Hiroshi Watanabe/DigitalVision via Getty Images

Description

Over the course of several years, CONMED Corp. (NYSE:CNMD) has gone from experiencing weak/neg growth to consistently growing HSD thanks to a few particularly fruitful deals, the introduction of innovative new products, and a more robust and competitive product lineup. While the business has faced difficulties due to macro headwinds and disruptions in the supply and demand for capital equipment, I am confident that CNMD’s continued focus on innovation and high-growth products will position the company for sustainable growth in the future.

4Q22 Review

4th quarter sales were significantly impacted by the warehouse software implementation, which was the main reason for this weak quarter. The sluggish sales were accompanied by a minor downward revision to preliminary 2023 guidance given in November.

From an objective standpoint, CNMD would have performed above expectations. Without the disruption headwind, it’s likely that sales and earnings would have surpassed where consensus estimates were. Even CNMD’s longer-term profitability guidance exceeded my (and, I suspect, most investors’) expectations, with a projected 60% gross margin before FY25, compared to the prior consensus estimate of 57.7%. However, I did not appreciate hearing that the company would be cutting its FY23 projections. Investors are more likely to place weight on this downward revision than on the improved long-term margin guidance. I believe investors will likely be watching 1Q23 results closely for clues about CNMD’s ability to regain market share (given the disruptions), and I believe this will have a significant impact on the stock price.

More on disruptions

Obviously, the disruption had a major effect on business performance (hence the weak sales). As inventory becomes available to fulfill these backorders, the good news is that CNMD should be able to recoup around $30 million of the disruption. On the other hand, I believe the remaining $35 million represents lost revenue because customers were forced to seek out services from competitors. Additionally, although the overall operating situation has improved and the backlog recovery is expected to boost sales in 1Q23, the extended remediation timeline and the possibility of harm to customer relationships are sources of disappointment. That said, without the setbacks, both AirSeal and Buffalo Filter could have grown by over 20%, which is encouraging. Management having faith to continue growing these two business units by more than 20% in FY23 is a good sign.

Other outlooks

The $12.5 million in M&A contribution saw no impact from the warehouse problem, being driven primarily by In2Bones and their well-integrated sales force and exciting product offering. Successful efforts are also being made to train and educate employees at Biorez, and CNMD is concentrating on moving the two-year follow-up clinical data forward to position the company for growth and margin expansion in FY24 or later.

Guidance

Management revised its FY23 forecast by lowering its top-end revenue and EPS guidance. Management also mentioned that while FX and macro pressures were felt in 1H23, they would be neutral to positive in 2H, and that Q4 would have easier comps. As for other business units, the guided $22–$26 million contribution from M&A at In2Bones and Biorez in 1H suggests to me that these divisions continue to enjoy healthy underlying momentum. Margin wise, management guided GM to be between 55.5% and 55.8% in FY23, with further increments in FY24/25 as the company reaps the full benefits of its high-growth, high-margin products. Furthermore, the sequential improvements in warehouse management reflected in the guided 1Q23 revenue of $262 to $272 MM provide confidence that the situation is improving.

Valuation

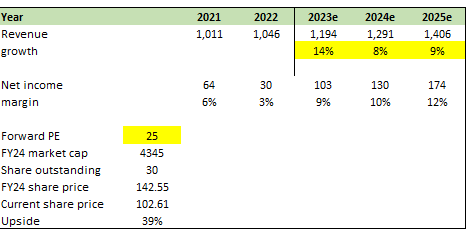

My revenue and earnings assumption mostly mimics consensus figures and management guidance. My variant view here is on valuation. As for CNMD’s forward PE of 30, I think that’s too high given the company’s lackluster near-term outlook. I anticipate CNMD multiples to trade down to the mid-20s (the middle of its historical range) in the near future in light of the updated EPS guide down and potential FX headwinds.

Own estimates

Summary

While Q4 results were below expectations, CNMD has resolved the warehouse software problem and should benefit in 2H23 from an easy comp and easing macro environment. In addition, without the setbacks, both AirSeal and Buffalo Filter would have expanded by over 20% in 4Q22 and are expected to expand by over 20% in 2023. Furthermore, both In2Bones and Biorez had successful 4Q22 as well. Thus, even though I anticipate multiples to contract over the medium term, I believe the upside is still attractive.

Be the first to comment