Andrii Chagovets/iStock via Getty Images

Data I/O (DAIO) is the leader in programming equipment for chips, which positions it very well to profit from secular growth tailwinds but these secular winds are at times overpowered by more cyclical downturns.

That is what happened the last couple of years but we already noted in our previous article that the cyclical downturn is abating, and Q3 results show that the secular growth story is reasserting itself.

DAIO IR presentation

Here are the main secular tailwinds:

- Ever more chips are going into ever more things, with 5G being a main catalyst for the IoT market where chips-infused intelligence makes analog objects digital and amenable to data analytics.

- Chips become more complex

- This holds especially for their largest segment, automotive (63% of orders YTD), cars are increasingly becoming driving computers (see picture below).

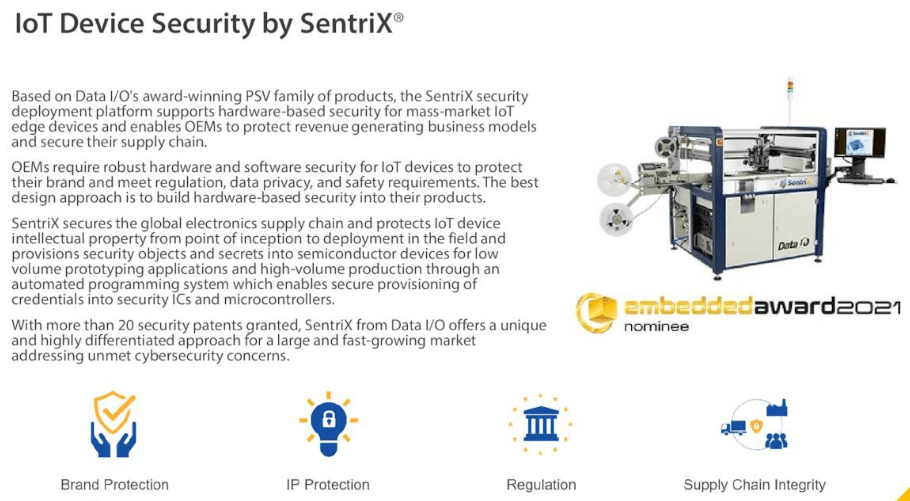

- Security concerns are increasing with the multiplication of touch points on the internet powered by 5G and the IoT revolution, which is a secular tailwind for Data I/O’s SentriX secure provisioning solution.

Automotive

Their main segment is automotive, and that’s simply the result of ever more electronics going into cars, which have become veritable computers on wheels.

DAIO IR presentation

This trend is set to continue, driven by electrification and autonomous driving.

DAIO IR presentation

The company has also anticipated the shift in automotive towards UFS memory, which is rapidly becoming the new standard with their LumenX platform with VerifyBoost technology, which (Q3CC):

delivers verified performance up to 750 megabytes per second on high-speed Gear 3 by two lane support for UFS 3.1 devices…LumenX programmers within our PSC programming systems deliver up to 4.5x improvement in programming performance and reduce the total cost of programming by up to 39% while using VerifyBoost.

Existing systems can be upgraded with these capabilities.

