Elevator Pitch

I maintain a “Neutral” rating on Hong Kong-listed Mainland China property developer China Overseas Land & Investment Limited (OTCPK:CAOVY) (OTCPK:CAOVF) [688:HK].

China Overseas Land’s revenue and operating profit decreased by -14.7% and -24.9% YoY in 1Q2020 largely due to the coronavirus pandemic, but the company expects a recovery in 2Q2020. China Overseas Land’s contracted sales decreased by -11.7% YoY in the first three months of 2020, as compared to a +25.2% YoY growth in contracted sales for FY2019. While there has been a recovery in contracted sales for China Overseas Land in March 2020, the company is unlikely to do better than a single-digit YoY increase in contracted sales for FY2020 under the best case scenario.

More importantly, the company still generated approximately 97.3% and 80.6% of its FY2019 revenue and operating profit from the cyclical property development business. As such, a “Neutral” rating for China Overseas Land is fair.

The company has set targets of achieving RMB5 billion and RMB10 billion in rental income by FY2020 and FY2023 respectively, and this is key to the positive re-rating of the stock’s valuations in the future.

This is an update of my initiation article on China Overseas Land & Investment Limited published on November 20, 2019. China Overseas Land’s share price has increased by +9% from HK$26.10 as of November 18, 2019 to HK$28.45 as of April 29, 2020 since my initiation. China Overseas Land trades at 7.2 times consensus forward next twelve months’ P/E, versus its historical five-year and 10-year average consensus forward next twelve months’ P/E multiples of 7.0 times and 8.3 times respectively. The stock also offers a historical FY2019 dividend yield of 3.6%, and a consensus forward FY2020 dividend yield of 4.0%.

Readers are advised to trade in the company’s shares listed on the Hong Kong Stock Exchange with the ticker 688:HK, where average daily trading value for the past three months exceeds $60 million and market capitalization is above $40 billion. Investors can invest in key Asian stock markets either using U.S. brokers with international coverage, such as Interactive Brokers, Fidelity, or Charles Schwab, or local brokers operating in their respective domestic markets.

