Qualcomm headquarters sign in San Diego, California, USA. JHVEPhoto/iStock Editorial via Getty Images

Editor’s note: Seeking Alpha is proud to welcome MarketXLS as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Qualcomm, Inc. (NASDAQ:QCOM) appears to be trading at value lower than its intrinsic worth, and is expected to benefit from long-term developments such as 5G technology and the creation of virtual worlds. Despite the typical downturn in the semiconductor industry, the company has achieved strong financial performance in the fourth quarter. In this article, we will comprehensively analyze Qualcomm’s fundamental factors and utilize three distinct valuation techniques to determine a fair value estimate for the company. Our analysis will consider various financial and operational metrics to arrive at a well-rounded assessment of the company’s worth. We aim to provide a more thorough and reliable estimate of Qualcomm’s fair value by applying multiple valuation methods.

Qualcomm is a global semiconductor and technology company that provides a wide range of products and services for the mobile, automotive, and IoT markets. It is headquartered in San Diego, Calif., and was founded in 1985. Qualcomm is known for its pioneering work in developing 3G, 4G, and 5G wireless technologies. It is a leading provider of many mobile devices’ chipsets, modems, and other hardware components. The company also licenses its intellectual property to other manufacturers and operates several businesses in digital media and automotive areas. Qualcomm has a market capitalization of over $100 billion and is a constituent of the S&P 500 index. In addition, Qualcomm is known for its innovations in wireless technology, including the development of the first commercial CDMA-based cellular technology and the first mobile processor with a one gigahertz clock speed.

Qualcomm has a wide range of products and services, which can be broadly divided into four main categories:

Wireless Communications

Qualcomm is a leading provider of chipsets, modems, and other hardware components for mobile devices such as smartphones, tablets, and laptops. It also offers a range of software and services related to wireless communication, including 5G technology and the Internet of Things (IoT).

Licensing

Qualcomm licenses its intellectual property to other companies, including patents related to its wireless technology and other technology innovations. This is a significant source of revenue for the company.

Digital Media

Qualcomm is involved in developing and distributing digital media products and services, including video and audio content and technology for streaming and distributing media over the internet.

Automotive

Qualcomm is involved in developing technologies for the automotive industry, including advanced driver assistance systems (ADAS) and telematics. It also offers products and services for connected cars and electric vehicles.

Qualcomm’s products and services are focused on enabling wireless communication and providing solutions for various industries.

Background and Estimations

The company experienced a slowdown in demand for mass-market handsets in the consumer IoT market. The weakening of demand got further exacerbated by the deterioration of the macroeconomic environment, including continued COVID-19 restrictions in China.

In calendar year 2022, there was a decline in handset demand of at least 10% over the previous year. In addition, there has been an increase in channel inventory due to the rapid deterioration in demand and the ease of supply constraints across the semiconductor industry.

Due to these elevated levels, the most prominent customers had effectively altered their inventory policies. As a result, they drew and are drawing down their inventory, and the company’s near-term financial performance got negatively affected.

It is estimated that the channel has had elevated inventory levels for approximately eight to ten weeks. However, the situation may take several quarters to resolve because of the environment’s dynamic nature. As a result, more than half of the inventory drawdown will be completed during the first quarter of the upcoming fiscal year.

To manage spending levels, the company has implemented specific measures. These include freezing hiring and reducing spending on handsets, other mature product areas, and general and administrative expenses. In addition, optimizing R&D investments is being undertaken to focus on the growth of the automotive and IoT industries.

Depending on how the macroeconomic environment develops shortly, further action might be taken to reduce operating expenses.

