Emir Memedovski/E+ via Getty Images

The PIMCO Corporate & Income Opportunity Fund (NYSE:PTY) utilizes a dynamic asset allocation strategy across several fixed income segments including high-yield corporates, investment grade credit, real estate mortgages, as well as foreign bonds. Its leveraged profile and active management as a closed-end fund have helped it stand out with benchmark-beating performance over the past 2 decades. Income investors will likely also be attracted to the fund’s 12% yield through a monthly distribution.

That being said, the market conditions this year have resulted in significant volatility considering rising interest rates and wider credit spreads amid a weaker economic environment. PTY is down more than 25% in the past year at its market price on a total return basis while the NAV has pulled back 10% over the same period. Still, we highlight a couple of reasons to see value at the current level with the fund well-positioned to rebound as macro outlook improves going forward. Several indicators between narrowing credit spreads, and room for the U.S. Dollar to pull back suggest PTY can rally from here.

What is the PTY Fund?

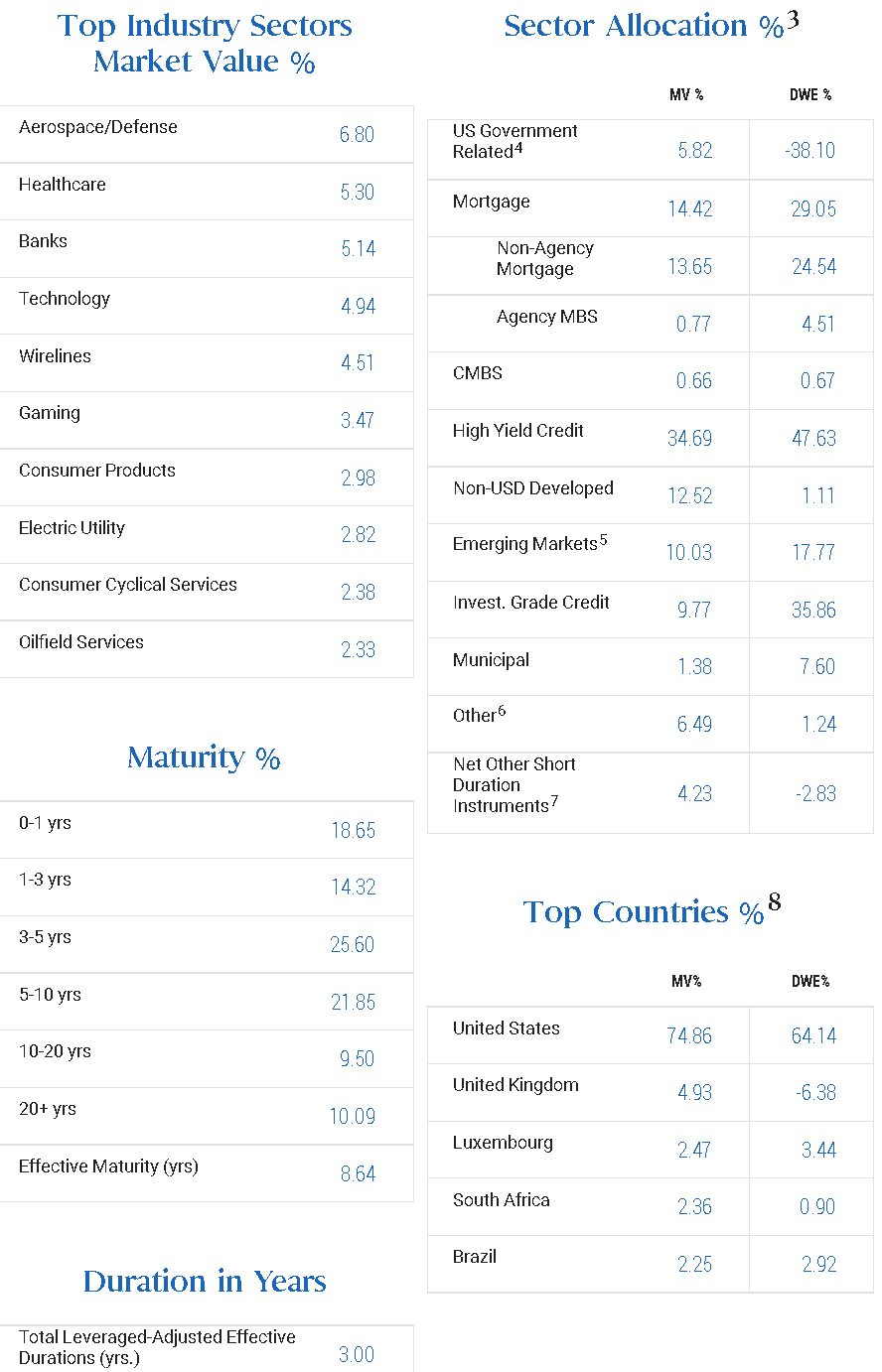

According to the fund manager, the investment philosophy employed by PTY focuses on duration management, credit quality analysis, risk management techniques, and broad diversification. The effort here is to maximize a total return through a combination of current income and capital appreciation. The idea of duration management is to allocate positions to minimize interest rate sensitivity across different fixed income segments.

High yield credit represents the largest position of the fund at 35% of the market value or 48% by duration weighted exposure (DWE). The difference between these two metrics considers the average maturity of holdings by sector and their corresponding allocation. The total leverage adjusted effective duration at 3.0 years implies an intermediate maturity structure.

