KristinaGreke/iStock via Getty Images

Investment thesis

I recommend to stay neutral on Cricut (NASDAQ:CRCT). The trend towards personalization and customization, with many consumers willing to pay more for customized products, presents a good opportunity for CRCT. However, the stock may face challenges in the short term due to increased demand during Covid, so it may be best to hold off on investing for now.

Business overview

CRCT produces cutting machines with computerized controls for home crafters. The products may be used to cut, write, and create aesthetic effects from a wide range of materials.

A better description of CRCT business can be found in their IR overview page here.

Personalization, digitization, and creativity are all coming together

Nowadays, individuals prefer to surround themselves with personalized objects. One study found that a whopping 25% of consumers would pay a premium for a customized offering. From the same study, more than 35 percent of buyers have shown an interest in having furniture, household goods, and do-it-yourself items made specifically for them. I contend that this is the single most important factor contributing to CRCT’s expansion.

Another factor driving this sector ahead is the widespread use of social media, where people all around the world are actively participating in innovative creative projects. Hundreds of millions of individuals all around the world use social networks on a regular basis. Thanks to the widespread availability of social media, people are now able to find fresh inspiration for their initiatives and ideas whenever and wherever they please. Naturally, this is good news for CRCT. Millions of people follow CRCT on social media, and thousands of individuals have uploaded projects to the site.

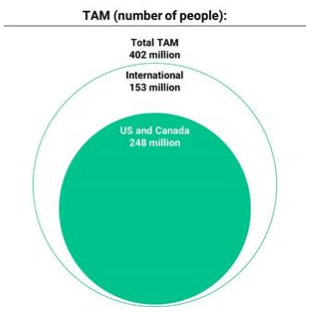

Even though the numbers are a little dated, I think the sheer enormity of this TAM is indicative of the CRCT’s growth potential. The S-1 states that management believes there are more than 153 million potential CRCT customers in major international target areas, for a grand total of over 402 million potential customers.

S-1

Vertically integrated platform that is easy to use

CRCT equipment is distinguished by its user-friendliness and the fact that it is enabled by software. I believe that CRCT’s ability to help new users get up and running quickly on the platform thanks to its user-friendly interface is a major selling point. When compared to other cutting machines, my observation is that Cricut models consistently deliver faster cutting rates over a wide range of blade depths and materials.

Also, because of its vertically integrated business strategy, CRCT is able to participate in projects all the way from the initial idea to the final product. Because of this, CRCT is able to participate in the planning stage at an earlier point than its competitors, giving it a major competitive edge. Once the user has adapted their workflow to incorporate CRCT, they are more likely to continue using it for the duration of the project, and maybe for future projects as well.

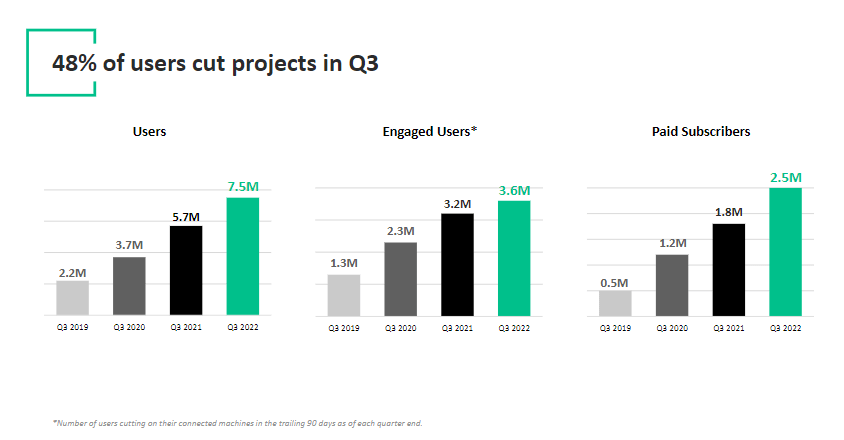

Based on CRCT’s success in attracting a large community of creatives (7.5 million users, 2.5 million of whom are paying customers), I would say that this strategy has been fruitful.

3Q22 earnings

The scalable nature of the CRCT’s technology design also makes it possible for users to access and contribute from virtually any computer at any time. Additionally, CRCT maintains a growing database and catalogue of resources. Due to the one-of-a-kind nature of any given creative activity, this database helps users determine if linked resources are appropriate for their specific environment. Pressure, speed, and machine tools for a unified experience are all recorded, updated, and regulated in the CRCT materials database.

Effective go-to-market model

As the number of Cricut users increases, I believe the effectiveness of this self-perpetuating marketing technique will also increase due to the positive word-of-mouth it generates. The more people who use the CRCT product and like it spread the word, the more people will use the platform. CRCT has invested in digital and social media marketing in addition to word-of-mouth marketing to draw in customers (as mentioned above, CRCT has a pretty strong social media presence that is well-engaged).

On top of that, I think CRCT has done a great job of grasping the importance of an omnichannel presence in the modern business world. This is especially true now, when customers typically expect to be reached via a variety of methods, not only online. In addition to selling directly to customers digitally, CRCT also works with traditional and online retailers to distribute its wares and services.

Recurring revenue

For a monthly price, CRCT offers access to their equipment, materials, and design content. Although I anticipate sales from Connected Machines segment to continue growing over the long term due to the large TAM, I do see the growing mix of these recurring revenue categories as a positive part of the business.

International expansion

The TAM is huge, thus I anticipate that CRCT will expand into new markets in order to meet rising demand abroad. In my opinion, the potential for CRCT to grow worldwide is substantial. Actually, CRCT has already begun to enter new markets lately like South Korea, Japan, and Taiwan. They’ve also localized their design apps into a number of other tongues.

Based on my research, it appears that CRCT has done an excellent job of delivering localized information and will continue to offer relevant content for countries where they are at different phases of development. I believe CRCT will persist in its quest for global expansion, with a special emphasis on nations with sizable numbers of active creatives, who will be most receptive to the Cricut value offer.

Like their local rollout, I imagine CRCT’s international expansion would use a mix of traditional and digital retail channels.

Competition

While I do think CRCT has achieved success in some areas, I also think it faces stiff competition overall, especially in its Accessories & Materials division, where I see little room for distinction.

In the market for cutting machines, Cricut faces off against rivals including Brother, Graphtec, and Silhouette America. I think that Cricut’s ability to cater to beginners more effectively than its competitors is due in large part to the company’s smart and user-friendly software. It’s also worth noting that Cricut machines have consistently faster cutting rates over a wide range of blade depths and materials.

When it comes to accessories and materials, Cricut faces the likes of Hobby Lobby, HSN, Jo-Ann, and Michaels, among others. Due to the low obstacles to entry, this sector is extremely competitive.

Valuation

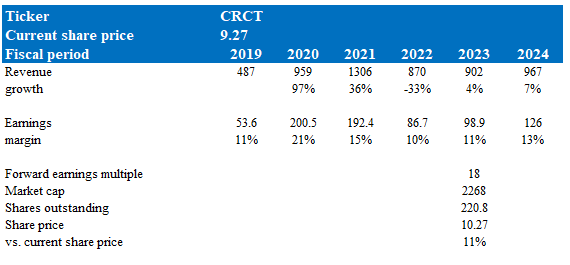

Unless there is a significant change in the near-term catalyst – demand returning to normal levels due to the post-Covid effect – I believe the stock has limited upside. According to my model, CRCT could be worth 11% more than it is now if it trades at 18x forward earnings multiple in FY23.

Model walkthrough:

- Revenue to face a steep decline in FY22 and minimal growth recovery in FY23 due to weak economy and Covid demand pull-forward effects.

- CRCT earnings margin to decline back to historical levels pre-Covid and slowly improve as subscription revenue becomes a larger mix.

- CRCT to trade at a forward earnings multiple of 18x earnings in FY23. I believe it is unlikely for CRCT to trade at the current 25x forward earnings given the slowing growth and higher rates. Hence, I think the market will re-rate this downwards to a lower multiple.

Own calculations

Risk

Competition

As was previously said, competition is extremely high in this field. Although I agree that the CRCT product is less straightforward and easier to use, I do not think this is a major differentiator that can’t be replicated.

Covid pull-forward demand

In 2020, CRCT earnings jumped by 97%, up from 43% in 2019, thanks to a 71% increase in the number of registered users. I think the company’s sales went up since more people stayed inside to do things like handicraft because of the lockdown. Investors should be prepared for some growth turbulence in the near future because of this, in my opinion.

Conclusion

CRCT is a company that produces cutting machines with computerized controls for home crafters. Personalization and customization are trending upwards, with many consumers willing to pay a premium for customized products. This presents a good opportunity for CRCT, as its machines are user-friendly and can be used on a wide range of materials. Additionally, the company’s vertically integrated business model allows it to participate in projects from the initial idea to the final product, giving it a competitive edge. However, the stock faces headwinds in the near term due to demand pulled forward during Covid, as such, I believe it is best to stay neutral for the time being.

Be the first to comment