Financials

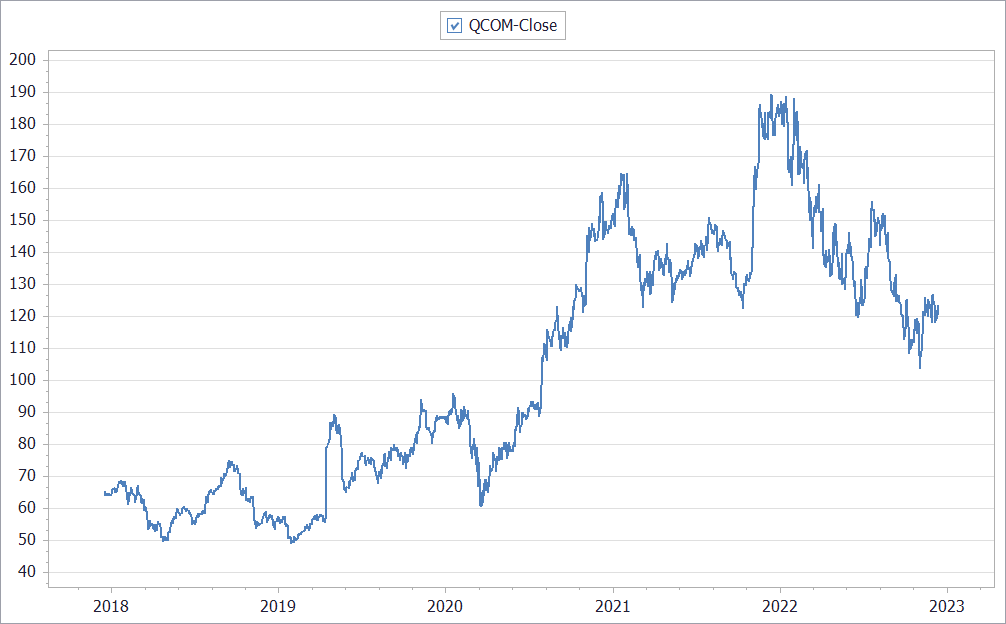

Qualcomm’s stock price has more than doubled over four years, from $56.91 at year-end 2018 to $121.21 as of Dec. 15, 2022, owing to a significant increase in revenue each year. The growth has resulted from expansion into chips for automobiles and IoT devices.

Share Price (MarketXLS)

Source: Created by author

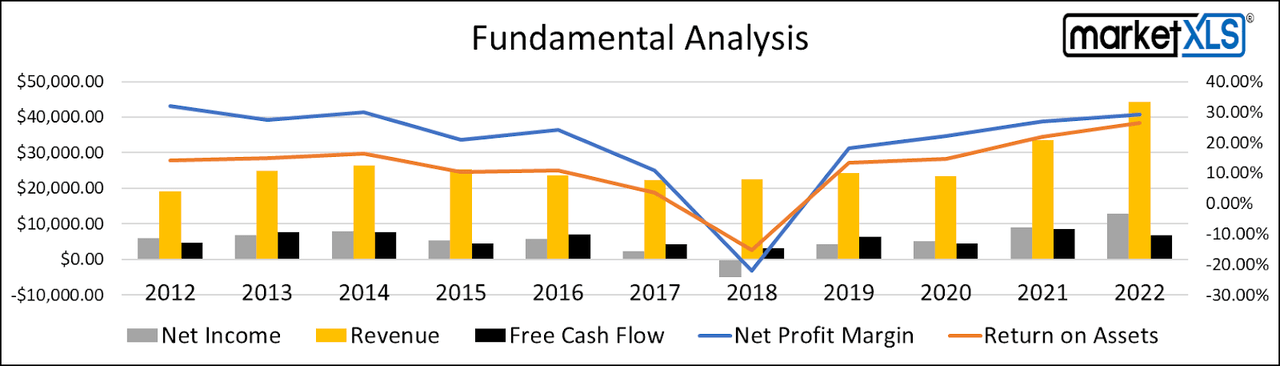

In the past four years, the company’s revenue has been growing at an average rate of 19.66%. As a result, the company’s debt/equity ratio has significantly improved from 20.29 in 2018 to 0.86 in 2022. Free cash flow has also almost doubled in the same period.