Investment grade credit at 36% by DWE reflects longer maturity holdings in higher quality names in an effort to balance risk. Emerging markets debt, municipal bonds, and non-agency mortgages are all well represented. At this point, nearly a quarter of the fund’s market value is in foreign securities, including developed markets like issues in the United Kingdom.

PIMCO

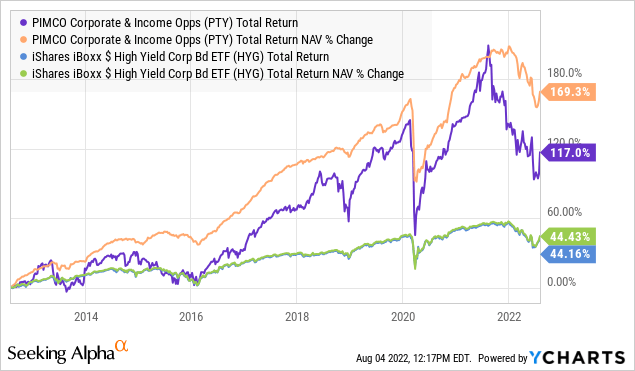

The takeaway here is that the strategy has worked with PTY returning 117% on a total return basis to its market price over the past decade or 169% at NAV which compares to a more modest 44% in the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) which we use as a benchmark.

From the chart below, notice that the strong gains between 2016 and through 2021 were during a period of interest rates trending lower and overall strong economic activity. Fast-forward and the decline over the past year with significant volatility reflects the shift in the market environment. The combination of higher interest rates with the Fed tightening along with more difficult operating environment for the underlying corporate credit exposure explains much of the selloff. The fund’s effective leverage of 49% has added to the volatility but would help the fund outperform to the upside on an eventual rebound.

Note that PIMCO also offers several other CEFs within the multi-sector fixed income/allocation strategy category like the Dynamic Income Fund (PDI) or Dynamic Income Opportunities Fund (PDO). While all of these technically follow different mandates through unique portfolios, we would expect the performance to be relatively correlated to similar market themes in fixed income.