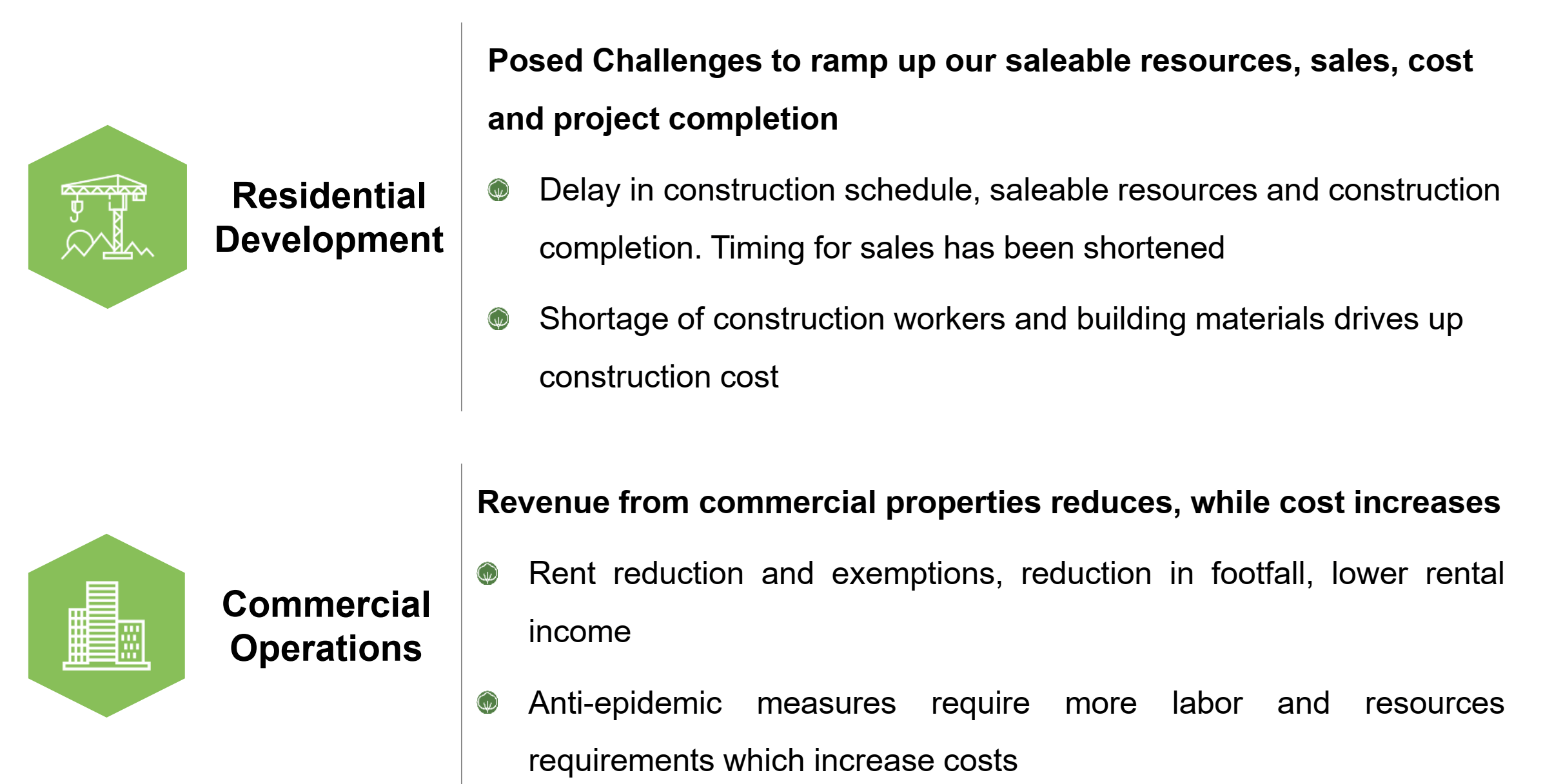

Impact Of Coronavirus Pandemic

In the company’s FY2019 financial results presentation slides released on March 26, 2020, China Overseas Land highlighted how the coronavirus pandemic has negatively impacted the company’s property development and property investment businesses as per the slide below. China Overseas Land derived 80.6% and 19.3% of the company’s FY2019 operating profit from its property development (residential development) and property investment (commercial operations) businesses respectively. The company generated the remaining 0.1% of its FY2019 operating profit from hotel operation, construction and building design consultancy services.

Negative Impact Of The Coronavirus Pandemic On China Overseas Land

Source: China Overseas Land’s FY2019 Results Presentation Slides

{kind=link}

On April 23, 2020, China Overseas Land provided an update on its 1Q2020 operating and financial performance. The company’s revenue and operating profit fell by -14.7% YoY and -24.9% YoY to RMB20.68 billion and RMB5.61 billion respectively in 1Q2020. China Overseas Land attributed the weak financial performance in the recent quarter to a slower pace of revenue recognition (construction progress was affected by the coronavirus pandemic) and foreign exchange losses resulting from a weakening of the RMB relative to HKD (the company changed its presentation currency from RMB to HKD starting with the FY2019 results). China Overseas Land’s contracted sales also declined by -11.7% YoY to RMB59.72 billion in 1Q2020.

Nevertheless, China Overseas Land has a positive outlook for 2Q2020 and FY2020. The company highlighted that “results of the first quarter shall not be taken as the basis for estimating change in profit for the full year” and it “expects the results in the second quarter to be restored” as part of its 1Q2020 update.

At the company’s FY2019 earnings call on March 26, 2020 earlier, China Overseas Land also disclosed that there have been signs of recovery. China Overseas Land mentioned that all of its construction projects have resumed work by late-March 2020, with the exception of Wuhan, the epicenter of the coronavirus pandemic. Similarly, all of the company’s property showrooms, except for Wuhan, were opened as of late-March 2020. Notably, Wuhan only accounts for less than 2% of China Overseas Land’s land bank as of end-FY2019.