Fundamental Analysis (MarketXLS)

Source: Created by author

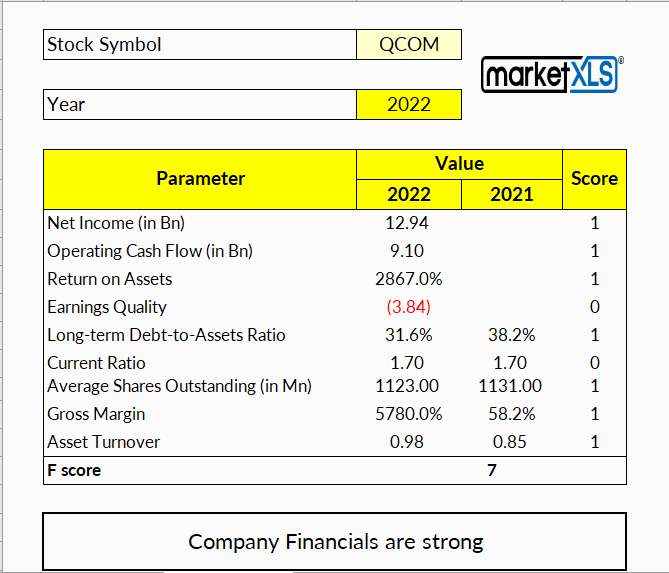

The company has an F-Score of seven out of nine, indicating that the financials are strong. Financial investors use this score to find the best-value stocks (nine being the best). It is calculated based on key financial metrics like return on assets, operating cash flow, current ratio, asset turnover ratio, and gross margin.

F Score (MarketXLS)

Source: Created by author

Future Outlook

According to data from market research firm Data Bridge, the 5G smartphone chipset industry is expected to experience a compound annual growth rate of 49% through 2028, reaching a size of more than $2.5 trillion. Qualcomm, a leading provider of chipsets for 5G technology, is well-positioned to benefit from this growth. In fiscal 2022 (ended Sept, 25th), the company generated 66% of its revenue, or $25 billion, from handsets. In addition, while Qualcomm has forecasted negative sales growth for the upcoming quarter in the handset industry, the overall growth is expected to make any slowdown temporary. As a result, Qualcomm’s leadership in the 5G smartphone chipset market is expected to drive strong performance for the company in the coming years.

Recently, Volkswagen (OTCPK:VWAGY) set up a years-long partnership with Qualcomm to develop automated driving technology, with the contract set to run until 2031.

