tiero

The current market environment is a dream for value investors, as there are many cheap stocks to choose from. For long-term investors, however, it’s important to pick stocks that will not only survive the current market meltdown, but also thrive in the decades thereafter. For those looking for generational quality buys, they don’t need to look much further than Corning (NYSE:GLW). In this article, I highlight what makes now a great time to pick up shares of this durable name, so let’s get started.

Why GLW?

Corning is a global leading innovator of materials science. It’s been around for over 170 years and specializes in the production of glass, ceramics, and optical fiber, the latter of which makes GLW a crucial partner to telecom players. Corning has a leading market share in many end markets, with products that include flat-panel monitor displays, Gorilla Glass, gasoline particulate filters in cars, and very importantly, optical fiber for broadband communications.

What makes Corning stand out is the robust demand for its optical fiber products that serve as the plumbing for telecoms and the emerging 5G category. Furthermore, Corning is also becoming an important player to the semiconductor industry through its 80% ownership stake in Hemlock Semiconductor, which manufactures ultrapure polysilicon for the semiconductor and solar industries.

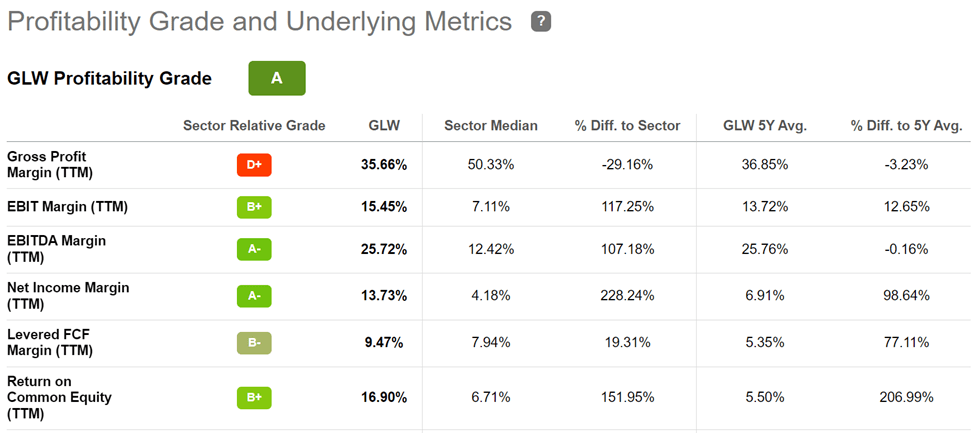

Corning benefits from its size and scale, as its business is both research and manufacturing intensive. This creates an economic moat around the business, making it very difficult for new entrants into the business, and results in high profitability. As shown below, GLW scores an A grade for profitability, with sector leading EBITDA and Net Income margins of 26% and 14% respectively. Moreover, it generates an attractive 17% return on equity, due in part to hefty share repurchases, which amounted to a 44% reduction in share count over the past 10 years.

GLW Profitability (Seeking Alpha)

Meanwhile, GLW has been performing well despite macroeconomic headwinds showing up during the second quarter, with revenue growing by 7.4% YoY to $3.8 billion. This was driven primarily by Optical Communications as well as solar sales in Hemlock and emerging businesses. Not all is rosy, however, as display technologies showed cracks with an 8% sales decline amidst a decline in consumer spending.

Looking forward, I see some of the macroeconomic headwinds being manifested in GLW’s third-quarter results. However, I see the long-term growth thesis as being intact. This is supported by tailwinds in the optical fiber segment that is part of a larger megatrend towards increasing needs for faster and more reliable telecommunications. This was highlighted by management during the Goldman Sachs (GS) Communacopia Technology Conference a couple weeks ago:

Our relentless commitment to R&D allows us to reinforce and extend our leadership and distinctiveness in vital capabilities. This puts us squarely at the center of secular trends that touch many facets of daily life, and also creates the foundation for customer collaborations that advance their industries.