Contracted Sales Growth Expected To Slow In FY2020

As highlighted earlier, China Overseas Land’s contracted sales decreased by -11.7% YoY in the first three months of 2020. However, it is important to note that the company’s contracted sales actually grew +7.0% YoY to RMB26.77 billion in March 2020, versus a -22.7% drop in contracted sales in 2M2020. This suggests the residential property market in Mainland China has recovered substantially since March 2020.

China Overseas Land’s contracted sales grew by +25.2% YoY to HK$377.17 billion in FY2019. Looking ahead, the company did not provide exact guidance on FY2020 contracted sales at its FY2019 earnings call on March 26, 2020, and only highlighted that it expects contracted sales to be higher this year compared with FY2019. China Overseas Land estimated that the company has approximately RMB680 billion in salable resources for FY2020, so a modest 55% sell-through rate will enable the company to match last year’s contracted sales.

Prior to the coronavirus pandemic, China Overseas Land has set a contracted sales target of RMB400 billion for FY2020. It is reasonable to assume that China Overseas Land should deliver at most a single-digit YoY increase in contracted sales for FY2020 under the best case scenario.

Rental Income Growth Targets Unaffected By Coronavirus Pandemic

China Overseas Land noted at the company’s FY2019 earnings call on March 26, 2020 that it has offered more than RMB20 million as rental rebates to provide support for tenants of its shopping malls up to the end of February 2020. China Overseas Land generated RMB3,749.5 million of rental income last year, and the company has set targets of achieving RMB5 billion and RMB10 billion in rental income by FY2020 and FY2023 respectively.

As of December 31, 2019, China Overseas Land owned 72 commercial properties, which included 45 office buildings, 12 flexible working office projects, 13 retail malls and two rental apartments available for long-term lease. Going forward, China Overseas Land has eight new commercial properties which are slated to commence operations this year, including two office buildings, two shopping malls and four rental apartments. The quality of China Overseas Land’s investment property portfolio is validated by the fact that all of China Overseas Land’s office buildings are Grade A properties, and approximately 60% of them are located in Tier-1 cities in Mainland China.

China Overseas Land should see a positive re-rating of the stock’s valuations over time, assuming the company is able to increase its revenue contribution from recurring income sources such as rental income from commercial properties in the next few years.

Valuation And Dividends

China Overseas Land trades at 6.7 times trailing twelve months’ P/E and 7.2 times consensus forward next twelve months’ P/E based on its share price of HK$28.45 as of April 29, 2020. As a comparison, the stock’s historical five-year and 10-year average consensus forward next twelve months’ P/E multiples were 7.0 times and 8.3 times respectively.

China Overseas Land is also valued by the market at 1.00 times P/B, versus its historical five-year and 10-year mean P/B multiples of 1.17 times and 1.63 times respectively.

China Overseas Land offers a historical FY2019 dividend yield of 3.6%, and a consensus forward FY2020 dividend yield of 4.0%.

The company recommended a final dividend of

Market consensus expects China Overseas Land to increase its dividends per share to HK$1.15 in FY2020, which implies a +13% YoY growth and an increase in the company’s dividend payout ratio to 29%. China Overseas Land’s future dividends are supported by a relatively comfortable net gearing of 39.4% for the company as of March 31, 2020.

Risk Factors

The key risk factors for China Overseas Land are weaker-than-expected contracted sales growth for its property development business, a slower-than-expected increase in rental income contribution from its property investment business, and lower-than-expected dividends in the future.

Asia Value & Moat Stocks is a research service for value investors seeking value stocks with a huge gap between price and intrinsic value, leaning towards deep value balance sheet bargains (i.e. buying assets at a discount e.g. net cash stocks, net-nets, low P/B stocks, sum-of-the-parts discounts) and wide moat stocks (i.e. buying earnings power at a discount in great companies like “Magic Formula” stocks, high-quality businesses, hidden champions and wide moat compounders). Sign up here to get started today!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment