Funtay

British American Tobacco p.l.c. (NYSE:BTI) has seen share price weakness lately, which I believe is another good opportunity to consider the company’s strong forward dividend yield which currently stands at 7.4%. British American Tobacco’s shares present investors with an opportunity to pick up a safe dividend and participate in the upside delivered by its alternative products categories consisting of the three brands Vuse, glo and Velo. British American Tobacco’s shares are attractively valued based off of earnings, and the company could announce a new stock buyback in FY 2023. Therefore, I believe the risk profile for British American Tobacco is very much skewed to the upside!

An opportunity to buy a strong 7.4% yield

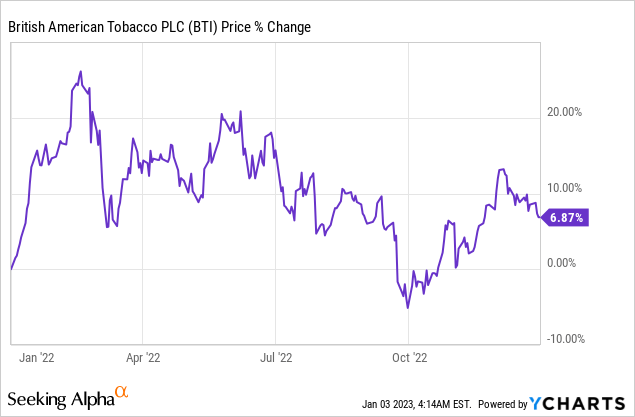

Last year ended without a Santa rally, and recent market weakness has translated to weakness in shares of BTI as well. British American Tobacco has seen a strong price recovery since reaching a low in October, but shares have recently started to dip again. I believe BTI is worth considering on the drop considering that the company is growing its new product categories rapidly. That helps counter the decline in the traditional combustible product category.

British American Tobacco’s guidance for FY 2022

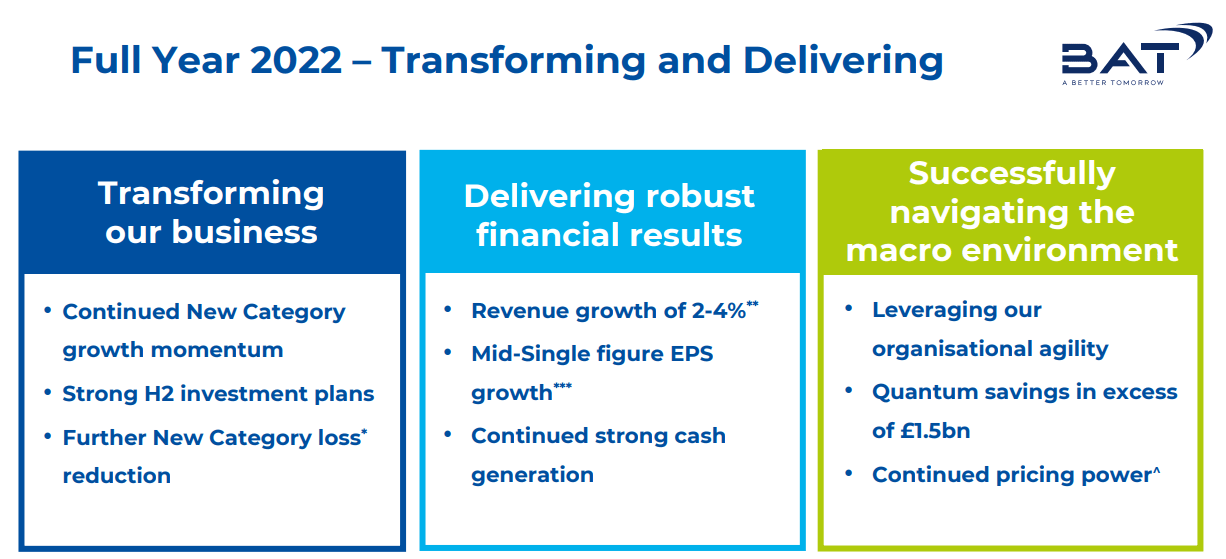

BTI has guided for 2-4% top line growth in FY 2022 and mid-single digit growth in adjusted diluted EPS. While the top line is expected to remain challenged due to a decline in the share of smokers as well as forex headwinds, BTI has laid out an ambitious long-term plan to grow its alternative product categories to £5B in revenues by FY 2025 and drive the segments to consistent profitability by this time. The revenue growth target implies a 25% compound annual growth rate between FY 2021 and FY 2025. In FY 2021, British American Tobacco’s new product categories generated £2.1B in revenues.