Valuations

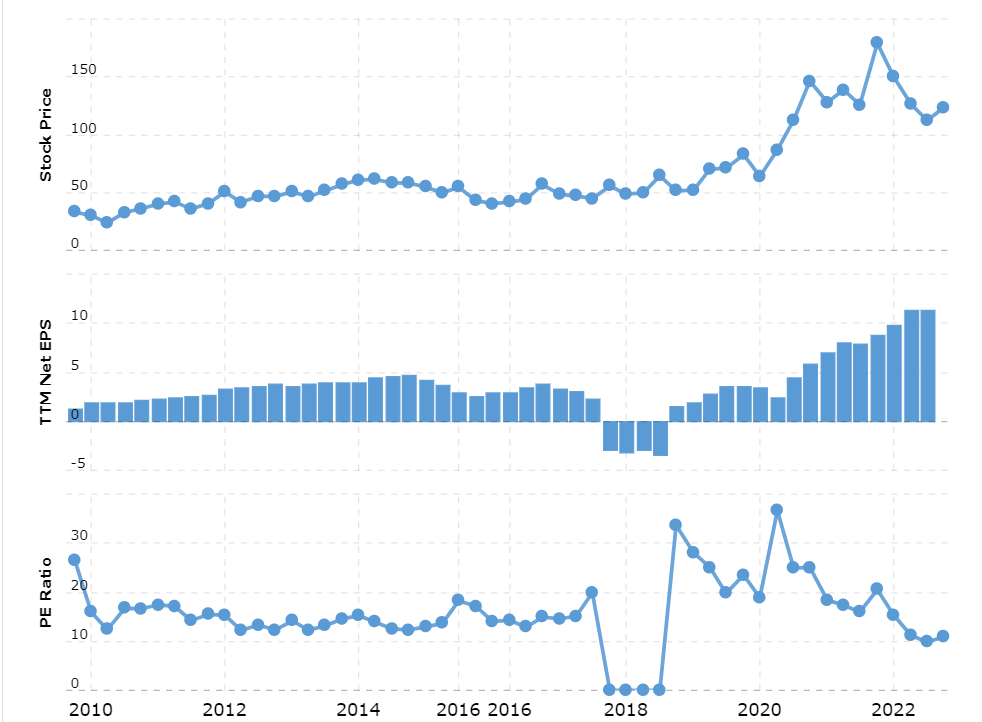

Qualcomm, a global leader in wireless technologies and mobile data solutions, has seen a tough year in the stock market. Over the last 12 months, the stock has dropped by 33% and has continued to underperform, despite the company reporting solid revenues and net profit growth for the current quarter.

One of the key factors contributing to Qualcomm’s underperformance is the continuous rate hikes by the Federal Reserve, which have led to a deteriorating market environment. Additionally, the company missed its earnings per share (EPS) guidance by approximately $0.80, further weighing on investor sentiment.

Qualcomm analysis by Macrotrends (Macrotrends)

Source: Macrotrends

However, we believe that Qualcomm’s long-term growth prospects remain strong and that the company is well-positioned to weather the current market challenges. Therefore, let’s perform different valuation techniques to estimate Qualcomm’s fair value.

P/E Multiple Valuation:

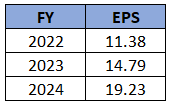

According to a recent analysis, the company’s EPS has grown at a quick pace of 20.2% over the last 12 years and has grown at an impressive rate of 57% over the last four years. Based on our analysis, Qualcomm’s EPS growth rate may slow down in the coming quarters but is still expected to grow at around 30% over the next two years. If these projections hold, the company’s EPS for the fiscal year 2024 could be around 19.23.

PE Valuation (MarketXLS)

Source: Created by author

Using a conservative price-to-earnings (P/E) multiple of 15, below the company’s historical median P/E of 18, Qualcomm’s share price could reach $288.48 in the next few years. Even with a discount rate of 10%, the company’s current share price could be around $238, representing a significant potential upside for investors.

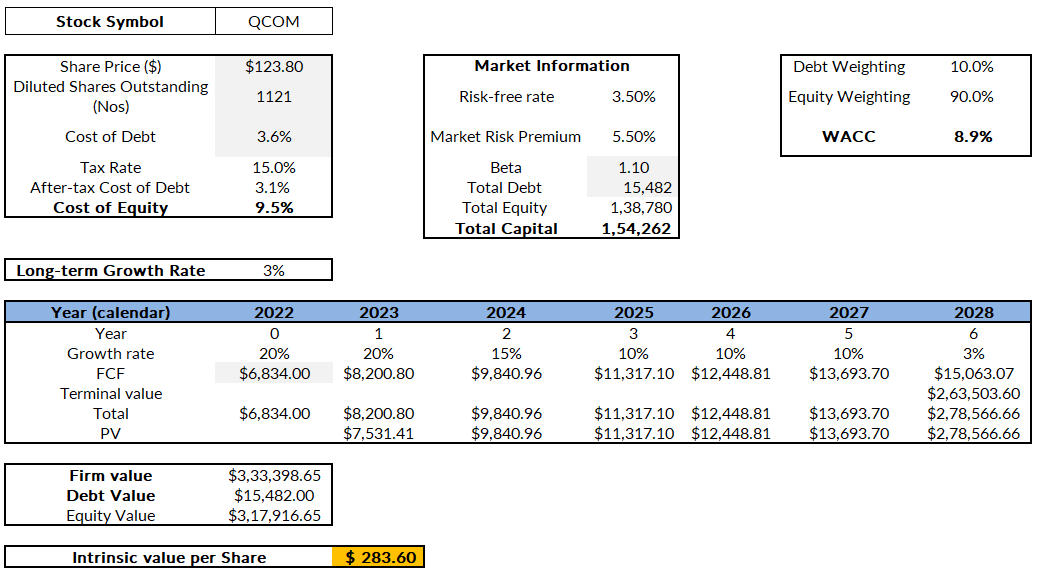

DCF Valuation:

A couple of assumptions have been made by us to perform this DCF valuation.

