CHUNYIP WONG

Real estate services firm CBRE Group (NYSE:CBRE) has been a fantastic stock over the past 6 years, having returned nearly 16% annually while the largest REIT ETF (VNQ) has returned less than 4%.

CBRE has been a beneficiary of:

-

Ongoing institutionalization of real estate whereby assets are increasingly owned by professional owners who outsource many services to CBRE and up until recently, transacted properties more frequently than individual owners.

-

Low interest rates which, until recently, have bolstered REIT and private fund returns and helped attract more capital to the real estate asset class driving transactions, financings, and demand for services.

While this has driven strong revenue and EPS growth for CBRE, there are other emerging trends which are negative for CBRE.

Near-term headwinds

Anyone who hasn’t been living under a rock this year knows it has been a terrible year for stocks. It has been an even worse year for REITs, with the largest REIT index/ETF VNQ generating a total return of -30% thus far in 2022. With cost of capital rising dramatically, REITs aren’t in a position to acquire many new properties.

While REITs represent a small percentage of the overall real estate universe, difficulties raising capital are becoming apparent in private markets as well. With the 10 year treasury having risen over 2% thus far in 2022, debt financing costs for real estate transactions has risen dramatically. The cost of 10 year debt for multifamily or industrial real estate (sub-sectors which don’t have significant structural headwinds like office) has increased from low to mid 3s during 2021 to around 6% today.

In late 2021/early 2022 cap rates for multifamily or industrial were in the mid 3s to low 4s. While cap rates have drifted up during 2022, cap rates are still below debt financing costs (known as ‘negative leverage’) which has curtailed the appetite amongst private buyers of these assets.

The slowdown in the transaction market was communicated via 2Q22 REIT conference calls. Here is commentary from the Essex Property Trust (ESS) management highlighting a significant slowdowns in transaction levels:

Essex Property Trust 2Q22 Transcript (Seeking Alpha Transcripts )

Similar commentary from Camden Property Trust (CPT) management regarding transaction levels:

Camden Property Trust 2Q22 Transcript (Seeking Alpha Transcripts )

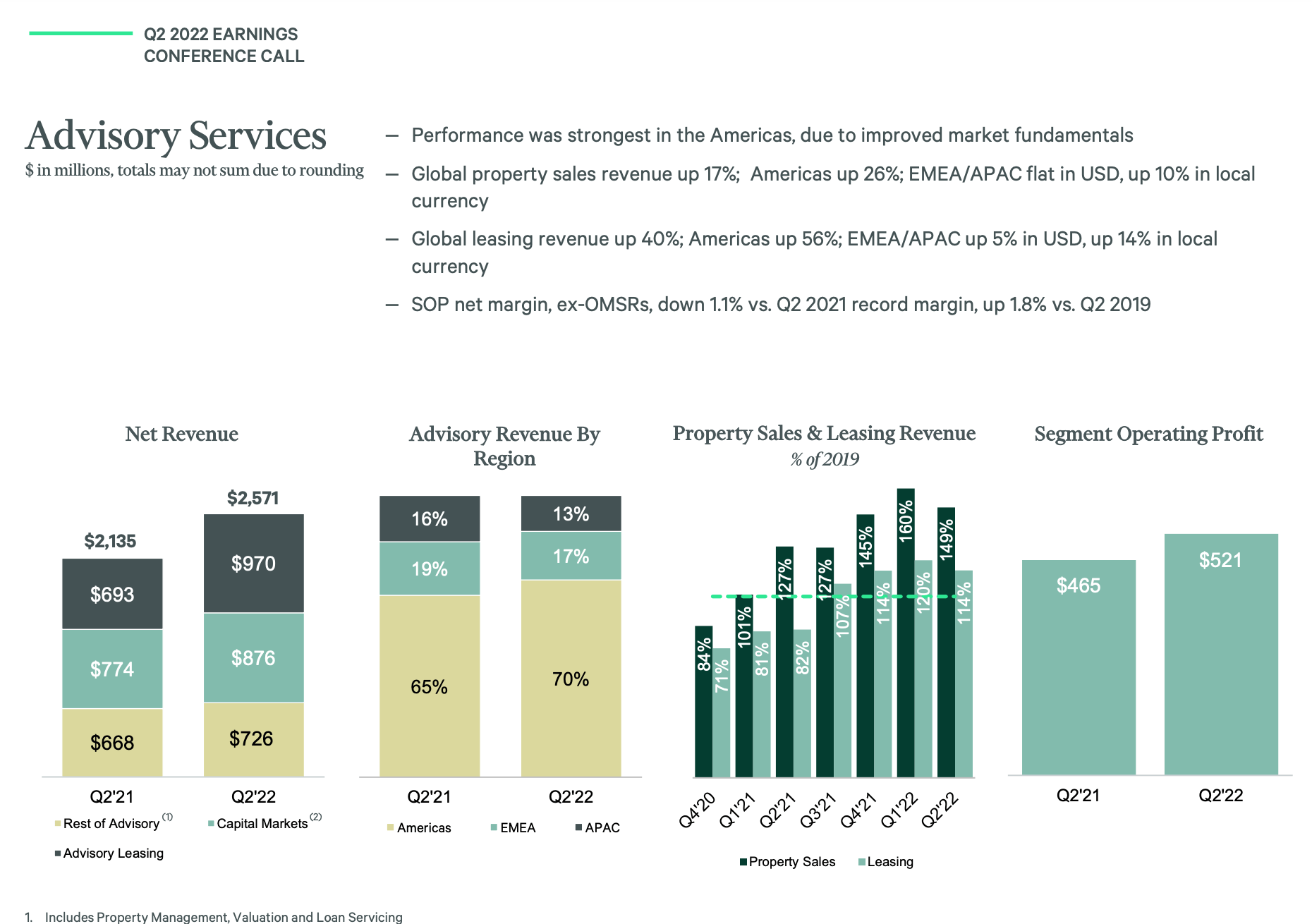

Pretty much every REIT (across multifamily, industrial, office, etc.) noted a significant slowdown in transaction levels. However, this slowdown hasn’t really hit CBRE’s results yet. As shown below, CBRE’s Advisory Services segment (largest segment within CBRE representing ~60% of group operating profit) showed a 17% YoY increase in property sales. It is important to note that most of the transactions which closed in 2Q were agreed to in 1Q or April (there is typically a ~60 day lag between agreeing to a deal and closing the transaction) when interest rates were much lower. The transaction market will be much weaker in 2H22 and likely into 2023.

CBRE 2Q22 Advisory Services Performance (Investor Presentation)

The other large subsegment within Advisory services is global leasing which consists mainly of office and industrial leasing. Both of these areas are economically sensitive. Many employers (META and AMZN both made headlines in the past couple months) are putting the brakes on signing new office space both due to work from home but also because employers are hiring fewer new workers (and in some cases shedding workers). This slowdown in leasing will further pressure this business segment.

Longer-term Headwinds

Private equity has been evolving over the past decade. Back in the day, the model was buy/fix/sell. The quicker it got done, the higher the IRR and sooner the realization of incentive fees. Sometimes there wasn’t even any fixing – A great example of this was Blackstone’s (BX) deal to buy Sam Zell’s Equity Office Properties in 2007 for $39 billion. BX divested 2/3 of the assets within 6 months. Think of the fees to a firm like CBRE – both on the buy & sell. Blackstone has become the largest owner of real estate in the world. But its strategy has changed.