Source: British American Tobacco

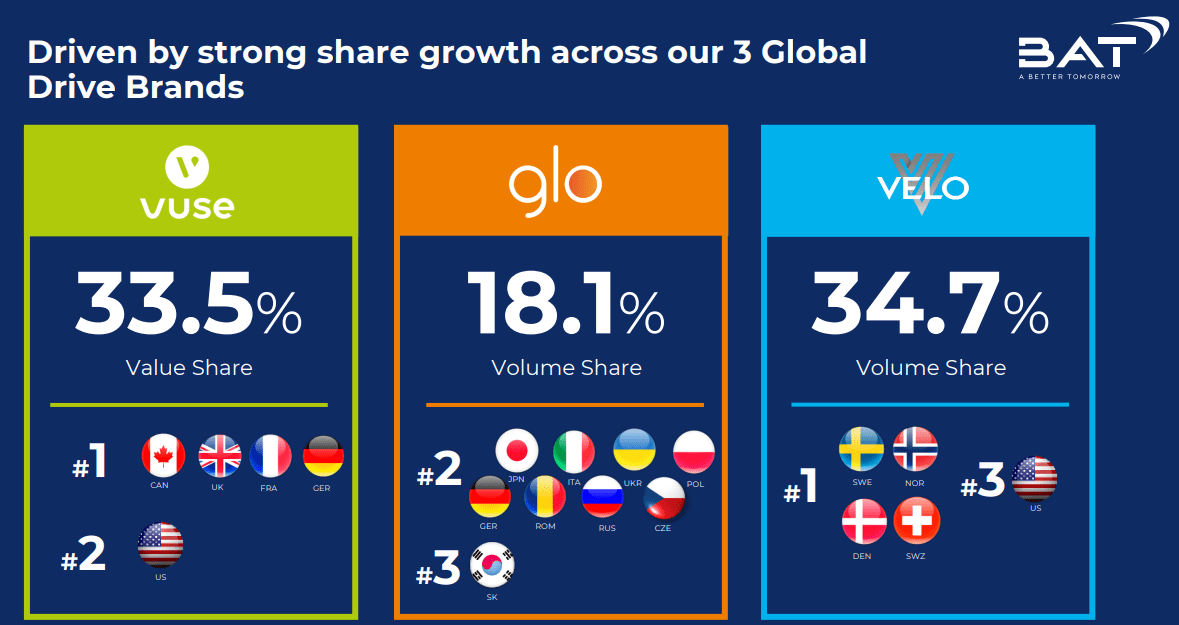

Alternative product categories consist of three distinct value propositions for consumers, mostly of the younger generation: (1) Vuse, which is BTI’s vaping brand; (2) glo, which is sells and markets heated tobacco products; and (3) Velo, which is British American Tobacco’s oral nicotine products.

In the first six months of FY 2022, alternative products within British American Tobacco’s portfolio have seen 45% year-over-year revenue growth (on constant rates), and all three brands saw major volume and market share gains in key markets. This momentum can reasonably be expected to continue in FY 2023, and BTI not only said in a release in December that it confirmed its outlook for FY 2022, but also that Vuse is now the number 1 vape brand in the U.S. with a total value share of 39.3%.

Source: British American Tobacco

Investors could see a new stock buyback

British American Tobacco announced a £2B stock buyback in FY 2022, and the company could add to this program in FY 2023. Obviously, a falling stock price makes a strong case for an additional stock buyback program, and since the tobacco firm in the past has returned cash both as dividends and as stock buybacks, I believe management could announce a new £2-3B buyback in FY 2023 – perhaps when it presents earnings for the last quarter in February.

British American Tobacco’s valuation

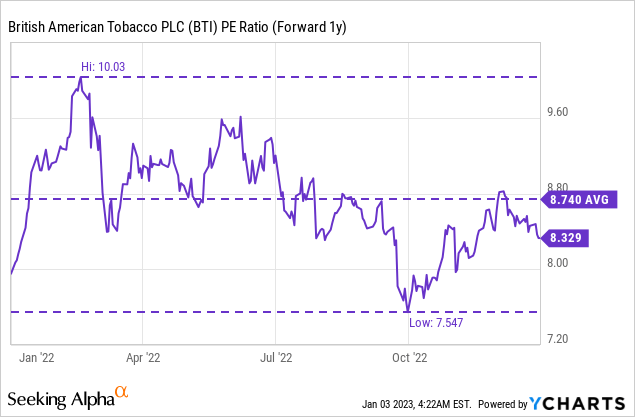

British American Tobacco’s shares are cheap, and investors are currently paying an 8.3 X forward P/E ratio for the tobacco firm’s 7.4% dividend yield. Additionally, shares are trading below the 1-year average P/E ratio, which indicates that investors, perhaps, have become too negative on the prospects of British American Tobacco’s growth potential, both in the U.S. and internationally. I believe stock buybacks are making good sense here for British American Tobacco at such an attractive valuation.

Risks with British American Tobacco

The share of smokers has been on the decline for decades, and British American Tobacco is experiencing top line headwinds as a result. Possibly even more challenging is the regulatory environment, which places advertising restrictions on tobacco firms. In particular, the U.S. government is actively (but so far unsuccessfully) trying to ban e-cigarettes. Going forward, the regulatory and business environment likely will remain challenging, and slowing top line growth could lead to a lower valuation factor for British American Tobacco’s shares.

Final thoughts

I believe British American Tobacco’s shares are attractive in two distinct ways: (1) The dividend yield has risen to 7.4% due to BTI’s recent share price weakness; and (2) The valuation is very attractive again considering that the tobacco company’s shares are trading at a P/E ratio of only 8.3 X. They are also trading below the 1-year average P/E ratio, and a new stock buyback in FY 2023 could help stabilize the stock price.

Considering that investors also have the opportunity to invest in the company’s growth in the alternative product category, which is seeing accelerating momentum, I believe the risk/reward for British American Tobacco p.l.c. is very compelling for long-term investors!

Be the first to comment