Bradley Caslin

After our follow-up analysis on Air France-KLM (AFRAF; AFLYY), it is now time to comment on Deutsche Lufthansa’s (OTCQX: DLAKF, OTCQX: DLAKY) quarterly performance.

The German national carrier benefited from a rebound in demand in its passenger business but also and above all thanks to the cargo division.

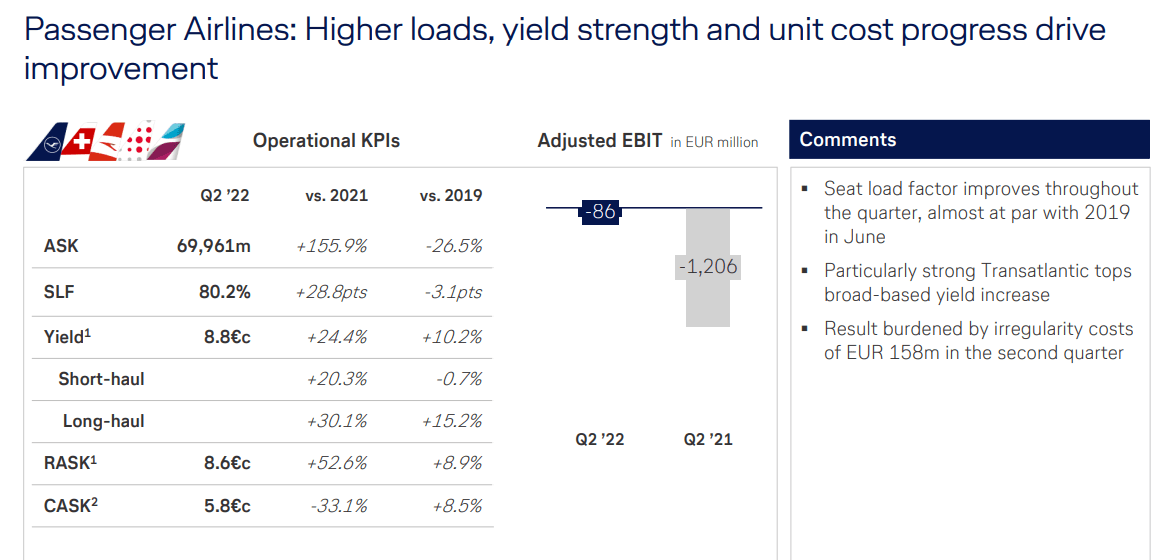

29 million passengers traveled with the Group’s airlines in the second quarter compared to 7 million over the same period of the previous financial year. Faced with strong demand, the company continued to expand its capacities in the first half. Over the three months to the end of June, the capacity offered was around 74% of the pre-crisis level, while the load factor stood at 80%. In premium classes the load factor also reached 80% in the second quarter, exceeding the level of 2019 (76%), stimulated by a still high demand among ‘leisure travelers’ and an increase in the number of reservations among business travelers.

In the first semester, top-line sales significantly increased to €13.8 billion versus the €5.8 billion recorded in the same period of 2021. Thanks to “continuous and consistent” cost management actions and the expansion of flight capacity, the company’s airline unit costs fell 33% in the second quarter compared to the same period last year. However, these costs remain 8.5% above the pre-crisis level and despite the strong results, the passenger activity business still suffered an operating loss of €86 million in the second quarter versus a minus €1.2 billion recorded a year earlier. Looking at the three-month period, the group’s net profit reached €259 million against a loss of €756 million. This is the first result in green since the outbreak of the health crisis and was supported by the record number achieved by the freight division.

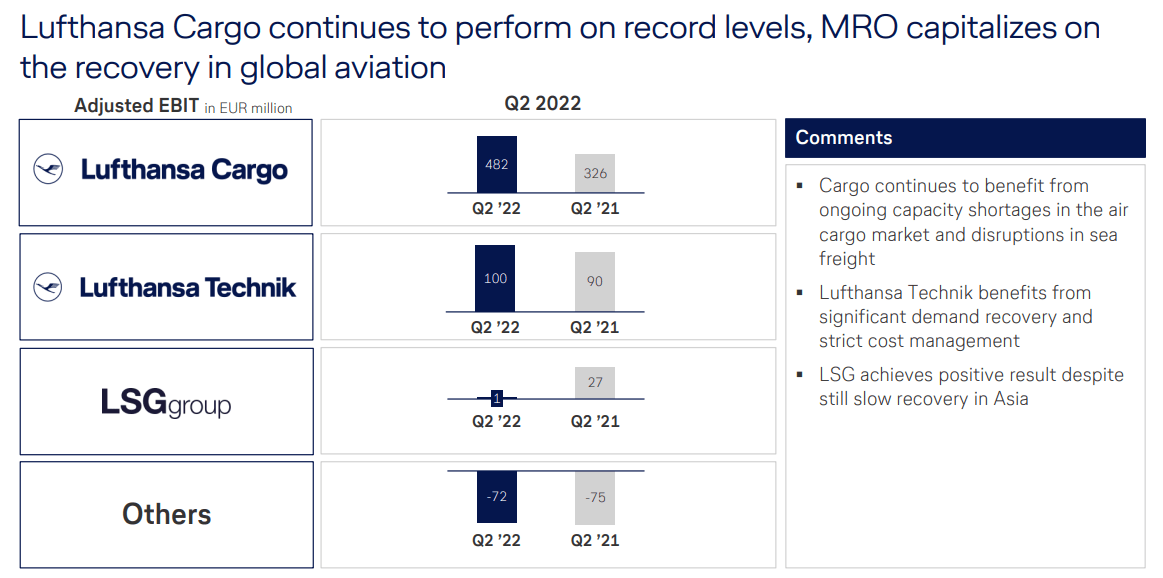

CARGO Division (Deutsche Lufthansa Half-year Results)

More in detail, Deutsche Lufthansa was impacted by cancellations and delay costs in the quarter. This negative one-off impacted the group by a total amount of €158 million. As we already mentioned in the Air France-KLM analysis, this outcome happens for “the operational difficulties imposed by some airports such as London Heathrow and Amsterdam Schiphol”. More important to note is the fact that airline companies “increased the fares of air tickets, and this will drive future underlying profitability. Consequently, airline companies have attributed these inconveniences mainly to airports. However, airlines have been accused of selling airline tickets despite knowing that flights could not be made, causing inconvenience to customers. If this is proved by the competent authorities, airline companies might be exposed to pretty high fines”.

Passenger Financial Results (Deutsche Lufthansa Half-year Results)

Given the high level of new bookings and structural improvements in working capital management, the adjusted free cash flow was significantly positive, reaching €2.1 billion compared to the €382 million recorded a year earlier. Thanks to the supportive cash flow generation, Deutsche Lufthansa was able to further reduce its debt burden (by more than €2 billion) and also reduce its pension fund obligation.

Conclusion

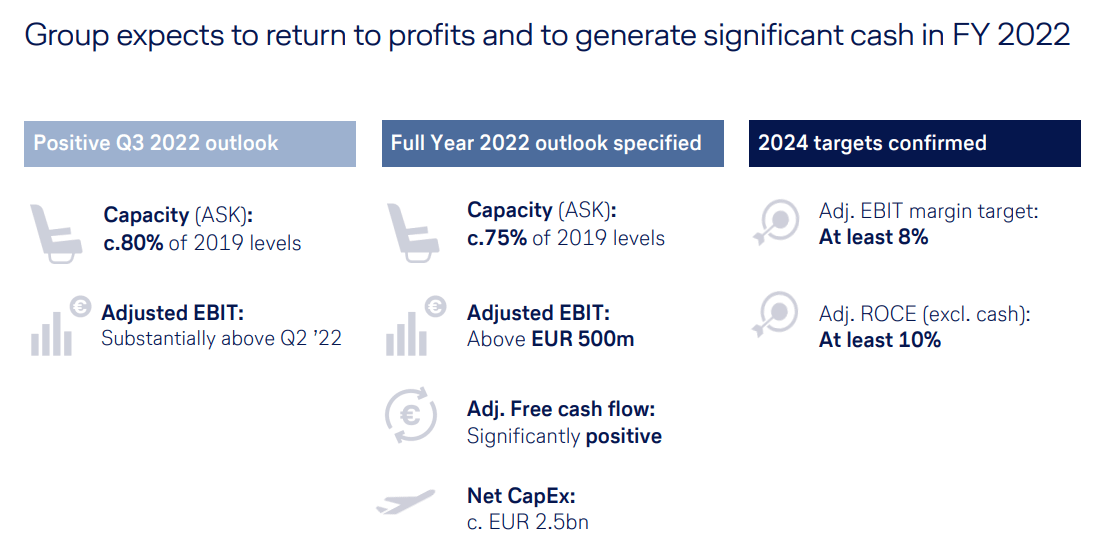

Lufthansa expects its profits to continue to rise in the coming months amid booming demand, even as staff shortages prompt airports to limit capacity. Bookings for the months of August to December 2022 currently average 83% of the pre-crisis level. Despite the need to cancel some flights to stabilize operations, the company will continue to increase capacity based on demand and expects to offer around 80% of its pre-crisis capacity in the third quarter. This should result in a further significant increase in adjusted EBIT compared to the second quarter. After downsizing during the pandemic, Lufthansa expects to hire some 10,000 new employees over the next 18 months, half of them in the second half of 2022.

The Group clarifies its outlook and now expects adj. operating profit to exceed €500 million for the full year. It also expects a clearly positive adjusted free cash flow. In the meantime, Lufthansa put pressure on the Italian government for the ITA Airways dossier. The CEO of the German carrier, Carsten Spohr, during the conference call with analysts confirmed that ITA Airways needs a strategic partner and “we think we are the right one” he concluded. We have already covered the topic, and we are positive about that. Our internal team continues to prefer other names within the sector, Ryanair and Deutsche Post, in particular.

Deutsche Lufthansa Guidance (Deutsche Lufthansa Half-year Results)

Be the first to comment