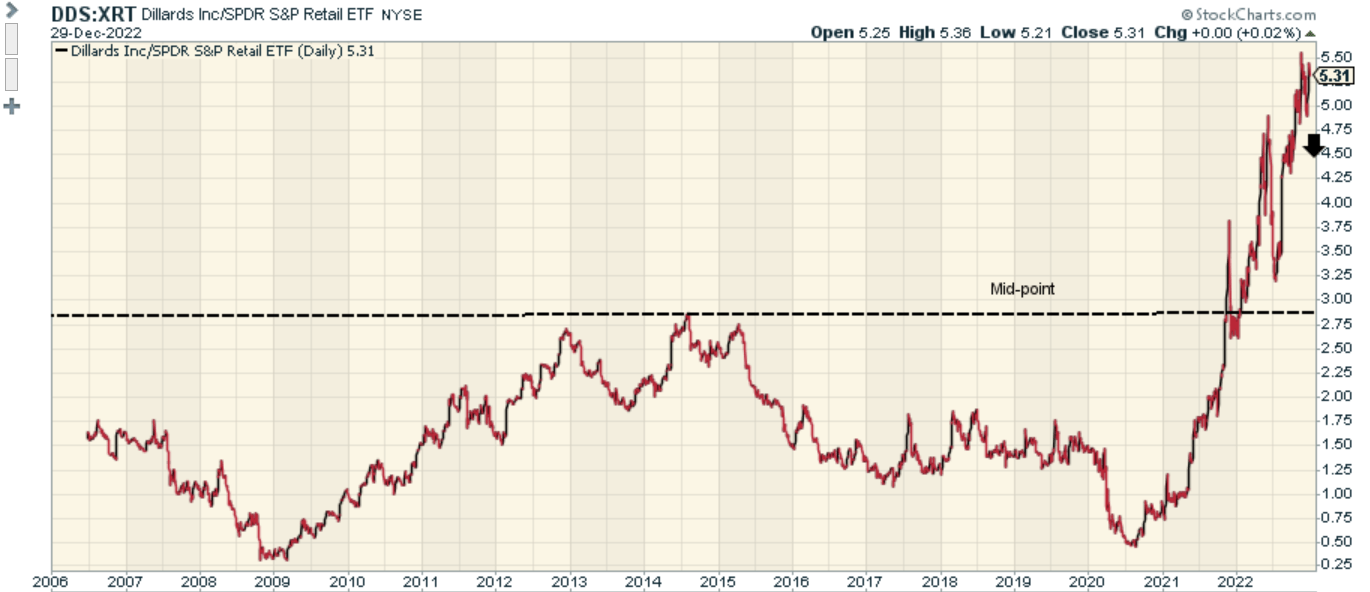

After delivering solid returns of around 37% this year, one has to wonder if there’s further juice left in the DDS stock, particularly as it currently looks enormously overbought relative to its peers from the retail space, as represented by the SPDR S&P Retail ETF (XRT); note that the relative strength ratio of DDS and XRT (5.31x) is a good 84% higher than the mid-point of its long-term range. If you’re someone who believes in the notion of mean-reversion, you would think investors would rotate out of Dillard’s into other retail options which offer better risk-reward.

Stockcharts Investing

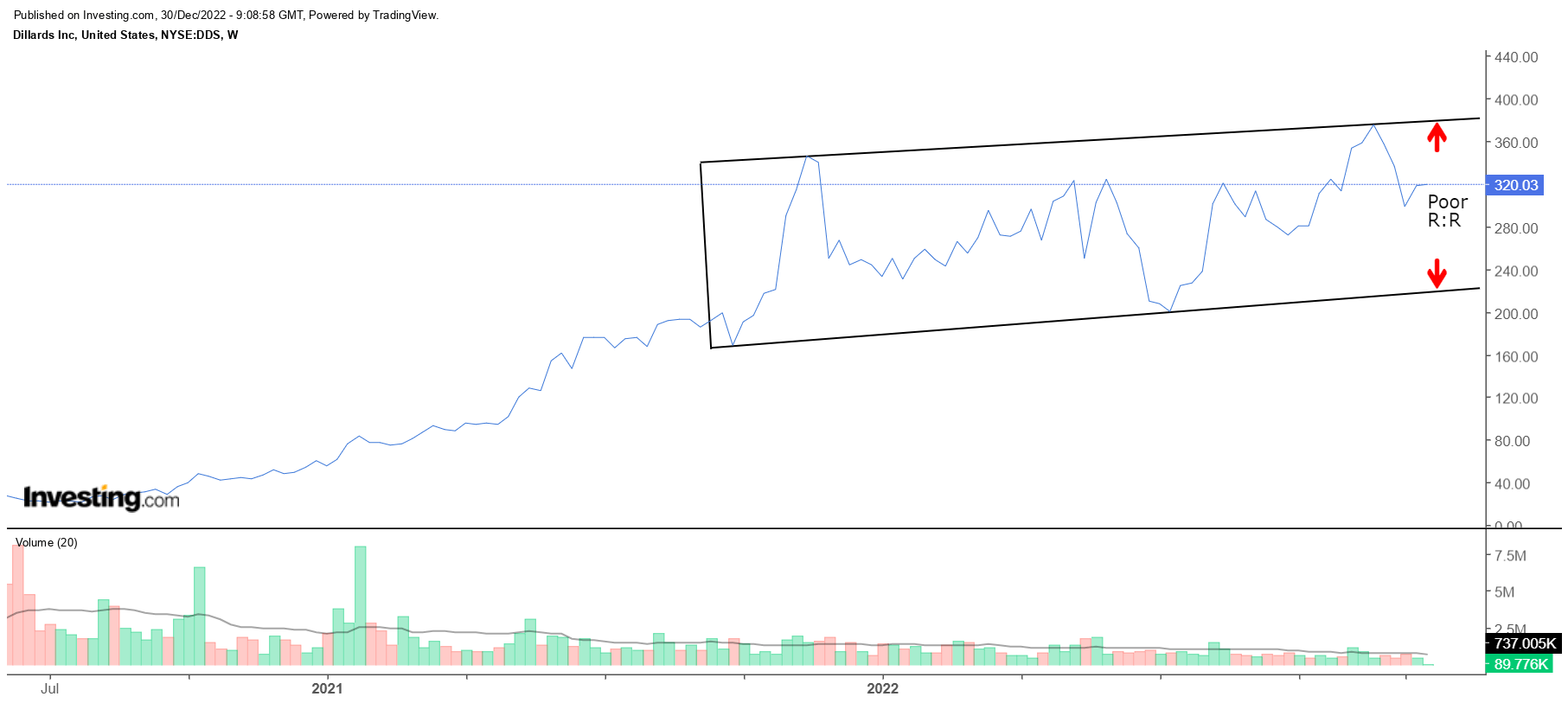

On the standalone weekly chart, we can see that since Q4-21, the stock has been chopping around within a slight ascending channel. If you’re thinking of going long, it’s difficult to get too excited about the risk-reward on offer at the current price levels, as the price is currently a lot closer to the upper boundary of this channel (around the $370 levels) than the lower boundary (around the $220 levels), implying weak risk-reward of 0.5x.

Be the first to comment