-

Risk-Free Rate: Looking at the current market, we have assumed it as 3.5%.

-

Market Risk Premium: According to our assumptions, it would be about 5.5%.

- Free Cash Flow Growth Rate: We have assumed the growth based on industry and company outlook.

DCF Valuation (MarketXLS)

DCF Valuation Model (MarketXLS)

Source: Created by author

Based on the assumptions stated above, we undertook a DCF analysis and, even with such a conservative growth figure in free cash flow, the intrinsic share value comes out to be $283.60.

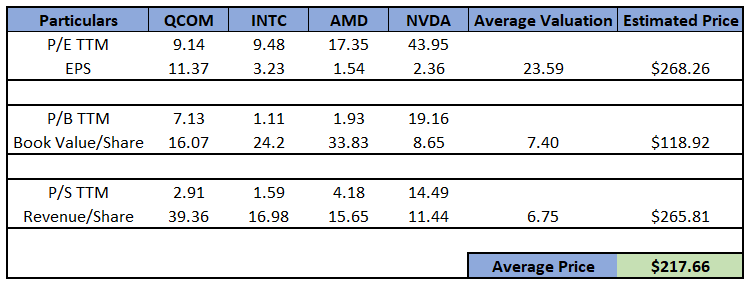

Peer Valuation:

We compared the P/E ratio, price/book ratio, and price/sales ratio of Qualcomm with Intel Corporation (INTC), Advanced Micro Devices Inc. (AMD), and NVIDIA Corporation (NVDA). Then, we took the peers’ average and extrapolated it to the financials of QCOM.

Peer Valuation (MarketXLS)

Source: Created by author

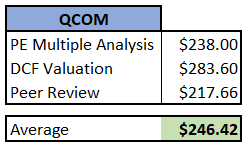

After all the valuation models calculations, Qualcomm’s fair value turns out to be $246.42, showcasing the company’s potential in the future.

Qualcomm fair value (MarketXLS)

Source: Created by author

Overall, while Qualcomm has faced some challenges in the short term, its solid fundamentals and growth prospects make it a compelling investment opportunity for the long term.

Risks

As a leading provider of semiconductor products and technologies, the company faces several risks that could potentially impact its business. One risk is the possibility of customers choosing to vertically integrate and develop their own integrated circuits, which could lead to competition for Qualcomm. Another risk is the high concentration of Qualcomm’s business in China, which exposes the company to potential impacts from trade and national security tensions between the U.S. and China. Qualcomm’s operations and business could be at risk from security breaches or misappropriation of its technology, intellectual property, or other proprietary or confidential information. Finally, Qualcomm’s reliance on a few key customers and its heavy dependence on China for revenue (with 63.61% of its revenue coming from the country in the recent financial year) makes the company vulnerable to shifts in demand or changes in customer preferences.

Conclusion

Qualcomm has grown leaps and bounds in the past decade, achieved $44 billion in revenue, and commands $138 billion market capitalization. It appears to be a lucrative long-term investment as the company transitions from smartphones to automation and the IoT. The 5G upgrade cycle in the handset segment should continue to benefit Qualcomm. In addition, the company is expected to benefit from the CHIPS Act, which provides funding for semiconductor research and development in the U.S.

We have determined Qualcomm’s fair value as $246 per share based on our analysis of its financial data on various valuation models. As a result, it offers an excellent investment opportunity with a time horizon of two years.

Be the first to comment