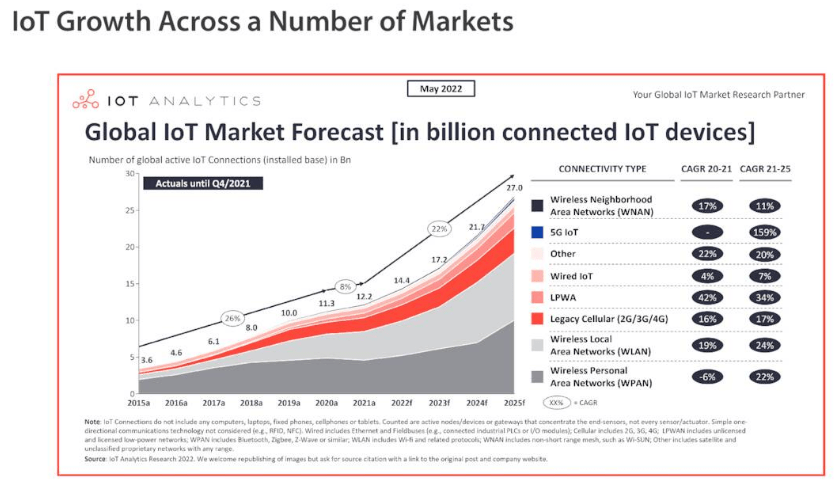

Internet of Things

Security concerns are increasing with the multiplication of touch points on the internet powered by 5G and the IoT revolution, which is also set for rapid multi-year growth:

DAIO IR presentation

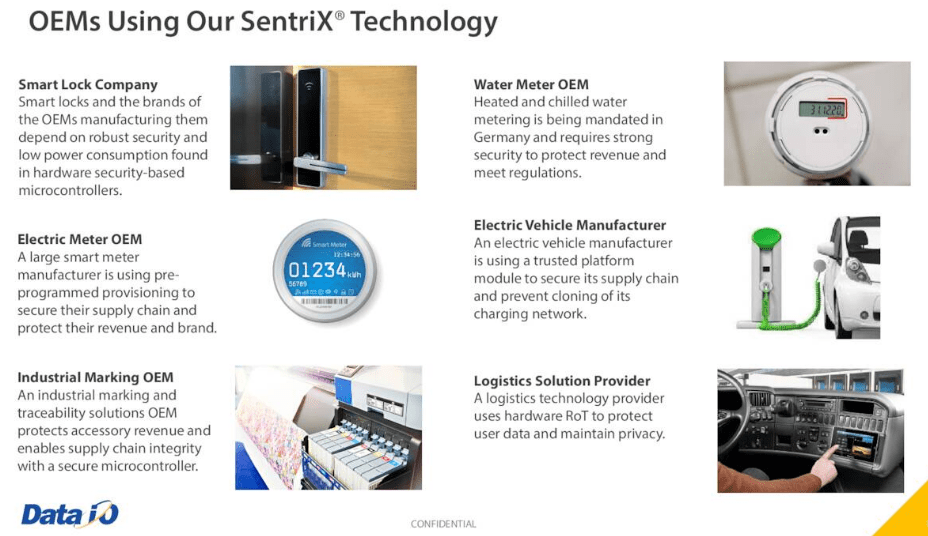

This is fertile ground for the SentriX providing secure provisioning:

DAIO IR presentation

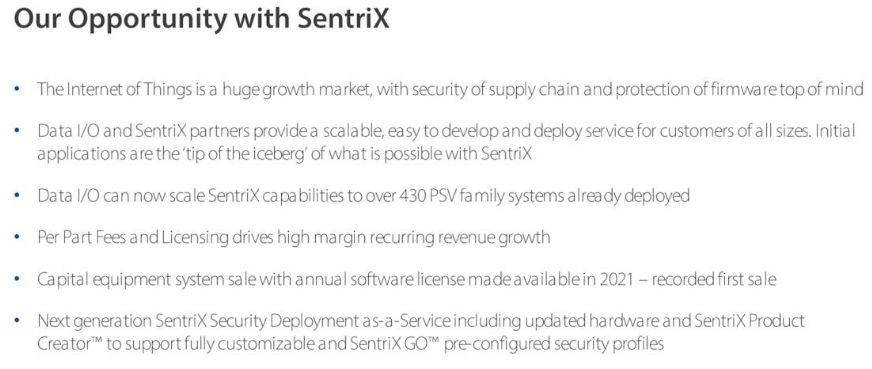

After a slow start demand for the SentriX is gaining traction:

DAIO IR presentation

This is good to see as we expected much more from the uptake a couple of years ago, but there were some teething issues, its use was complex and the company enabled prospective clients to pay for SentriX services out of OpEx instead of having to make a capital investment and purchasing the machines outright.