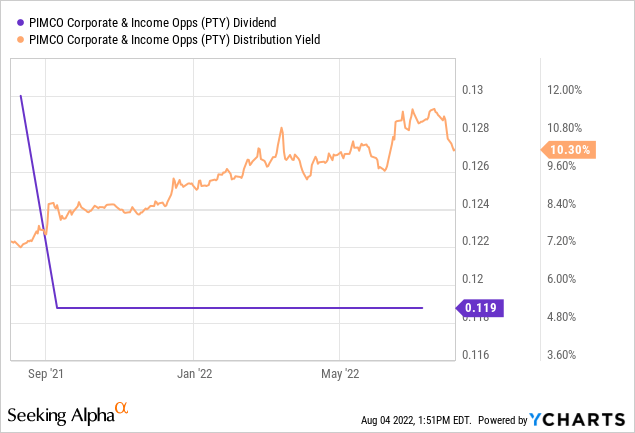

PTY is recognized as one of Pimco’s “flagship” funds given its 12.5% average annual total return since inception, which is the highest among 21 funds by the asset manager. That being said, some of that shine may have rubbed off over the past year considering the monthly distribution rate was cut to $0.1188 per share from the prior rate of $0.13, although the indication is that the current payout is sustainable in the foreseeable future.

Note that while PTY distributed a small return of capital (ROC) in 2021 representing around 20% of the payout, historically the fund’s monthly distribution has been met by underlying portfolio income achieved through the leveraged strategy.

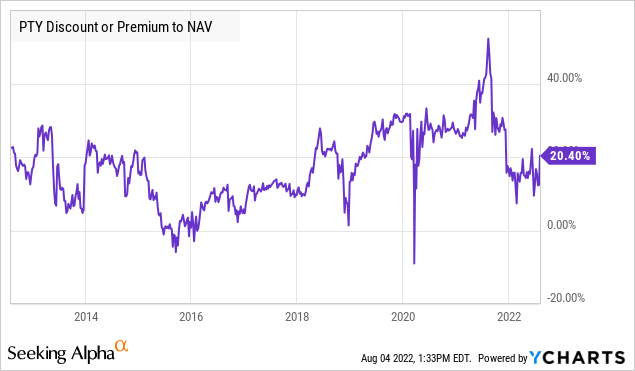

We note that PTY trades at a premium to its net asset value of 20%. This is a case where investors bid up shares owing to their long-term track record and reputation of market-beating returns. Keep in mind that the PTY has historically traded at a widespread considering an average premium to NAV of 23% over the past 5 years. By this measure, the fund doesn’t necessarily stand out as super cheap, but otherwise in line with its historical norm. In an environment where credit gains momentum, there would likely be room for the premium to climb even higher.

Bullish on High-Yield Credit

We’re bullish on PTY and see the fund as an attractive option to gain exposure to high-yield credit through a compelling income-focused strategy. The first point here is that there are indications market conditions are improving compared to an environment of deep pessimism in Q1 and Q2. The most positive development has been a sharp pullback in energy prices, including the national average of gasoline falling for 7 straight weeks, and trending below $3.99.

This is important since high inflation has been one of the main headwinds to economic conditions this year. Evidence that the CPI is set to cool off opens the door for improving consumer sentiment and business expectations. One line of thinking is that the Fed would have room down the line to slow its pace of aggressive rate hikes.