For example, in optical communications, broadband is increasingly viewed as a basic human right. We are partnering with leaders in the industry to create a world with nearly infinite and ubiquitous bandwidth and I’m going to use this to illustrate our overall strategic approach and how it drives growth.

We extend our leadership and support our customers by delivering solutions that help them realize their network visions better, cheaper and faster and Corning’s track record sets the standard for doing just that. We’re seeing robust growth and customer demand as we create significant innovation programs in broadband, 5G and the cloud.

To support this growing demand, we’re increasing capacity for both cable and fiber. At the end of August, we announced that we’re expanding our manufacturing capacity for optical cable by building a new plant in Arizona. It’s supported by our long-term relationship with AT&T.

Meanwhile, GWL maintains a strong BBB+ rated balance sheet and pays a respectable 3.6% dividend yield that’s well covered by a 46% payout ratio. Even more impressive is the fact that GLW has a 5-year dividend CAGR of 12% and 11 years of consecutive dividend growth.

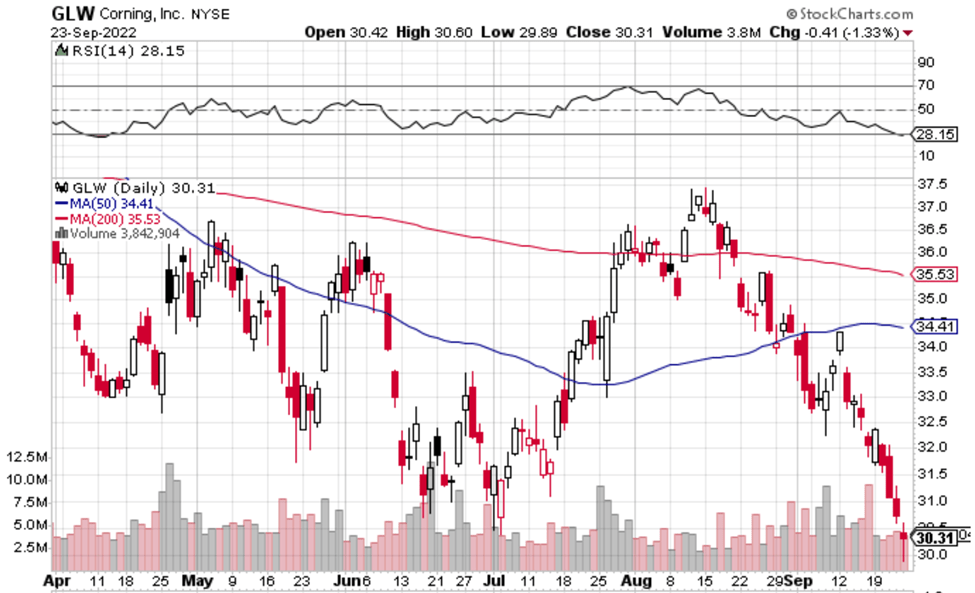

It appears that the market is overly-rotated on near-term challenges and doesn’t appreciate the overall quality of the enterprise and its long-term growth drivers. As shown below, GLW is now trading well below its 50- and 200-day moving averages of $34.41 and $35.53, and carries an RSI score of 28, indicating that it’s in oversold territory.

GLW Stock Technicals (StockCharts)

Moreover, at the current price of $30.31, GLW trades at a PE of 13.7, sitting well below its normal PE of 17.9 over the past 5 years. This is also considering the 12% annual EPS growth rate that analysts estimate over the next 2 years. Morningstar has a $42 fair value estimate, and sell side analysts have an average price target of $39.64. Using the more conservative of the two estimates, GLW could produce a potential one-year 34% total return including dividends.

GLW Valuation (FAST Graphs)

Investor Takeaway

In summary, I believe that Corning is a very attractive investment at the current price. The company has a strong track record of innovation, pays a respectable and high-growing dividend, and is well-positioned to benefit from tailwinds in the optical fiber segment. While there are some near-term challenges, I believe that the market is overly-fixated on these and is underestimating the long-term growth potential of the company. For these reasons, I view Corning as being a strong buy at present.

Be the first to comment