It is difficult to say how much this is going to add to revenues as they don’t split out the results, but given the IoT TAM and security concerns, there can be little doubt that the market opportunity is substantial. Management concurs:

DAIO IR presentation

Cyclical nature

The secular tailwinds get pushed to the background at certain intervals by cyclical downturns. However, we think diversification of their customer base, as well as a change in the business model for SentriX (allowing forms of pay-per-use), should lessen these over time.

The present cyclical upturn was long in the making and haphazard as it got upended by multiple one-time issues like the pandemic, supply chain problems, the war in Ukraine, and Chinese lockdowns.

The easing of the latter, more especially the easing of the lockdown of Shanghai at the end of Q2 provided a major boost to Q3 figures, so once again it seems that the cyclical upturn is materializing.

Financial results

| Q3 | Q4 | Q1/21 | Q2 | Q3 | Q4 | Q1/22 | Q2 | Q3 | |

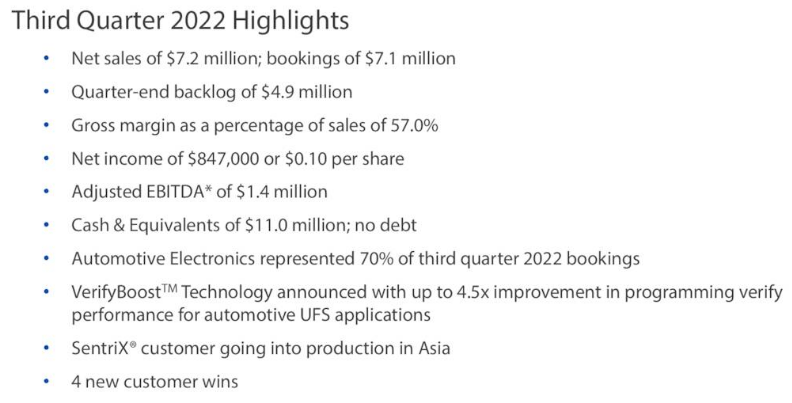

| Sales | 5.9 | 4.9 | 6.0 | 6.7 | 6.7 | 6.4 | 5.0 | 4.8 | 7.2 |

| Bookings | 5.6 | 6.0 | 5.4 | 8.9 | 5.0 | 6.2 | 6.2 | 6.4 | 7.1 |

| Backlog | 2.8 | 3.9 | 3.0 | 5.0 | 3.3 | 2.9 | 4.1 | 5.8 | 4.9 |

| Gros Marg | 55 | 52.9 | 55.5 | 57 | 60.7 | 54.4 | 46.4 | 57.8 | 57 |

| Adj. EBITDA | 169K | -194K | 173K | 597K | 564K | 117K | -932K | -64K | 1.4 |

DAIO IR presentation

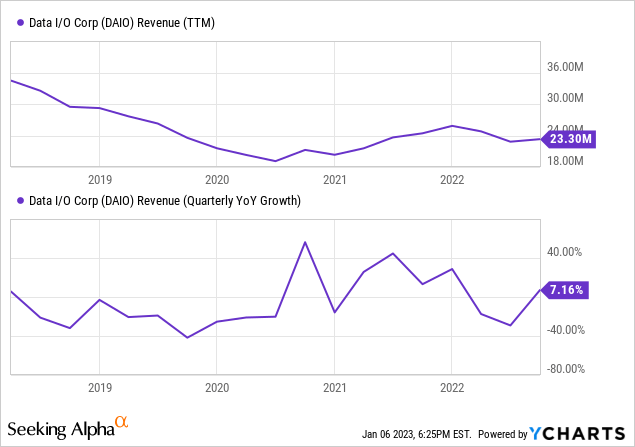

Revenue is still quite a long way off from the previous cyclical high, which is a little surprising. What’s less surprising is the erratic quarterly growth, given all that has gone on in the economy over the last several years:

Since 90%+ of revenue comes from outside the US the performance is even more remarkable given the strong dollar, especially the euro and yuan.

