Kittisak Kaewchalun /iStock via Getty Images

Introduction

I have been keeping an eye on Crown Holdings (NYSE:CCK) for the past year as I’m a firm believer in exposure to the aluminum beverage can market. There currently is a massive supply shortage and the Big Three in the aluminum beverage can market are rapidly building new plants to try to meet up with the demand increase. In this article I’ll focus on Crown Holdings’ financial situation and performance and I’d recommend you to read my article on Ardagh Metal Packaging (AMBP), one of Crown’s competitors, for a more in-depth review of the aluminum can market and the current supply shortage.

2021 was a transition year for Crown Holdings as the company is now focusing on the aluminum cans

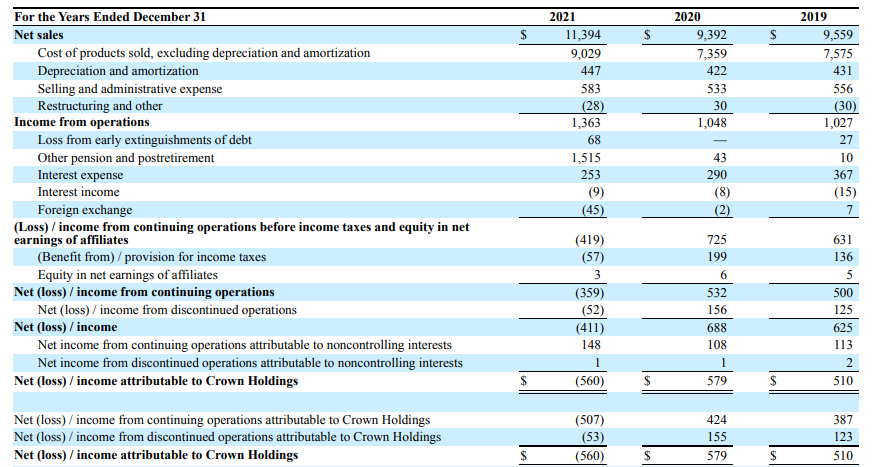

The total revenue generated by Crown Holdings in 2021 increased to $11.4B which resulted in an operating income of $1.36B, an increase of approximately 30% compared to the result in 2020. This doesn’t mean the company was profitable: Crown Holdings elected to record a pension and retirement charge of in excess of $1.5B which caused the pre-tax to fall to minus $419M.

Crown Holdings Investor Relations

The reported net loss from continuing operations attributable to the shareholders of Crown was $507M while the total net loss including the loss from discontinued operations was $560M or $4.30 per share. The net loss was obviously caused by the pension-related expenses, which were incurred after the company transferred its pension plan obligations to an insurer.

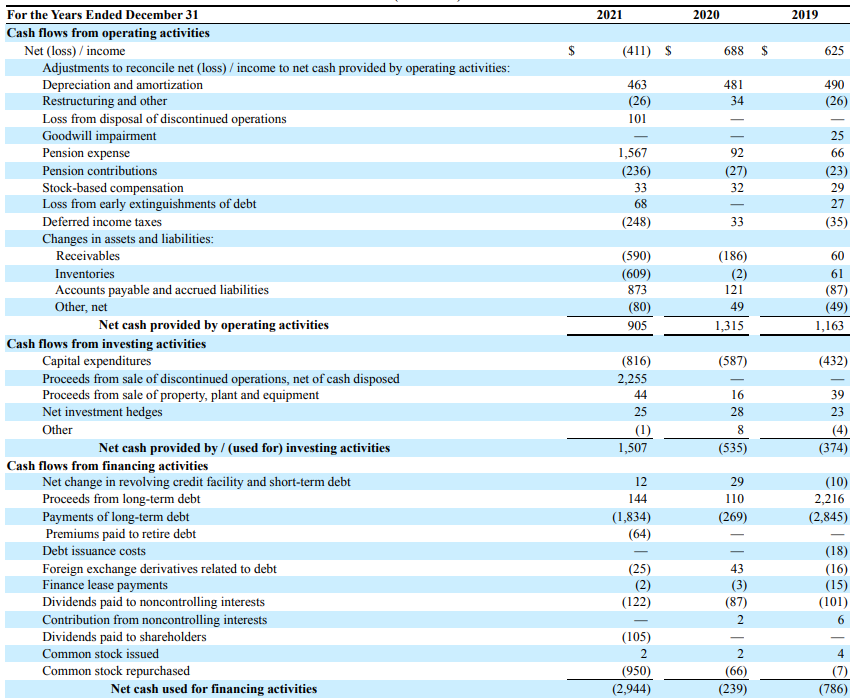

As you can see in the cash flow statement below, the vast majority of the pension-related expense was a non-cash charge and Crown Holdings only paid $236M in cash. Additionally, the reported operating cash flow of $905M includes a net investment of $326M in the working capital position and on an adjusted basis, the operating cash flow was approximately $1.33B despite the higher-than-average cash pension contributions and the $248M in cash outflow related to deferred income taxes. On a more normalized basis, the underling operating cash flow would be approximately $1.5B, including lease payments and the payments to non-controlling interests.

Crown Holdings Investor Relations

The total capex was relatively high as the company has spent $816M. That’s caused by the fact CCK is aggressively investing in expanding its production capacity as the capex was for instance 76% higher than the depreciation expenses during the year. This means that while the free cash flow based on the underlying operating cash flow was approximately $700M, the underlying sustaining free cash flow (excluding growth-related investments) exceeded $1-1.1B. Its peers, Ardagh Metal Packaging and Ball (BLL) report a sustaining capex of approximately 2.5% of the total revenue. In Crown’s case, this would indicate the sustaining capex is anywhere in between $200M and $300M and using the higher end of that range, the sustaining free cash flow could easily be estimated at $1.2B. With approximately 124M shares outstanding, this would represent a sustaining free cash flow result of in excess of $9.5/share.

What can we expect in 2022?

As Crown Holdings continues to invest in expanding its production profile, there will be a major discrepancy between the reported free cash flow (which includes growth investments) and the underlying sustaining free cash flow (which only takes the sustaining capex into consideration and ignores the growth capex).

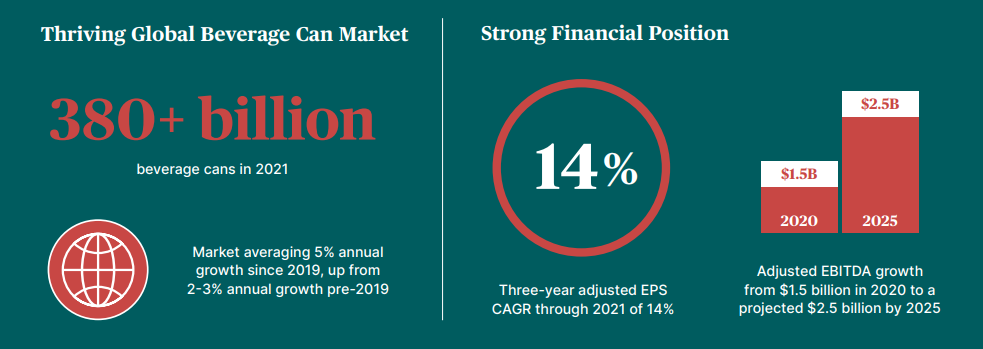

For 2022, Crown Holdings anticipates to report an adjusted EPS of $8-8.20 and a free cash flow result of $400M after spending $1B on capital expenditures. This again confirms my expectation the underlying sustaining free cash flow will continue to be in excess of $1B per year, and Crown Holdings is self-funding its expansion plans with for instance a new plant in the UK with an annual capacity of 3 billion units per year. This is just one example of how Crown expects to boost its annual EBITDA to $2.5B by 2025.

Crown Holdings Investor Relations

Investment thesis

The three main players in the aluminum beverage can industry are all ramping up their production capacity in an attempt to meet the demand. As explained in a previous article on one of Crown’s competitors, the supply and demand of aluminum beverage cans is not expected to reach an equilibrium before 2024-2025.

Crown Holdings is also aggressively investing in expanding its production capacity but the company will also have plenty of cash available to continue its aggressive share buyback program. That’s a good move as the lower share count will likely push the sustaining free cash flow per share to in excess of $10 in the very near future.

I currently have no position in CCK but as I strongly believe in the investment thesis for the aluminum beverage can market, I am overweight in AMBP, one of Crown’s competitors, simply because AMBP is the cheapest of the three main players in the industry.

Be the first to comment