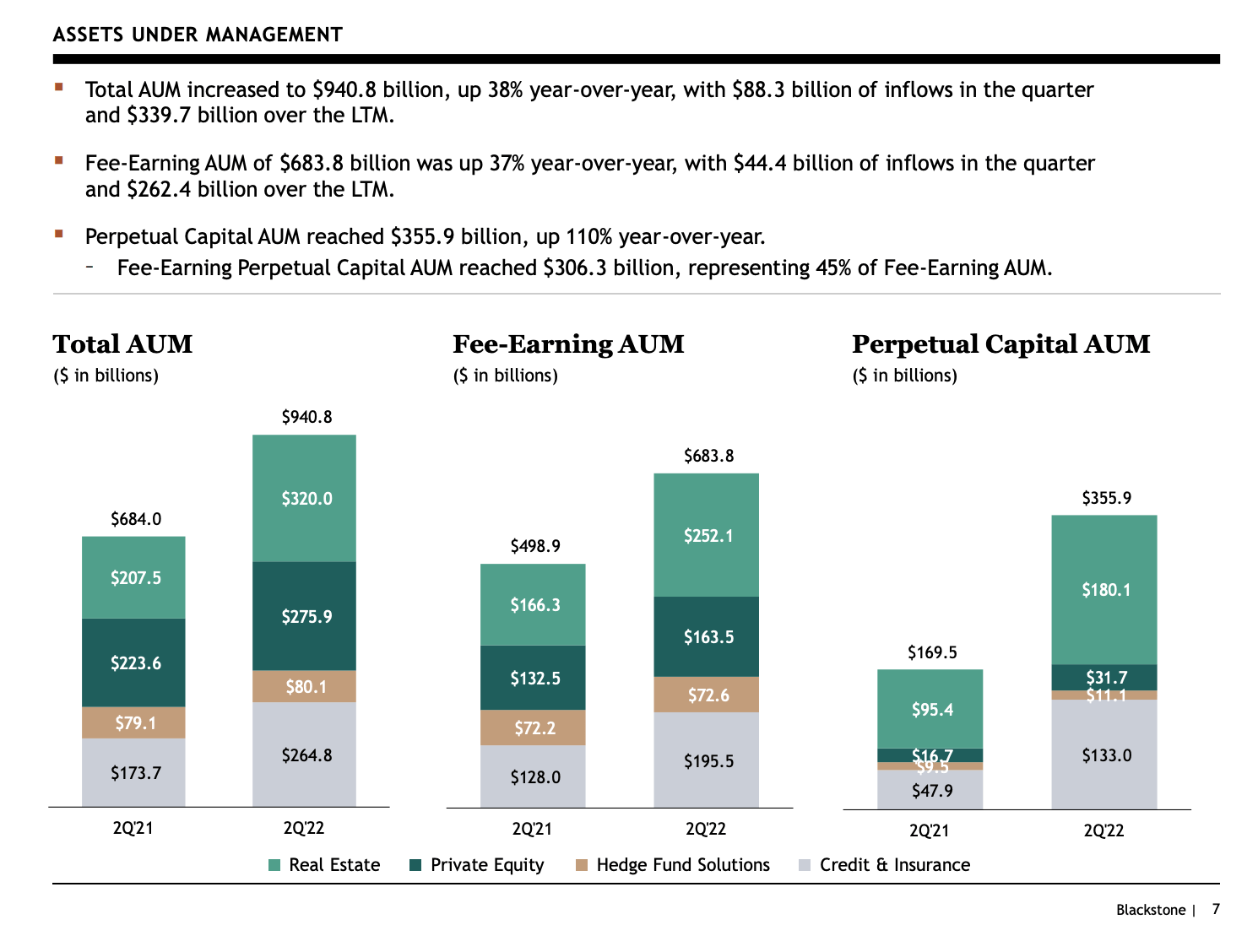

Blackstone Perpetual Capital (Blackstone Investor Presentation)

Today, increasing emphasis has been put on raising permanent/quasi permanent capital. As you can see above, in its real estate private equity business, perpetual capital now accounts for over 55% of total assets (the largest component is BX’s non-traded BREIT which has grown from $0 in 2016 to an astounding $126 billion today) which is up from virtually nothing 6-7 years ago. The reason BX has made this transition is because investors value earnings from recurring management fees at a much higher multiple than volatile performance fees which can disappear as capital market conditions change.

When BX raises permanent capital, it selects the assets for the fund differently. Rather than buy a troubled asset, fix it, and sell it, BX focuses on the thematic purchase of durable properties which can be held for decades. This change in strategy has implications for CBRE – while BX will still help the firm generate assets as it accumulates real estate for its permanent capital vehicles, it won’t need CBRE to sell the properties in 2, 3, or 5 years. It might not sell the properties for 10 years – or ever!

BX is not alone in pursuing the strategy. Starwood has launched a non-traded REIT which has grown from $0 to $26 billion in the past 5 years. It is employing a similar strategy. KKR launched a non-traded REIT following a similar strategy. The implications for CBRE from an increased prevalence of permanent capital is negative as more firms are holding real estate rather than paying CBRE to sell it.

Risks

If the Fed was to pause interest rate hikes, real estate equities, including CBRE would likely soar.

Conclusion

Despite a strong historical track record, I think CBRE has a tough road ahead as it faces both cyclical and structural headwinds. While the company appears to trade at a fairly low multiple (11.5x) of earnings, I believe that earnings are likely to decline significantly over the next 6-12 months.

Be the first to comment