While the Americas and Asia were strong the whole year Europe showed a marked recovery despite the prevailing macro headwinds in Q3 so the company is now doing very well in all of its main regions.

Automotive was even stronger than usual, with 70% of bookings in Q3 coming from this segment versus 63% YTD. The segment gained 4 new customers, making 16 new customers YTD.

The company has $5.2M in deferred revenue (at $300K which has already been shipped in Q4) and backlog ($4.9M) which is higher than usual and management argues it will ship in Q4, on top of the new orders they gain and ship in Q4.

The company sold 16 PSV systems in the quarter.

The pay-per-use SentriX business model is likely to produce a jump in revenue as a big customer is going into production.

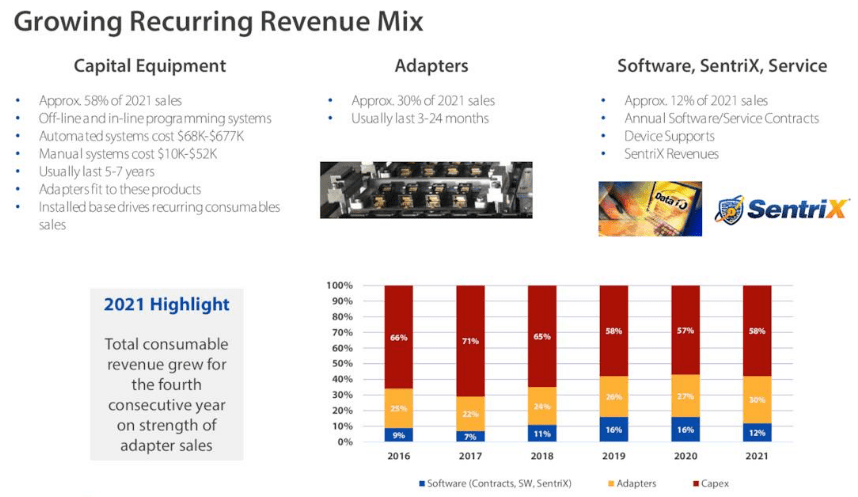

Consumables are 32% of revenues YTD (vs 30% 2021), and software and services are 12% of revenues YTD (unchanged). Then there is the case that increasing the installed base of equipment automatically increases the demand for adapters, which are recurring revenues, which are creeping up as a percentage of revenues:

DAIO IR presentation

Cash

The company had $11M in cash at the end of Q3, an increase of $700K versus the previous quarter. The company also has $13M in NOLs, and no debt.

Risk

The company might become too dominant in its main segment, automotive. There are few major automotive OEMs that are not using the company’s systems, so there are fewer new clients to win.

Management argued that 250+ of their 430 PSV systems in the field are focused on the automotive market, but they did actually win 4 new automotive customers in Q3 and 16 YTD.

So this obviously doesn’t mean there won’t be growth from this segment, or even that new customers will dry up.

There are still the tailwinds from ever more chips going into cars, and these being ever more complex, and with autonomous cars, the touch points with the internet will proliferate and increase the need for secure programming.

So programming needs will still rise at a double-digit rate (probably 20%+) interlaced with the occasional cyclical downturn, it’s just that there aren’t all that many new car manufacturers to win. Indeed, management remains very upbeat about their main segment (Q3CC):

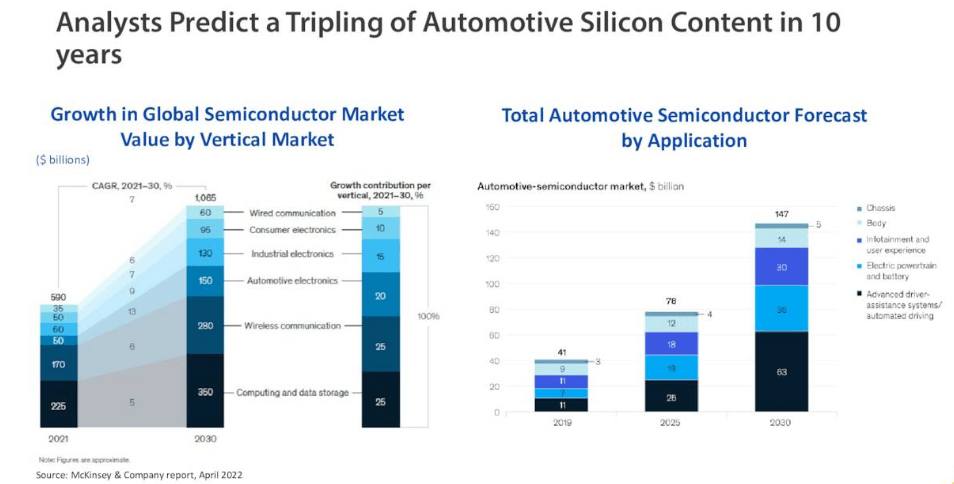

These overall trends on demand reinforce our long-term view of a tripling of the automotive semiconductor market by 2030 with automotive memory growing at an even faster rate

The main risk is of course another cyclical downturn, which is always possible, inevitable even. However, apart from little signs that the secular tailwinds are going to abate anytime soon, there are some mitigating factors that have some dampening effect on a cyclical downturn:

- With chips going into ever more things we expect the dominance of the automotive sector to gradually subside, and with a greater variety of clients from different markets, there will be greater variability in cycles, mitigating the cyclicality of demand.

- An increasing installed base of machines increases recurring revenues, which should blunt the cyclicality at least a little.

- The SentriX isn’t necessarily sold but can be used by clients on several forms of pay-per-use basis, smoothing out otherwise discrete CapEx cycles.

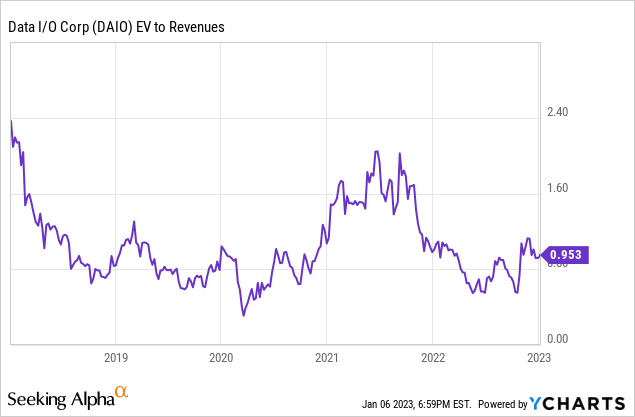

Valuation

This is an interesting graph because it shows that the stock could run significantly on a cyclical upturn. Not only would that mean much higher revenues, the stock could also get a boost from a valuation multiple expansion like in the previous cyclical upturn (in 2017-18).

The company produced a huge earnings surprise in Q3, EPS coming in at $0.10, which was $0.25 better than expected. Despite that, YTD earnings are still negative

Conclusion

The shares are promising for a number of reasons:

- The company is the market leader and has a strong technological basis.

- The company is benefiting from multiple secular tailwinds, as more and more complex chips go into ever more stuff, especially automotive and the IoT.

- IoT security concerns are a secular tailwind for the company’s secure provisioning platform, the SentriX.

- The company has a strong balance sheet with $11M in cash, $13M in NOLs, and no debt.

- Recurring revenues are gradually rising as a percentage of revenues.

- Q3 provided a huge positive surprise on both revenues and profits, which could finally mark the start of a cyclical upturn

- The shares aren’t terribly expensive.

On the other hand:

- The company still depends 60% on CapEx from clients, it’s a cyclical market even if there are forces to slowly blunt its impact.

- Despite the strong secular tailwinds and the SentriX, which was only introduced a couple of years ago, revenues are still well below the previous cycle top.

- Whilst Q3 results are promising, it’s too early to rejoice, especially considering what’s going on in the economy.

- We need more than one quarter with positive earnings to confirm a cyclical upturn, there have been a few false dawns in recent years.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment