tttuna/E+ via Getty Images

Following up from my recent article on fragrance and cosmetic firm Coty (NYSE:COTY), the company reported solid earnings this week. More importantly, the company generated significant free cash flow (FCF) to help in its deleveraging efforts. Meanwhile, it continues to regain lost market share in its cosmetics business, while fragrance sales remain strong and have begun to accelerate in January after the quarter ended.

For fiscal Q2, COTY’s like-for-like sales (LFL), excluding its exit from Russia and FX, rose 4% to $1.52 billion. Its exit from Russia was a -3% headwind, while FX was a -7% drag. Total sales were down -2%.

All regions saw LFL sales increases, with the Americas up 8% to $624.3 million, EMEA was up 2% to $713.5 million, and Asia sales edged 2% higher to $185.8 million.

Despite cost headwinds, gross margins expanded 110bps to 65.5%, helped by price increases. Adjusted gross margins also rose 90bps to 65.5%.

Adjusted EBITDA came in at $317.6 million, up 2%.

Meanwhile, it generated $455.1 million in free cash flow, ending the quarter with leverage of 4.1x. It also said the value of its stake in Wella rose $75 to $1.04 billion due to higher industry multiples.

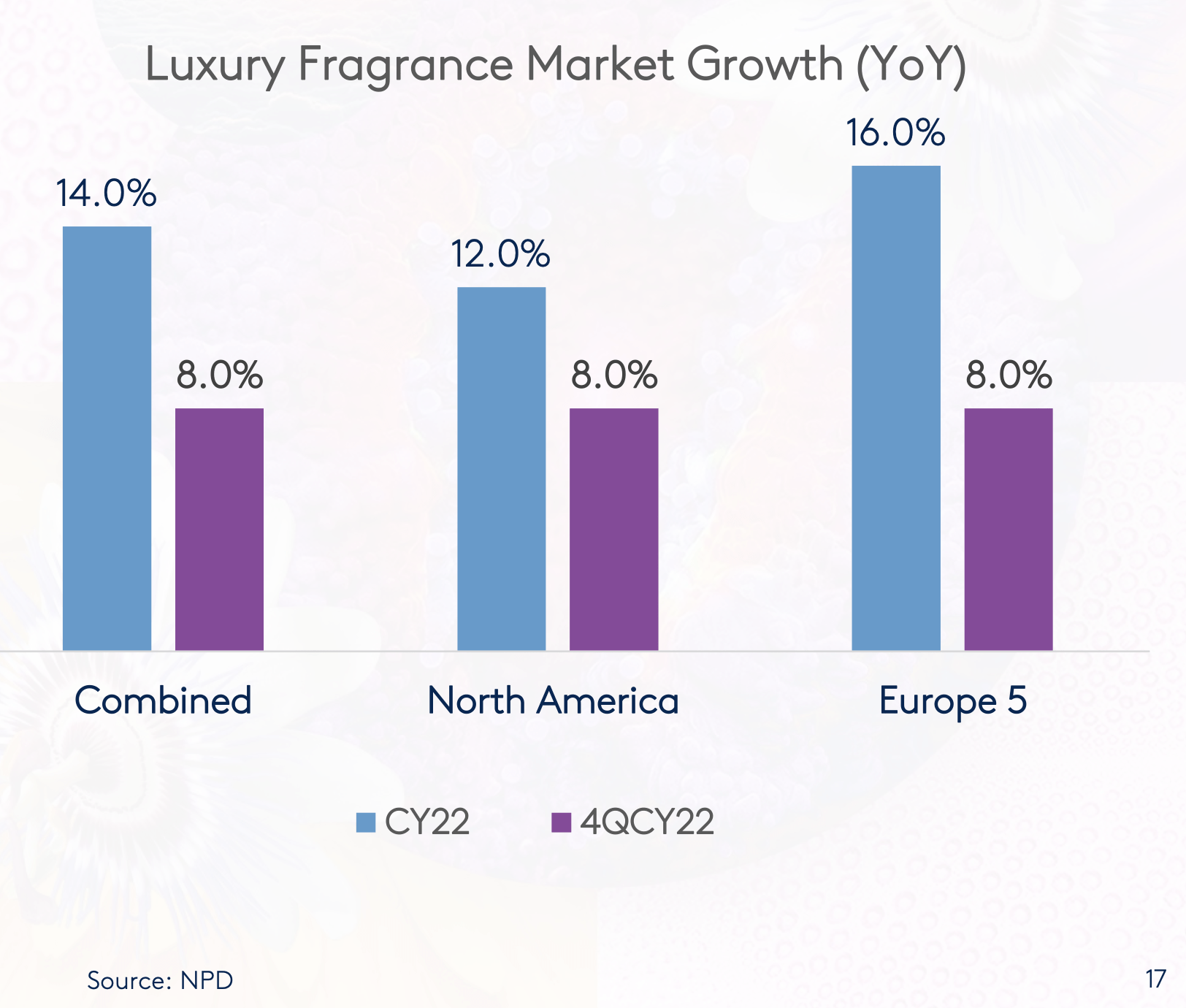

LFL Prestige sales increased 3%. COTY said the segment was hurt by industrywide shortages, specifically calling out glass bottles. The company said global travel retail was strong jumping about 40%, while Gucci and Kylie cosmetics grew over 40%. Overall, the luxury fragrance market remains strong.

Prestige adjusted EBITDA rose 4% to $228.5 million.

Company Presentation

Discussing the momentum in fragrance sales on its earnings call, CEO Sue Nabi said:

When it comes to the fragrance market/the fragrance index, indeed, the fragrance market is 25 — 20% to 30% higher than the levels of 2019. And in markets like the U.S., again, and you may know this, the Prestige fragrance market is over 60% higher than compared to pre-COVID levels. Again, it’s hard to see how this would just be driven to some onetime factors, I have to say.

And sometimes I hear this. And I do believe it’s not the right explanation. Historically, this has been big distinct category. But what we are now seeing in consumers using fragrance as part of their daily routine. And this business has become really a health business, mental health business, I would say. Fragrances being seen as mood boosters, allowing people to feel better in their daily — day-to-day life.

In particular, during the last couple of years, we have seen increased usage by new categories where the penetration has increased structurally. I’m thinking about Gen Z. I’m thinking about men and I’m thinking about “Hispanic consumers, if you of course focus on the American market. We are also seeing, at the same time, the rise of fragrance influencers and social media, specifically TikTok, but also on YouTube, which is also helping to drive sustainable growth for this category.”

Nabi further noted that fragrance penetration in the U.S. still trails Europe by a wide margin. U.S. penetration is in the high 20% level, while Europe is closer to 50%. China is only 3%.

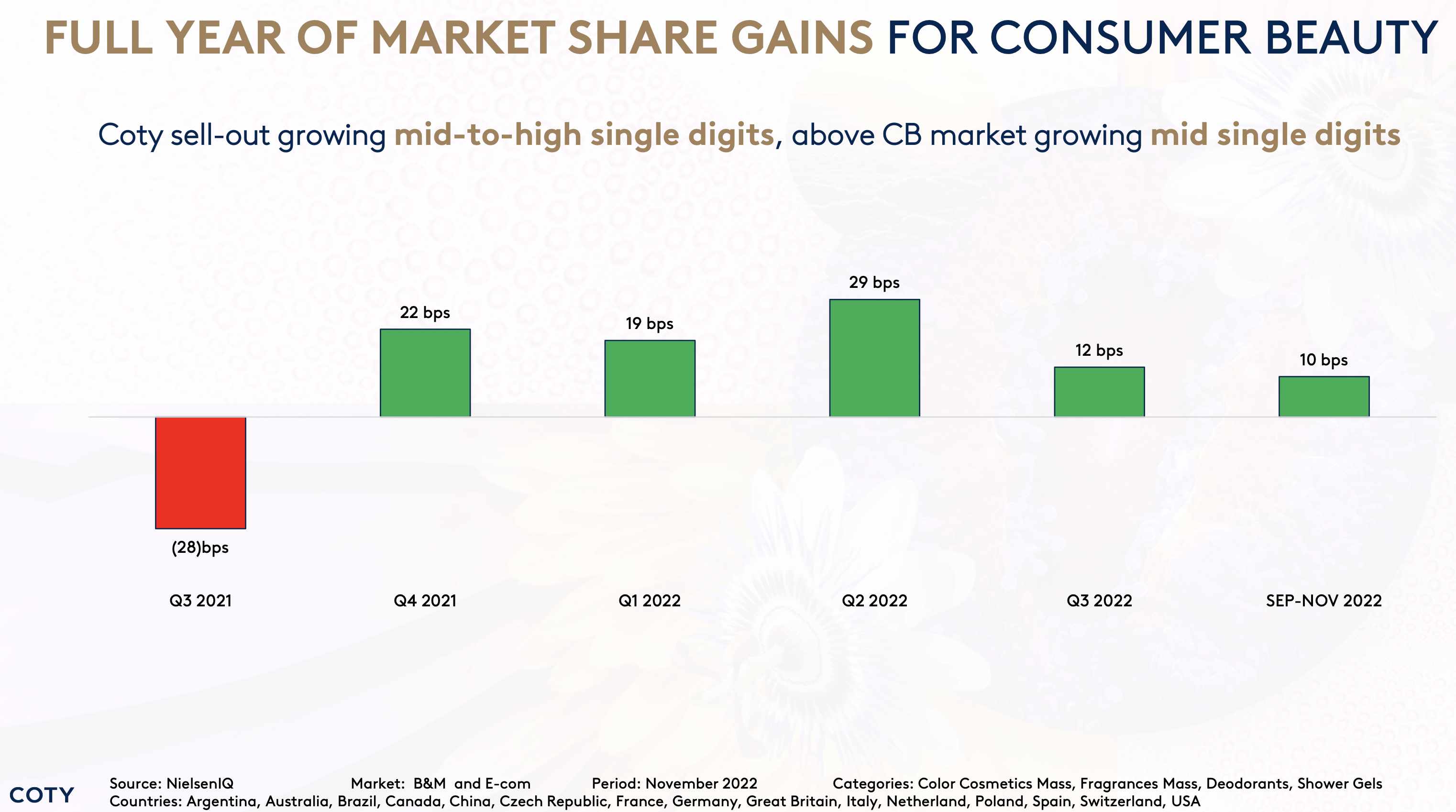

Consumer Beauty sales climbed 6% on a LFL basis, and was down -1% overall. The company said it continues to gain market share in the segment, and that a number of brands grew including CoverGirl, Rimmel, and Max Factor.

Company presentation

Discussing the resurgence in beauty sales, Nabi said:

So again, when it comes to Consumer Beauty, you’re right to point out on the fact that Consumer Beauty is entering the new cycle, in fact. The first cycle that started somewhere around Jan ’21 was really to reinvent the brand equity, sometimes coming back to historical brand equities, strengthening these, modernizing these, creating great advertising with the highest ROI as just mentioned by Laurent.

And this was really what explains the back to market share gains, which happened now for the full year. This is the first time since 2016 that this division is gaining market share for a full year. So this was Stage 1. Stage 2, in a way, I love to say that Stage 1 was fixing the surface, if I may say, and then Stage 2 is really getting deeper, and we’ll start to see real, I would say, disruptive, best-in-class in terms of efficacy in the market innovation.”

Nabi noted that it takes about 1.5 years to create a new, great cosmetic product. However, she said that new innovative products have the best ROIs in the company.

Looking ahead, COTY reiterated its full-year guidance calling for adjusted EBITDA of $955-965M based on current FX rates. It continues to expect LFL sales growth of 6-8%, with modest margin expansion. It continues to target exiting calendar year 2023 with 3x leverage and 2x for CY25.

Management said they are seeing strong demand in most markets and that component shortages are starting to ease. It sees particular strength in Prestige Fragrances. As such, they have seen an acceleration in January growth.

Nabi was also bullish on China pointing to the country reopening in January and noting that COTY had the most white space in China of any major beauty company. She also noted that there was a premiumization trend that was accelerating among Chinese consumers as well as a healthification trend that was benefiting skincare. In addition, the exec said she saw a shift from heritage brands to new premium brands and more willingness among Chinese consumers to try new, innovative brands.

Conclusion

This was exactly the type of report and guidance I wanted to see from COTY. The company is growing sales nicely on a LFL basis, margins are expanding, and most importantly it’s reducing leverage. Leverage is now down to about 4x, and well on track to be 3x by the end of 2023.

The company has generated FCF of $543.3 million its first two fiscal quarters. FQ3 is usually a small outflow, while FQ4 should be a nice inflow, resulting in about $600M in FCF for the year. That sets COTY up to meet its deleveraging goals, which should allow for the stock to re-rate higher closer to peer valuations. Rinse and repeat next year, as well as sell its remaining stake in Wella, and the company will have met its 2x leverage goal by the end of CY25.

Meanwhile, Nabi continues to prove that she is turning the company around through increased market share gains in cosmetics and strong fragrance sales. China and skincare, two areas where the company is under penetrated, both remain attractive opportunities. I continue to think Coty stock could trade up $16 or higher.

Be the first to comment