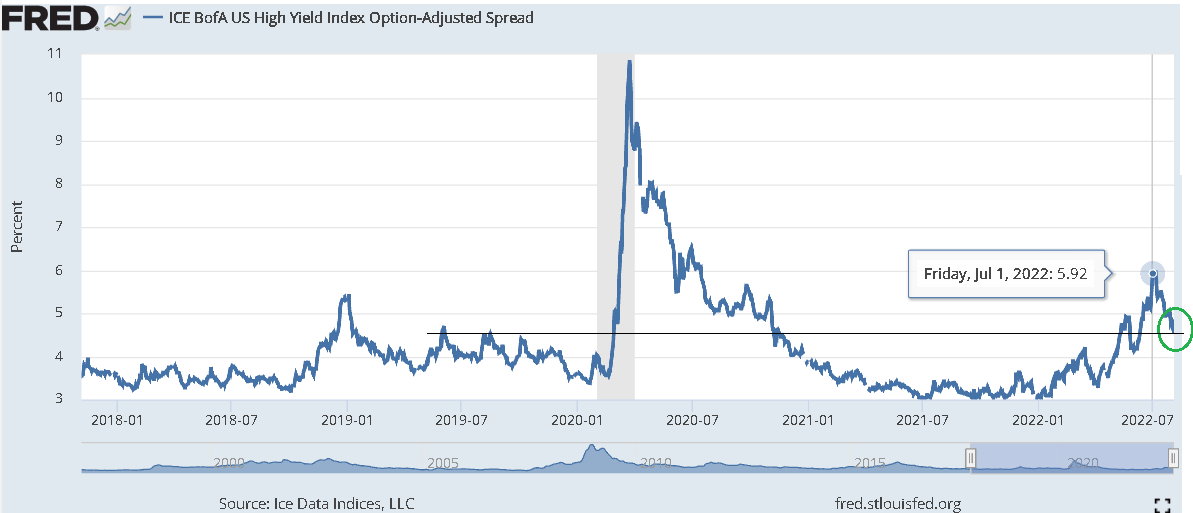

The impact is evident as credit spreads have narrowed sharply from their peak in late June, based on the “ICE BofA US High Yield Index Option-Adjusted Spread”. The implication of narrowing spreads, which refers to the premium demanded by the market to hold risky bonds over Treasuries, is that the general risk of default is falling.

St. Louis Fed

We can also point to the NY Fed Index, which shows global supply chain stress levels have eased to a one-and-a-half-year low. If there were fears of a depression-style economic collapse in early June, the latest data helps to brush aside those concerns, at least in our view.

To be clear, credit spreads and financial market conditions remain well off levels from 2021, but the theme here is a greater sense of stability, which is positive for credit markets and the PTY portfolio.

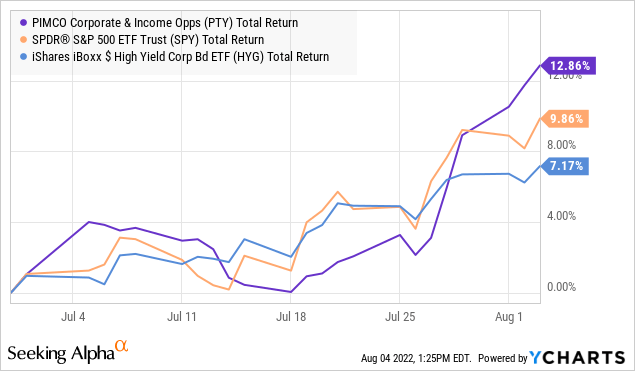

As it relates to inflation, we’ll get confirmation next week with the official July CPI, but it appears the market is already running with the narrative. Bonds have rallied, potentially pairing back long-term inflation expectations, while equities have also staged an impressive comeback in recent weeks. PTY is up nearly 12% this month, and we see the potential for more upside.

Final Thoughts

PTY is an interesting fund with the attraction here being an otherwise aggressive positioning to improve credit market conditions based on its leverage. While there are other funds that may offer a higher yield or trade at a deeper discount, the opportunity here is to buy a high-quality fund that has earned its reputation as an excellent income instrument with positive long-term returns.

With an expectation for interest rates to continue climbing and long-term bond yields to remain volatile, the bullish case for PTY is the so-called “soft-landing” scenario where economic conditions at least outperform a low bar of expectations despite the higher rates. We would expect credit spreads to narrow further as a tailwind for the PTY strategy.

As it relates to risks, it’s clear that deterioration to the economic environment from the current baseline would open the door for another blowout in credit spreads. A resurgence of sharply higher inflationary pressures would also undermine the bullish case for high yield.

Be the first to comment